The importance of Asian turbine OEMs is on the rise and much of this can be attributed to the rapid development of Mainland China’s offshore wind sector, which has grown to become the world’s largest offshore wind market in recent years. Global turbine OEMs have been serving the offshore wind market for a much longer period of time in comparison to their Asian counterparts, however Asian OEMs (from Mainland China, and the region as a whole) are now starting to be seen as potential alternative sources. This is being supported by the demand from Asian countries outside of Mainland China, with ambitious offshore wind targets. The question is, will Asian turbine OEMs become a force to be reckoned with, or will they struggle to make ground?

Asian markets are ready for the taking

National offshore wind targets and the development of an offshore wind industry within Asia has provided Asian turbine OEMs with a market that is ready for the taking over the next decade. Proximity to market is an important advantage that Asian turbine OEMs have over global turbine OEMs when it comes to marketing their turbines.

In 2020, emerging offshore wind markets such as South Korea and Japan announced national offshore wind capacity targets of 12GW and 10GW respectively by 2030. Asian countries are forecast to have a total installed capacity of 163GW of offshore wind by 2030 – larger than all the capacity in Europe – albeit over 70% of that will be in Mainland China. This represents a huge demand for turbines that need to be met. Bolstered by such demand, it would be strategic timing for Asian turbine OEMs to gain market share.

Trends in Asian turbine OEM market

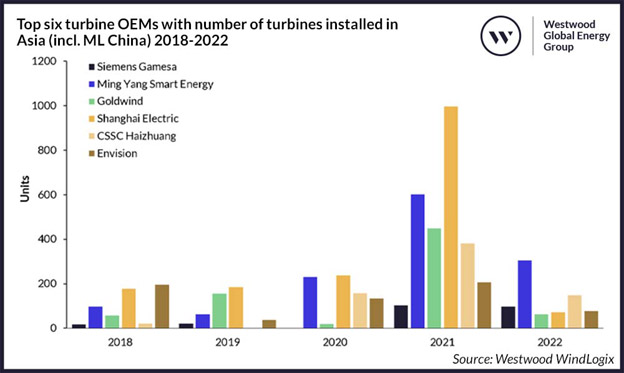

While the global market has primarily been supplied by the top three global turbine OEMs – Siemens Gamesa, Vestas and GE – a review of Asia’s turbine installations over the past five years shows that Asian turbine OEMs have dominated the market. Siemens Gamesa is the only non-Asian OEM that is featured in Figure 1, coming in at sixth place in terms of market share. It is worthwhile to note that Shanghai Electric benefited from technology transfer from Siemens Gamesa.

FIGURE 1: TOP SIX TURBINE OEMS WITH NUMBER OF TURBINES INSTALLED IN ASIA (INCLUDING MAINLAND CHINA) 2018-2022

SOURCE: WESTWOOD WINDLOGIX

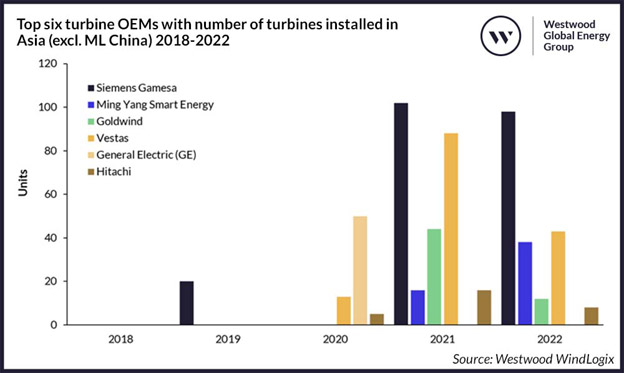

FIGURE 2: TOP SIX TURBINE OEMS WITH NUMBER OF TURBINES INSTALLED IN ASIA (EXCLUDING MAINLAND CHINA) 2018-2022

SOURCE: WESTWOOD WINDLOGIX

When Mainland China is excluded from the analysis, we see that global turbine OEMs (Siemens Gamesa, Vestas and GE) account for 75% of total turbines installed over 2018-2022 in the region. However, the key point to highlight here is that Asian turbine OEMs Goldwind, Ming Yang Smart Energy and Hitachi have managed to succeed in taking over some regional market share outside of Mainland China.

The price advantage of Asian turbine OEMs

One of the key advantages that Asian turbine OEMs have is that they can typically offer turbines at lower prices. Mainland Chinese turbine bid prices locally have fallen 34% from 2020-2022 levels since the central government subsidy was terminated, effectively responding to the need to lower offshore wind development costs in Mainland China. At the same time, global turbine OEMs are facing financial difficulties. Certain developers in South Korea have said that some global turbine OEMs are offering much higher prices for their turbines in a bid to bridge the gap for their financial difficulties. Among these developers’ considerations – on top of price – are localisation and reliability as well as competence. In the context of price, Asian turbine OEMs certainly have advantages over global turbine OEMs.

Barriers: Localisation isn’t easy

There are no signs indicating that Asian turbine OEMs will have it easier than global turbine OEMs when it comes to localisation in Asian markets. Japan, South Korea and Taiwan each have their own local content preferences. Being Asian is not a licence for easily winning turbine contracts on Asia offshore wind projects. An example is Taiwan’s second operational wind farm, the 109.2MWChanghua Demo Phase 1, which used turbines supplied by Japanese turbine OEM Hitachi. While that is the case, Hitachi has yet to win any other large-scale contracts for projects in Taiwan. It is therefore noteworthy that Asian turbine OEMs, like global turbine OEMs face the challenge of localisation and this stems from a recognition that Asian markets are diverse and heterogenous with unique local content requirements.

In terms of localisation difficulties faced by global turbine OEMs, the collaboration between Vestas and Taiwanese outfit Tien Li Offshore Wind Technology to build wind turbine blades locally in Taiwan was not a smooth operation. According to sources, localisation of Vestas’ designs faced challenges with technology transfer and talent cultivation, adapting to local conditions for blade manufacturing. It took four years to tweak the production process until April 2022 when the first V174-9.5MW blade was manufactured.

Taiwan’s latest local content rules for Round 3 offshore wind auctions – which call for 60% local content – could provide further challenges for turbine OEMs. The most recent rules will force turbine OEMs to create a local content strategy to service the Taiwanese market. As we have seen from the Vestas example, it took many years to manufacture blades locally. Therefore, this heightened emphasis on localisation, which encompasses turbine components, may present an additional obstacle for OEMs regardless of whether they are global or Asian, seeking to enter the Taiwanese market.

Case Study: South Korean turbine OEM market

In a bid to achieve local content, 2022 saw multiple partnerships take place between Korean turbine OEMs with global and Asian turbine OEMs. Asian OEMs such as Ming Yang Smart Energy and Shanghai Electric are entering the South Korean market through collaborations with Korean turbine OEMs. This is fresh territory for these OEMs, so close to home. Global turbine OEMs such as Siemens Gamesa, GE Renewables and Vestas have also formed partnerships with local partners to manufacture their designs in South Korea. Vestas has also announced plans to move its Asia-Pacific headquarters to South Korea.

TABLE 1: MARKET MOVEMENTS IN THE TURBINE OEM MARKET IN SOUTH KOREA

SOURCE: WESTWOOD WINDLOGIX

The fact that these new partnerships took place within the span of a year in 2022 showed that the market situation is very competitive and dynamic in South Korea. Asian turbine OEMs are making the same moves as global turbine OEMs around the same time, suggesting that Asian OEMs have a good chance of penetrating the South Korean market. South Korean developers that Westwood spoke to welcome these market moves and are keen to see how these partnerships will pan out. A strategic point of concern raised is that the turbine models marketed in South Korea need to be suitable for local wind speeds.

Success in South Korea?

Two out of five foreign turbine OEMs entering the South Korean market are Asian, but their success will likely depend on how competitive the turbine models are in South Korea in terms of marketed turbine ratings, maintenance competencies and track records.

Due to their wealth of experience, global turbine OEMs can provide long term maintenance contracts with greater OPEX certainty, and this is advantageous to project financing. Inexperienced turbine manufacturers, which includes the Asian OEMs to some extent, are unable to provide a reliable input to project OPEX. There is a perception among some South Korean developers that Asian turbine OEMs (including the Mainland Chinese and Korean turbines) have reliability and competency issues.

Another point of discussion is whether Asian and Korean OEMs will significantly benefit from their alliances. Will Pan Asian localisation possess stronger business relationships and capabilities, compared to those initiated by global turbine OEMs? Not necessarily. As Taiwan shows, global turbine OEMs have done well in localisation and in this regard Asian turbine OEMs have yet to prove if Pan Asian localisation works better. A lot of uncertainties lie in these partnerships and whether it will prove successful, remains to be seen. The fact that the Korean government is revising its regulations for offshore wind development including doing away with the local content requirement also poses uncertainty. Having in-depth knowledge of the Korean market through a local partner is a recipe for success, but whether turbine sales will improve in South Korea and in Asia is unclear.

Balancing cost vs reliability vs localisation

Asian turbine OEMs have a significant opportunity to become a force to be reckoned with if they can take advantage of the opening Asian markets to become a credible alternative to global turbine OEMs. They need to quickly gain market share and with that a good operational track record.

It will take time before they can become an accepted alternative to the dominant group of global turbine OEMs – both in region and further afield. What the Asian turbine OEMs do have is a good starting point, proximity to Asian markets and the ability to provide turbines at a lower cost. Mainland Chinese OEMs also have a strong domestic base to grow from.

Ultimately success will come down to how much developers weigh their options based on cost versus perceived quality, as well as the influence of any localisation policy, which has an equal effect on all OEMs.

Ruth Chen, Senior Analyst

rchen@westwoodenergy.com