Europe is heading into a predicted power crunch earlier than expected despite recent moves to curb demand and increase supply. The turmoil – due in large part to Russia’s invasion of Ukraine and subsequent sanctions – could cause vast demand destruction across industries and consumers. European governments and the power sector have lined up support packages to soften the financial blow but may need to consider some drastic moves before winter begins to bite, Rystad Energy research shows.

The hope that summer would bring a reprieve has not materialized, as gas flows drop and liquefied natural gas (LNG) cargoes reach their capacity limit. With temperatures rising, supply may not be sufficient to meet demand in addition to restocking ahead of next winter. Rystad Energy has reviewed Europe’s options to fill the power gap until longer-term solutions are in place.

In April, we expected the next European winter to be a tough time for consumers and governments. Our updated scenarios show that Europe will probably be heading into the storm much earlier than previously thought – and that the region will be underprepared for the chaos it will bring.

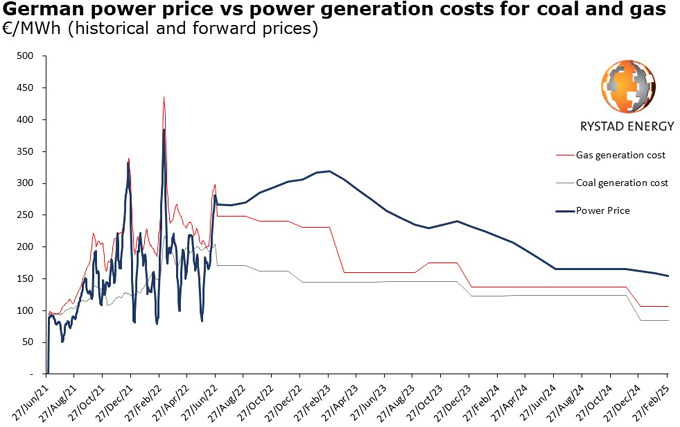

The uncertainty surrounding gas supplies to Europe is having a direct impact on power prices. Highly volatile gas supply has seen European power pricing swing far more wildly than before the war in Ukraine. At the start of Russia’s invasion in late February, prices spiked to a historical high of €530 per megawatt-hour (MWh) before stabilizing closer to €180 per MWh. Recent uncertainty surrounding Russian gas exports to Europe caused the baseload price to rebound to the current €278 per MWh – more than triple the price of a year ago. The surge in spot prices has lifted the forward curve, as the main uncertainty is for the winter when the supply/demand balance could get very tight.

“Europe’s options with regards to gas, coal, nuclear and renewables filling the power gap are extremely limited and costly. European governments have announced a raft of policies to secure more supply, support consumers and potentially curb demand should the crisis continue. The point at which the crisis will bite more deeply is looking closer and closer as we head into the summer and then autumn, this is increasingly a matter of ‘when’ and not ‘if’ the crisis arrives,” says Vladimir Petrov, senior power analyst at Rystad Energy.

Source: Rystad Energy research and analysis

Gas, LNG and reopening the Groningen field

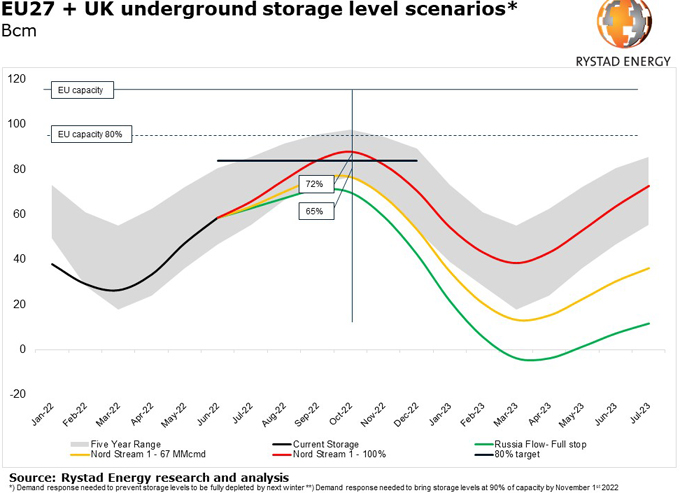

In recent weeks, a double whammy hit European gas markets. First, it was confirmed that the US Freeport LNG facility will be offline for 90 days before gradually ramping up production by the end of the year. Freeport LNG has over the past months exported most of its volumes to Europe – so with this development, 2.5% of Europe’s gas supply disappeared overnight. An even bigger blow was when the operator of the Nord Stream 1 pipeline from Russia to Germany said it would reduce exports from 167 million cubic meters per day (MMcmd) to just 67 MMcmd (Figure 2), instantly removing another 7.5% of Europe’s gas supply. This sent TTF gas prices surging from €83 per MWh on 13 June to €120 on 14 June and has since increased as Nord Stream 1 goes into a planned 10-day maintenance schedule.

Viable alternatives to Russian gas are limited in the short term. LNG terminals are running at full capacity, Norway is exporting as much as it can, and there is limited upside to exports from Azerbaijan and Algeria. If anything, the only major change on the supply side would be if the Netherlands were to ramp up supply from the veteran Groningen field. Groningen was once Europe’s largest gas field, with production of 55 billion cubic meters per annum (Bcma) – equivalent in supply terms to a full Nord Stream 1. The onshore field generated an increasing number of earthquakes over the past 30 years, and production has therefore been gradually phased out. The field has capacity to ramp back up to 20 Bcma relatively quickly if local and national governments permit, potentially offsetting a large share of the current shortfall from Russia. Such a restart at Groningen is speculative and could be politically contentious in the Netherlands, but it could clearly resolve many of Europe’s current concerns. So far, the Dutch government has only activated a plan allowing Groningen to produce 2.8 Bcm from the gas year ending in October 2023.

Coal prices set to increase

Germany has the largest coal power generation fleet in Europe and is now seeking to boost utilization, prioritizing near-term energy security over longer-term environmental targets. The country had a total of 46.7 gigawatts (GW) of installed coal power generation capacity in 2020, all of which was planned to be gradually decommissioned by 2038 to meet greenhouse gas emissions targets. Capacity was expected to drop to 36.1 GW already this year with the closure of at least 24 units. These plans have now been reversed, and the government is trying to extend the life of 10 GW of mothballed coal capacity until March 2024.

Source: Rystad Energy research and analysis, Refinitiv, Eikon

Of the plants being shut down between 2020 and 2022, around 20% burned lignite (brown coal which is mined in Germany) and the remaining 80% used hard coal, which is imported. A life extension of these plants is therefore likely to result in Germany needing to import more coal. Assuming an average load factor of 60%, these plants could generate 26.3 terawatt-hours (TWh) of electricity for the remainder of this year, equivalent to 9% of the country’s total generation. Additionally, 4 GW of German solar PV and wind capacity due to start up before the end of the year could add another 2 TWh of electricity generation. The extra coal, solar and wind generation could together replace 5 Bcm-worth of gas-fired power generation, equivalent to one-quarter of the gas normally consumed by Germany’s power sector.

With the international seaborne thermal coal market already incredibly tight, the prospect of additional demand from German coal-power restarts is certain to push imported coal prices beyond their current super-high levels. The main traded thermal coal benchmark (API2 specification 6,000 kilocalories per kilogram of coal delivered into Amsterdam-Rotterdam-Antwerp) is currently trading at around $377 per tonne, up almost $250 per tonne since the beginning of the year. German power utilities have been accustomed to burning a coal blend dominated by Russian coal with high calorific value and low in sulfur. European power plants will commonly blend high-sulfur US coal from the Illinois or Appalachian basins with low-sulfur Russian coal from the Kuznetsk Basin (Kussbass). This means that a switch from Russian coal is limited by the type of coal suited for individual plant boiler specifications.

The main preferred suppliers of high-energy, low-sulfur coal are producers in South Africa, Colombia and Australia. South African thermal coal exports into Europe have taken off this year, but there are significant obstacles in lifting supply further. The vast majority of South African exports are shipped from the Richards Bay Coal Terminal, which is struggling to operate anywhere near its capacity due to delivery problems with the rail transport system run by state operator Transnet. Poor maintenance, a lack of spare parts for trains, copper cable theft and vandalism have impacted rail delivery so badly that producers are even turning to road trucking up to 90 kilometers, at a cost four times the normal rail transport costs. Richards Bay free on board (FOB) coal prices (API4 specification) are now more than double what they were a year ago, but thermal coal export tonnages have only increased by around 8%.

Colombian coal exports are limited by mine production constraints, while Australian coal is often deemed too expensive and is essentially spoken for, which means there is very little international coal available for prompt delivery. One thing is certain: German coal-fired power generators are going to have to pay dearly for additional purchases. A potential relaxation of emission limits could allow generators to broaden their supply options with more US coal, but that is up to the German government to decide.

Nuclear

European nuclear power stations are not producing at capacity and many are facing shutdowns or reductions. European nuclear facilities are expected to average 69% utilization through 2022 unless shutdowns and reductions are reversed, below the global average of 76% utilization. Seven European nuclear power plants are earmarked to be shut down between now and the end of the coming winter. These power plants total 7.03 GW of installed capacity, representing about 1% of Europe’s dispatchable capacity and 10% of the remaining nuclear power plants. These plants include the Doel 3 and Tilhange 2 plants in Belgium, the Isar 2, Emsland and Neckarwestheim 2 plants in Germany, and the Hinkley Point B plant in the UK.

None of these plants are likely to have their shutdowns reversed or extended, but it is still possible to keep them running. The Belgian plants are not likely to continue running past their 1 October and 1 February shutdown dates, as the government stated in March that it would preserve two other plants instead. Hinkley Point B in the UK is slated for closure by 1 August, and there have been no signs of a reversal. The German government has been firm in its plans to eliminate nuclear power, which will be completed if the three remaining plants are closed as planned by 31 December.

Of all the above-mentioned plants, the three remaining German ones are the most likely – and perhaps the most necessary – to get an extended lease of life. Germany could amend its phase-out schedule to keep these plants running as they generate a significant amount of power – more than 1 GW each – and would greatly reduce some of the stress we see coming to the power grid this winter. One bright spark of note is that Slovakia intends to start generating 471 MW with a new nuclear plant, Mochovce 3, within the year.

Renewables

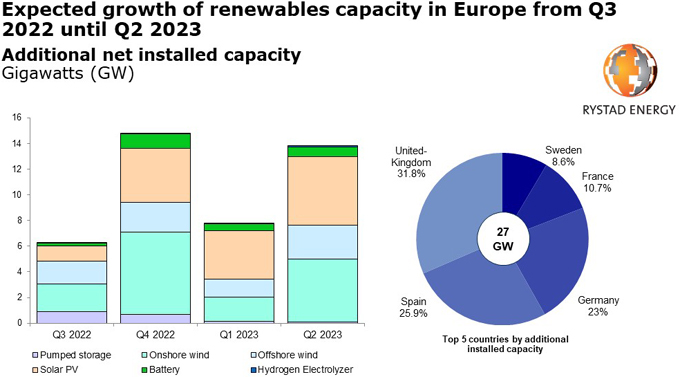

Given the current pipeline of projects in Europe, we expect 40 GW of additional renewables capacity to come online by the second quarter of 2023. Considering the 16 GW of new renewables capacity added to the power mix during the first half of 2022, the total installed capacity in Europe could reach 522 GW by the second quarter of 2023, covering 22% of the total power generation. Despite current supply chain bottlenecks and commodity prices crisis, 13.6 GW of utility-scale solar PV and 15.5 GW of onshore wind capacities should be added to the grid within the next 12 months. France, Germany, Spain, Sweden and the UK will lead the pace of installation, representing 67.5% of those potential new capacities.

Source: Rystad Energy research and analysis, RenewablesCube

The efficiency of offshore wind engineering, procurement and construction (EPC) companies will be key to support the replacement of Russian gas, as several high-scale projects are expected to start operations by the beginning of 2023, totaling 7.8 GW of additional capacity. Among those projects, the Hornsea Two farm (1.39 GW) in the UK North Sea is expected to be commissioned by the end of 2022, as the world’s largest offshore wind farm. In the meantime, battery storage will be essential to get the most out of renewables plants, given intermittency issues. We identified 2.4 GW of potential battery storage capacities to be added by 2Q 2023, with significant facilities such as the Wilton International BESS project (360 MW) being built in Teesside, UK.

These potential new capacities could be increased further if Europe manages to tackle its main barrier to the development of renewable energy – namely, permitting issues. Through the RePowerEU action plan, the European Commission acknowledged the pressing need to address the bottlenecks in the permitting process and has already released a legislative proposal to facilitate permitting. By adopting policies such as putting a one-year cap on the time needed to secure a permit in dedicated areas, renewables could grow more quickly and support the replacement of Russian gas in the power mix.

Europe’s ability to get through the winter will depend on how much can be done during the summer months to decrease demand and increase both imports and domestic production. All options are on the table, and Germany recently signed a 20-year deal for US LNG, the first of its kind and notable for the long duration of the deal. Domestic production, however, will be the crucial factor. All eyes will be on Nord Stream 1 when it is rescheduled to open on 21 July. The scale of the challenge means that Europe is already in a position where any and all options must be considered in order to find every spare molecule of power.

KeyFacts Energy Industry Directory: Rystad Energy