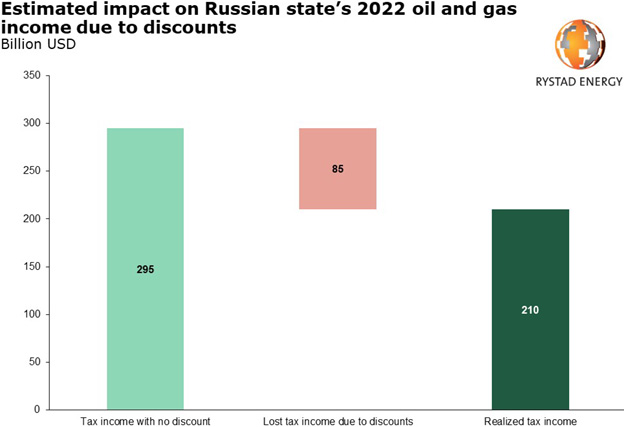

Russia’s government could lose as much as $85 billion in oil and gas tax income this year due to the significant discount to Urals blend crude, Rystad Energy research shows. The Urals blend – Russia’s key oil reference – has been trading at around $30-$40 per barrel lower than Brent – the global benchmark price for oil – since April. The steep discount on Urals shows that some of the sanctions imposed on Russia are having an impact and are reducing potential oil and gas income to the Russian government.

The Brent price surged past $100 per barrel following Russia’s invasion of Ukraine in late February, but not all producers are benefitting equally from the sustained high crude prices as the war rages on. Price differentials between Brent and other crude streams have widened considerably, and Brent is currently trading at a premium to almost all other crude streams. For Russia, Rystad Energy estimates that the total government income for 2022 would be around $295 billion if all oil assets realized the Brent oil price.

By using an average fixed spread of $40 per barrel between the realized price and Brent, we estimate that the tax income is reduced by $85 billion over the whole year, an almost 30% reduction compared to the “no spread” case. Rystad Energy estimates that the Russian government will earn around $210 billion in oil and gas tax income this year.

“We could potentially start to see the impacts of Western sanctions on Russian oil and gas revenues. The steep discount on Urals is costing the Russian government, while providing cheaper energy to some Asian economies. While the sanctions are likely to hit revenues, oil production has remained higher than expected, demonstrating that Russia’s upstream sector has adapted quickly to sanctions on sales,” says Daria Melnik, senior analyst at Rystad Energy.

Source: Rystad Energy research and analysis; Rystad Energy UCube

Source: Rystad Energy research and analysis; Rystad Energy UCube; Argus

Brent price differentials against other crudes narrows

During the first months of the Covid-19 crisis, between March and May 2020, several crude streams, such as Middle Eastern blends, traded at premium to Brent. At peak, this premium was close to $15 per barrel. Since the summer of 2020 until the beginning of this year, the spread between the different crude streams and the Brent price has been hovering around plus or minus $5 per barrel.

Spreads started to increase again at the beginning of this year, widening to between $5 and $15 per barrel for most of the largest crude streams, with Maya heavy oil blend increasing to almost $20 per barrel. With the outbreak of the Russian-Ukraine war, Urals blend started to trade with a large discount to Brent. From the middle of February to the beginning of March, the differential increased from $10 per barrel to $40 per barrel – this is the largest differential to date.

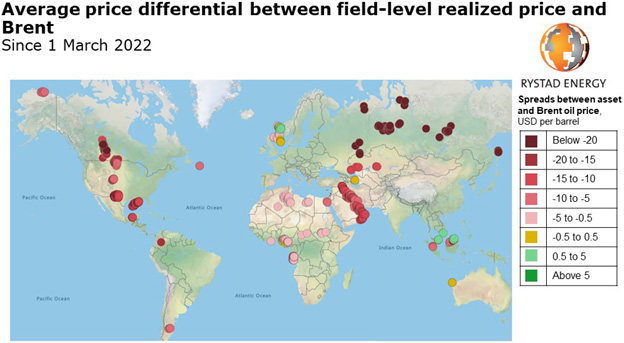

Since 1 March 2022, the price differentials between the field realized price and Brent have widened, all Russian oil and some Canadian oil sands blends have experienced a discount of more than $20 per barrel. In addition, Middle East crude is showing a discount of between $5 and $10 per barrel.

Revenues down but Russian production resilient

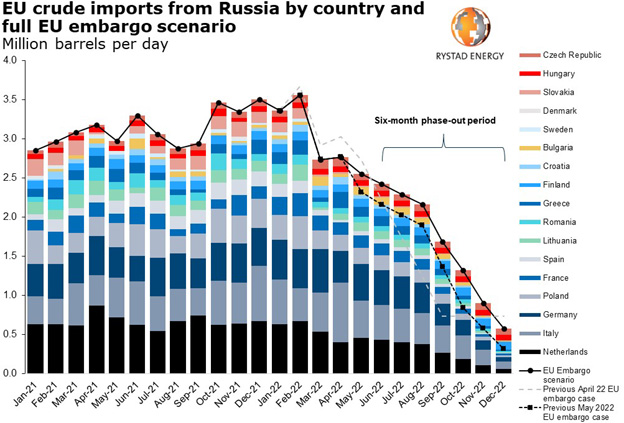

Russian crude production for this year is on track to be more robust than previously expected as the country’s industry has proven surprisingly resilient to Western sanctions over the country’s ongoing conflict with Ukraine. Russia continues to export crude at pre-conflict levels, following a huge drop in April, while refinery runs and oil output remain strong. Despite the European Union (EU) recently finalizing an embargo on Russian oil, its impact on Russian crude exports and production will be milder than Rystad Energy previously expected as we have made an upward revision to the country’s ability to redirect volumes. We now assume a more gradual phase-out of Russian volumes to Europe, with some undercompliance and lags expected in the first few months after the embargo comes into effect. At the same time, demand for Russian oil products, both inside and outside the country, ended up above expectations, leading to upward revisions in refinery runs for this year. As a result of this resilience, Rystad Energy has significantly revised Russian crude production for 2022, adding almost 700,000 barrels per day (bpd) to the previous forecast of 8.7 million bpd.

Source: Rystad Energy research and analysis; Rystad Energy Oil Trading Analyst Solution; Argus, Vortexa

Crude exports from Russia continued to grow in May and stayed above 5 million bpd, in marked contrast to a widely held belief that exports would fall due to Europe’s deepening cuts to imports. With the EU finalizing its embargo in June, Russia has successfully redirected more and more volumes to Asia – primarily China and India. In spring, total crude exports were higher than pre-conflict levels, signaling that Russian producers have managed to swiftly readjust to the new market reality. Refinery runs in Russia also began to recover in May. While Rystad Energy previously expected refinery runs to drop significantly due to what we anticipated to be a more pronounced economic downturn inside the country than what materialized and lower oil product exports, actual volumes increased by 135,000 bpd to just above 5 million bpd. In June, refinery runs showed an unprecedented growth by 700,000 bpd driven by higher oil products demand inside the country.

KeyFacts Energy Industry Directory: Rystad Energy