Dave Waters

Director/Geoscience Consultant, Paetoro Consulting UK Ltd. Subsurface resource risk, estimation & planning

Is writing articles here a sign that we have nothing better to do? Too much time on our hands? Not really. Is it an integral part of some great crusade? Not really. For me, I like writing. It is an opportunity to clarify my thinking to myself. If everything has to have some great purpose that's a shame really. I do it because I enjoy it and it helps me, and every so often it would appear it helps others to clarify their own thoughts. Which way? That's their choice.

So, energy transitions. Where are we?

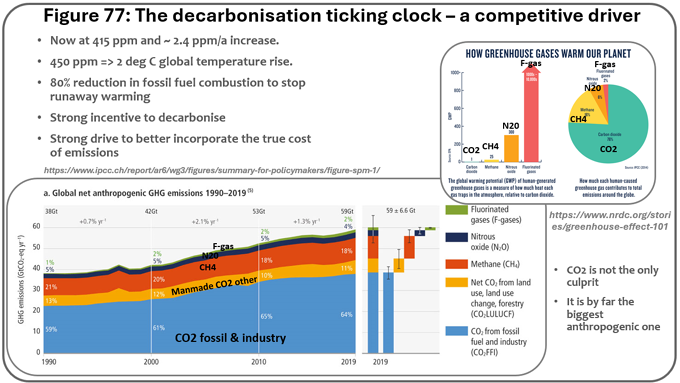

The reason for wanting one is not going away. "Figure 77" below, as for many in this text, is lifted from another article so ignore the number, but it informs why we want to reduce free burning of hydrocarbons as much as we can.

We want to stop runaway warming. Not because the planet has never been warmer in geological time (it has), or because CO2 is some poison, but because the climate, food, water, sea level, and energy systems of a world of unprecedented population of 8 billion people in vulnerable largely artificial systems, are at risk. Not to mention habitats of many other species we would quite like to preserve.

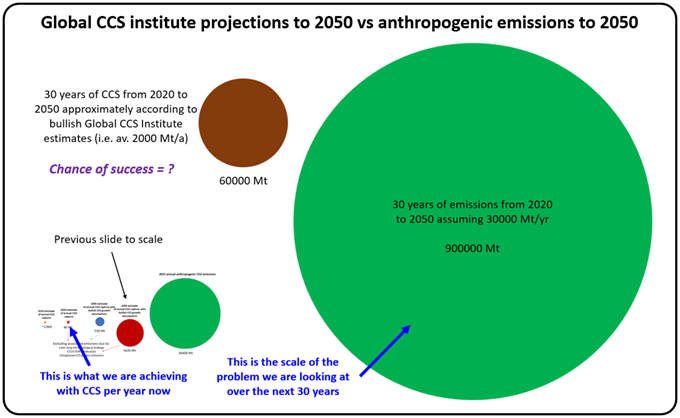

These emissions are not something that any kind of carbon capture has any hope of compensating. The below figure illustrates the scale. We will explore natural carbon capture stabilisation routes to help, the day when we stabilise emissions at a bearable level, but first we have to reduce them. We might practice it before then, but we manage expectations as to its priority.

This leaves us with a problem, because we have survived off a multi-hundred million year windfall of fossil energy accumulation for a couple of centuries and more, and that reliance is interwoven into the very fabrics of our societies and supply chains. Changing it is not going to be easy. The amazing volumetric energy densities of hydrocarbons have lifted the world into a "bloom" of activity and prosperity. Now however, we know that this cannot continue for two key reasons. Firstly, if we burn all the remaining hydrocarbon resource we will do irreparable harm to future generations of people and other biodiversities. Yet so much of our energy, especially very high heat intensive things like refining metals, has depended on this rich volumetric energy density from hydrocarbons for so long. Obtaining such energies from other routes is challenging, and for now costly.

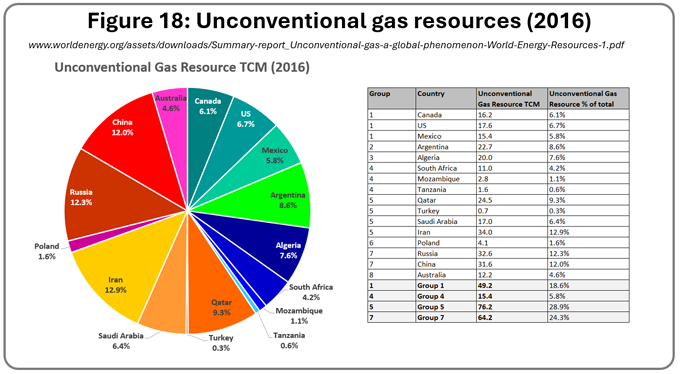

The immediate problem is not a lack of hydrocarbon resource. Although that which can be extracted economically is not an inexhaustible resource, it cannot go on forever; there is a very large amount of resource left still, which we can technically access, even if at greater cost. Arguably the best illustration of that is the unconventional gas resource the planet has, as per the figure labelled # 18 below - again stolen from another article of mine. As we can see it is Russia, China, the Middle East, North Africa, Argentina, Canada, Mexico and Australia which dominate the underexploited areas of this resource pool, to accompany the US, where it has been put to use and effectively prolonged that country's reliance on hydrocarbons, for better or for worse. The problem then is not running out of resource, the problem is twofold - how we damage the environment if we burn it (and we've already seen CCS will not rise to any mitigating challenge there), and the fact that it will cost more to extract. Not just $ and damage, but in terms of energy and materials.

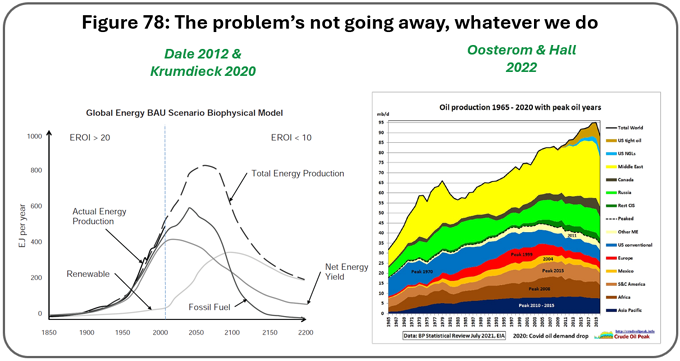

If we look below at the figure labelled #78, we can see the problem is similar for oil and not going to go away. We might as well then - if we are going to be investing huge amounts, think about doing it on things that have much longer running room. 2020, at the right end of the Osteroom & Hall chart at right in the figure, was COVID time and a bit unusual, but there are several key things to note.

Firstly that every region apart from Russia, perhaps Canada, and the Middle East has peaked for conventional oil production. These regional peaks have occurred not because every last drop of technically accessible oil has been squeezed out, but because the logic of competing with much larger, cheaper resources in the Middle East, North Africa, and Russia, has dissipated.

Secondly that a new lease of life for the US oil production was provided by "tight oil" but that its scale is of a temporary reprieve, not a long-lasting solution.

Thirdly though, if we look at the chart on the left, we see that whatever happens, business as usual would chew up the fossil fuel resource in an unsustainable way, and whatever the details of the precise date "peak oil" would happen, it is a day that is coming. Sometime this century even if we change nothing. After that the challenges for oil production will only worsen and worsen. There is then, great incentive to contemplate the "what else then?".

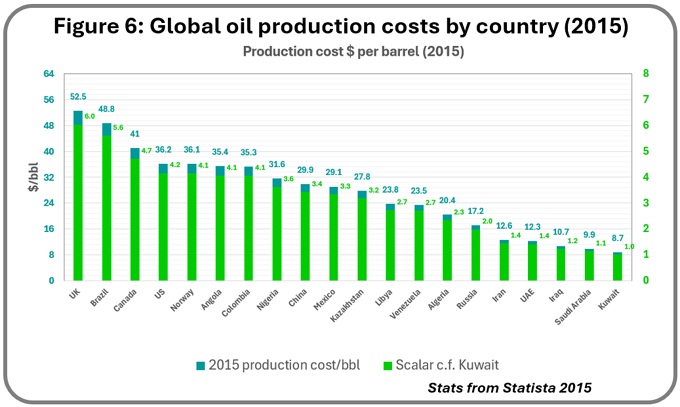

One of the key things to reiterate, is that this regional distribution story is largely driven by regional competition. If we look below at the figure labelled #6, the stats are a little out of date now, but the general trend still holds. The production cost in the Middle East, North Africa, and Russia, is far less than that of North America and Europe, and offshore deep water provinces of the Atlantic. Conventional gas is a fairly similar story, and we have already seen we have very little respite from that if we turn to unconventional gas instead.

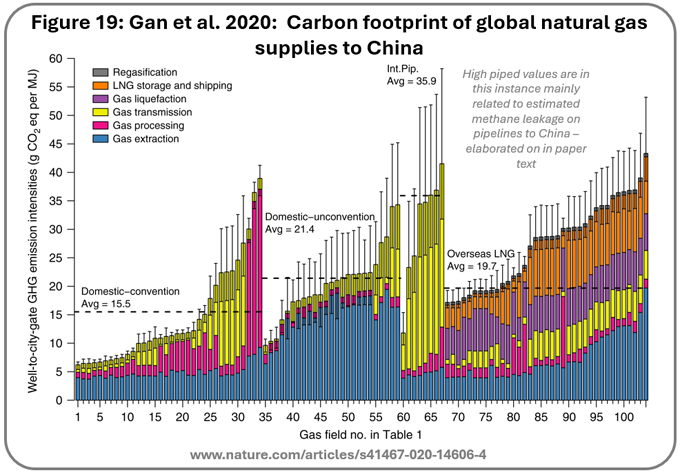

Furthermore, let's compare the emissions footprint of the different gas modes (conventional, conventional internationally piped, unconventional, LNG). We can recognise that unconventional gas use results in far greater emissions per MJ as shown in the figure labelled #19 below. That is an additional problem. As carbon pricing kicks in more fully, and it will, that will have an impact on competitiveness.

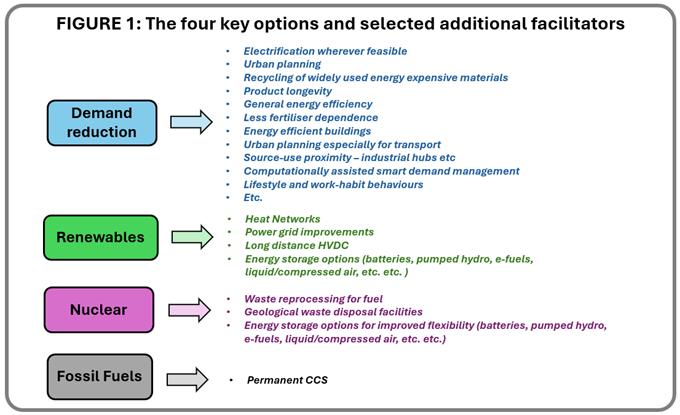

So what are the options then? There are effectively four key mega-pathways forward to tackle the problem. The first is demand reduction. This is infrastructure-led routes to do what we need to do, but using less energy to do it. Electrification and general efficiency is just one aspect of this. There are many others that are more proactive design planning at nation-scale to modify how we do things. Not to impose some iron portcullis, or cage, but to provide choice for people and companies to achieve what they need to using less energy. If it sounds a dream, it isn't a dream, but it is hard, and will take decades, and the rest, to plan and evolve.

The second is renewables, and the third is nuclear. Each of these has a wide variety of sub-categories, but a general problem is that they tend to be either full on - for reasons of operating efficiency (i.e. not inability to stop), or they are intermittent. That is to say an issue of supply not exactly matching demand. For hydrocarbons, that is in general much easier to switch on and off to match. So, for either of those things, nuclear, or renewables, to match user demand, requires management. There are three key ways that this can be done.

- Energy storage - keeping as much of the energy as feasible in a form that can be reactivated later on demand.

- Distal transmission - increasing the pervasiveness of long-distance continental-scale transmission of energy so that intermittency at any one location "averages out" more. We are not restricted to the renewable "capacity factor" of where we are located any more. We send where needed, receive when needed.

- Smart design management that juxtaposes users (e.g. high energy industries) with locations where temporal surpluses might on occasion be anticipated. Energy sponges to do something useful and permanent with the energy when it happens to be available, but which don't mind too much sitting dormant for a bit when it is not.

Doing these things is not trivial or without various types of cost, as we shall discuss further shortly, and there are electrical engineering challenges tied-up in much of it. There is however progress on those issues, and we can expect more. From some countries more than others.

The last option in the figure labelled #1 below, is fossil fuels "lite". Effectively as for now, but with a bit of mitigating carbon capture tacked on where we can manage it. Not something, as we have seen, that can ever solve the problem on its own. It is worth saying though, that if we can tackle all the other three routes effectively, then where, despite best efforts we have to fall back on fossil fuels for something somewhere, this might occasionally provide further help in that circumstance. Faint praise maybe, but not one to discount totally as long as we manage expectations on what it is capable of.

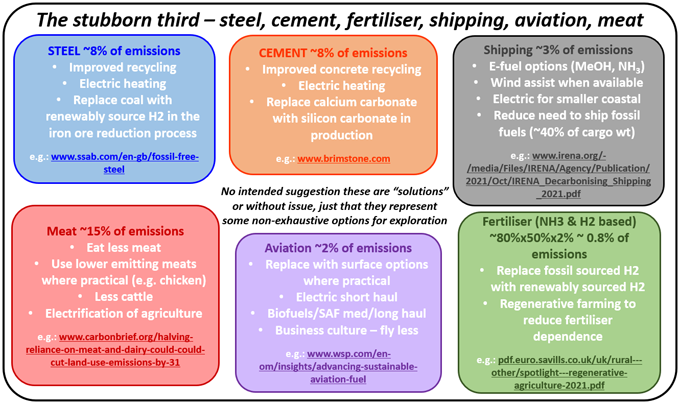

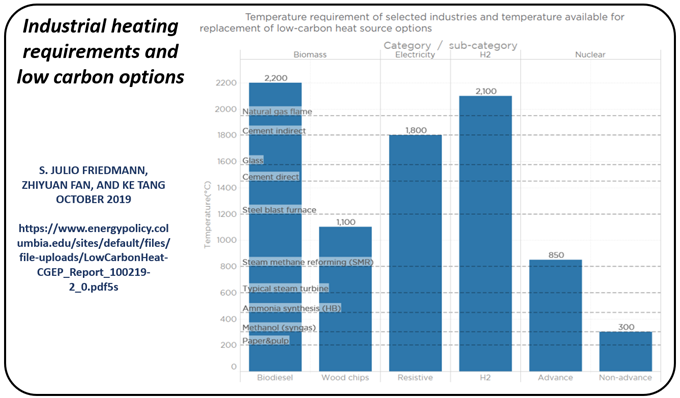

Now it has to be said, there are some things that are hard to do without hydrocarbons. Not necessarily technically impossible, but potentially costlier. Some of them are listed in the figure below. These are things that account for significant amounts of our emissions and which are harder to do without hydrocarbons. Not impossible though, and without being an advocate necessarily for any of the routes suggested, some of the non-fossil options that have been mooted are listed. It is a space that is fluid. Moving. Improving. Not without crashes and burns and false trails occasionally, but on average, progressing.

In general, it is the industrial process heating which poses the biggest challenge. Those requirements are summarised in the chart below.

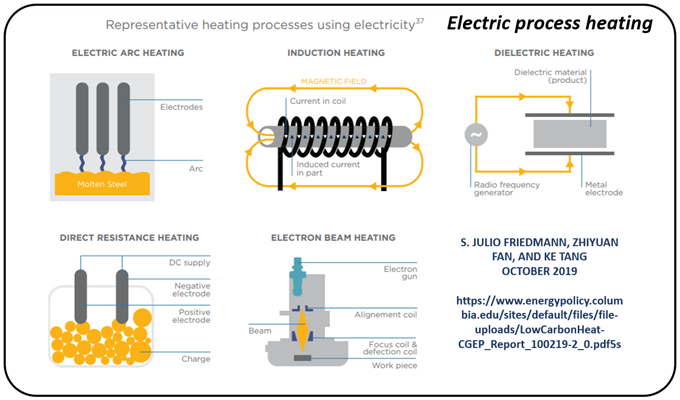

There are technically feasible routes to achieve the temperatures required with electric process heating as shown below, but the issue is really for now the cost, and also the sheer scale of electricity generation that is going to be required to do things this way. Bearing in mind we are also simultaneously switching all sorts of other things over to electricity too, on top of the stuff we use it for already. EV's, heat pumps, etc. etc.

Is electricity quantitatively up to the job - including refining and recycling all the materials required to sustain renewable and nuclear systems? I have a go at trying to think about that question more fully in a separate series of articles beginning with the first in the series here:

Similarly, I think a bit about a UK case study, beginning here:

There are no trite answers to all these questions. It is not going to be easy. However, we have no option other than to try. Fossil fuels are not going to be around forever to hold our hand into the sunset, so we need to think about what the viable plan B's are as soon as we can. Not rushing in foolishly where angels fear to tread, but getting on with the assessment. Nations are beginning to do so strategically, and we can get a bit myopic about levelised costs of energy and all those things, but the big players get it, and are building systems now for the days when hydrocarbons cannot be the number one reliance. Those who don't will be left behind. The financiers, including the insurance industry especially, are already on the boat. They can see the un-insurability-mayhem writing on the wall and don't want to be caught out.

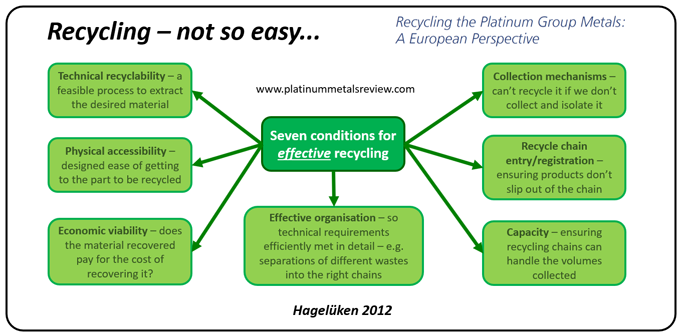

A key element in looking at the far future is thinking about recycling. Recycling everything is a non-sequitur. Recycling can be very difficult, and there are some things it just doesn't make sense to recycle. For some things, landfill is the best option. It can, after all, be an energy and cost-consuming exercise on its own. As shown in the figure below, there are a lot of things that need to align for recycling to be effective. It has to be planned at system-scale. There are some things, though, for which recycling is eminently economic and if we can recycle them, we save ourselves huge amounts of energy related to refining from scratch.

Recycling can never be perfectly 100% efficient, but what we can do helps. There are some big ticket items that can be recycled fairly easily and take us a long, long way in energy saving. For example steel, aluminium, copper. Other things, like the battery materials, nickel, cobalt, lithium, etc, help too. Really though it is the big three with the massively-scaled use of steel, aluminium, and copper that make the most difference. Not least because a considerable amount of metallurgical coal mining and associated emissions is also invested in steel production.

Note at this point that anything which uses vast amounts of steel and doesn't recycle it, is costing us vast amounts of energy relative to things that can. Perhaps most poignantly the various steel alloy tubings we use to case thousands upon thousands of oil & gas wells. Geothermal too, although the scale of that is much smaller. For all these, often with important amounts of other critical minerals to enhance pressure, corrosion, and temperature performance. They are left in the hole permanently and not recycled. That is in contrast to surface renewables materials which, to increasing measure, can largely be recycled, even if that is not always straightforward.

All this brings us back to our choices. Renewables, nuclear, demand reduction, fossil fuels-lite. Which delivers the best option? In truth that is a false question. In reality there are many different characters of energy supply and use and whatever story emerges, it is likely going to be a complex mix unique to every site and user. A story though that can shift considerably from the present. We can get fixated on short term machinations of prices, which typically, as we witness now, go up and down with short term fluctuations in supply chain availability and perceived geopolitical risks. What is more relevant to the long-term strategic attitude to what works best is the energy and effort input into the different routes, and the material availabilities to facilitate their supply chains.

A key aspect of this is the metric we refer to as EROI, or the energy return on invested. In a nutshell the concept is very easy. We don't gain much if we are expending more energy to produce useable energy than what it gives us. EROI is about how much energy we have left over to use, after we have poured all the energy we need into obtaining it. While it is not directly linked to price, indirectly it is ultimately, looking through long-term glasses, the most fundamental driver of it. If we can get more energy for less effort, we want to.

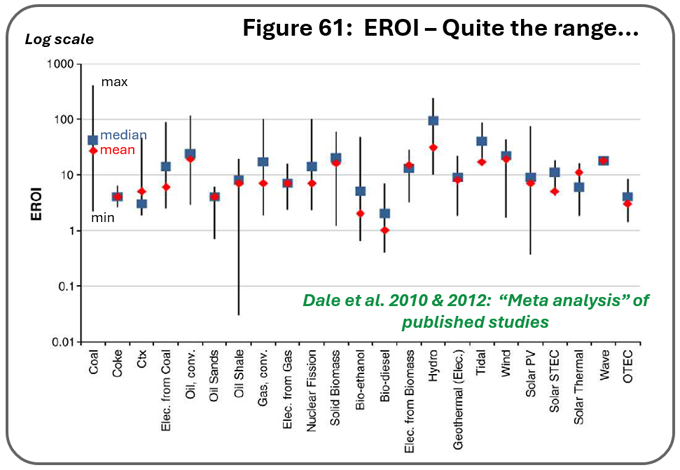

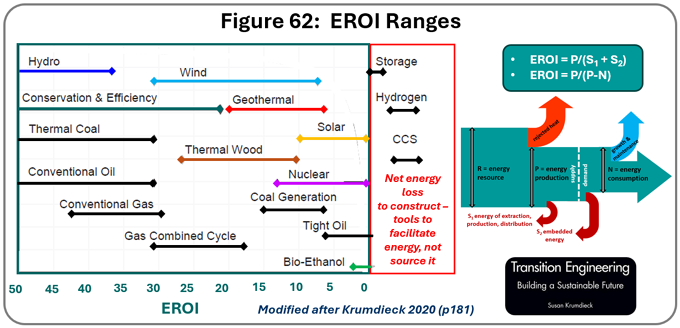

The history of the metric is a chequered one, because everyone measures these things differently and it matters where you start and where you finish. What we include in the process. Do we measure it just as delivery to customer, or in final overall use? Do we include geological waste repositories or don't we? Such things matter. The most important thing though, is to think about the concept, and in our own analyses to be self-consistent in comparison. The figure labelled 61 below gives a feel for this EROI variability issue. It is simply a collation from published literature of the EROI's calculated for different routes by different authors, with a mean, median, min and max shown, without presuming any consistency in method.

The figure numbered 62 below shows an estimate of various EROI's from 2020. Things have since moved on a bit, but there are some key takeaways. Firstly that conventional oil and gas at their inception were considered to have delivered great (high) EROI. Back in the days when finds were big and onshore and not so deep. In general, anything less than EROI 5 is considered marginal from a societal sustainability perspective. More than 50 marvelous. Anything less than 5 and it's akin to an energy mouse wheel. Running to stand still.

We can see that the renewables, apart from excellent EROI of hydroelectric, are seemingly lower in EROI, but they do still get into some comfortably useful ranges of 15 and above. However the point often made is that for many of these renewables to function practically, we need add-ons like distal transmission networks, or storage. Those are drags on EROI. They have energy and $ cost, and yet do not provide any new useable energy sourcing. So a system which has both renewables and storage, has a lower EROI than the renewables EROI in isolation would lead us to believe. That said, the same is true of CCS for oil and gas. So hydrocarbons today suffer the same issue. If we are going to mitigate their emissions with CCS at a site, then this drags their EROI down.

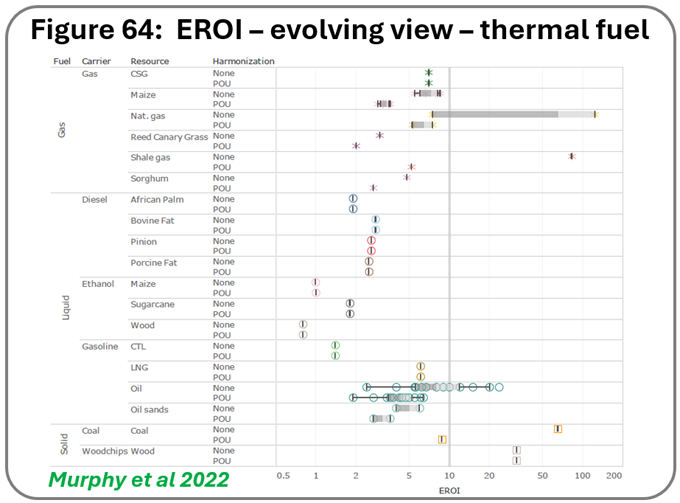

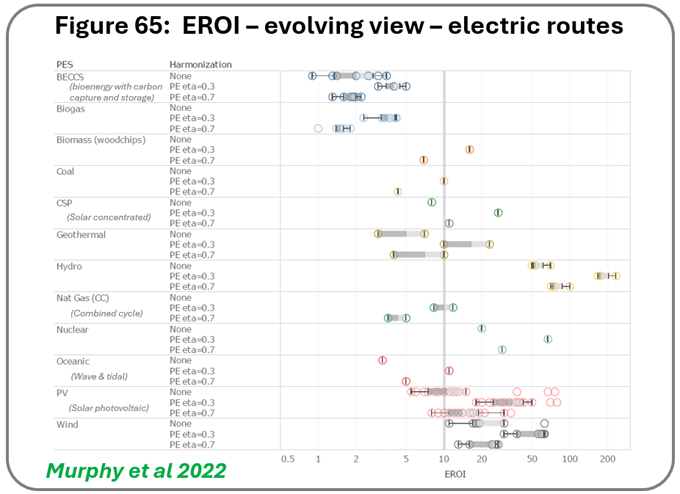

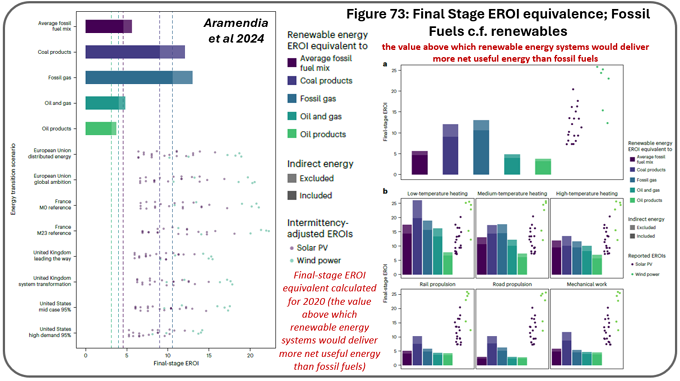

More recently we have seen more movement in the EROI calculation field, and these iterations note that previously, a lot of calculations have not taken EROI to full end use. To cut a long story short, when such correction is made, the distinction between modern production of oil and gas, nuclear, and renewables is far less clear cut. Even when the "EROI drag" for storage etc is taken into account. See the figures below numbered #64 and #65 and #73. The last one incorporating that correction for end-use. EROI accounting for what the final user in practice gets, not just what the provider delivers to them.

This is not to say renewables are the answer, it is merely to say any EROI advantage of modern oil and gas production has effectively gone, if it ever was as good as once thought. There are other things than EROI that dictate which energy sourcing is best for a particular site, but what this tells us is that at systems scale, whatever happens next, whatever we choose, suffers the same lowering EROI problem, and has roughly similar EROI values. If one of those routes also then happens to significantly damage our atmosphere where the other doesn't, that tells us something important about where we should invest most of our new efforts.

What it also tells us, is that if EROI is decreasing with time for all options, as ore grades decrease, hydrocarbon recovery becomes more energetically intensive, and recycling energy demands increase, then demand reduction will have a critical role along any new supply, transmission, storage, and smart usage routes.

Are there great engineering challenges ahead? Sure. Are all options likely going to persist in various uses for various reasons at various scales? Yeah. At least until we get our heads around some of the toughest engineering challenges. Yet, is there room and reason for fundamental changes in the proportions of energy sourcing from different routes, including renewables and nuclear? Yes. To make that work though will require proactive planning on energy demand reduction too.

The centuries-scale windfall of hydrocarbon-based energy is coming to a gradual end and we need to plan for its retirement. To learn to live within our energy means.

Any references listed in this article can be traced via the listings in the links referred to earlier.

KeyFacts Energy Industry Directory: Paetoro Consulting