The Journal of World Energy Law & Business, Volume 19, Issue 1, January 2026

Independent experts in oil trading disputes are often told by law firms that damages are to be calculated based on the difference between the ‘Market Price’ of the cargo at the time of the breach and the ‘Contract Price’ that would have applied if the breach had not occurred. ‘Market Price’ and ‘Contract Price’ are not straightforward because the price of a cargo is rarely a single fixed number. Instead, the price emerges from a formula, the outcome of which varies substantially depending on the highly volatile value of the many variables comprising the calculation. To explain what the ‘Market Price’ of crude oil or refined oil products is, this article examines the oil price negotiations that take place when oil changes hands and how both the Contract Price and the Market Price can vary substantially. In order to allocate damages fairly, judges and arbitrators typically want an answer from the expert that gives them a number, or a narrow range of numbers, pure and simple, on which to base their assessment of damages. In the words of Oscar Wilde, ‘The truth is rarely pure and never simple.’ This article attempts to explain why this is the case for oil prices and damages in oil trading disputes.

Independent oil trading experts are usually instructed by the law firms appointing them in oil trading disputes that damages are to be calculated based on the difference between the ‘Market Price’ of the cargo at the time of the breach and the ‘Contract Price’ that would have applied if the breach had not occurred.1

‘Market Price’ and ‘Contract Price’ are concepts that are not as straightforward as they may at first appear. That is because the price of a cargo is rarely a single fixed number. Instead, the price emerges from a formula, the outcome of which varies substantially depending on the highly volatile value of the many variables comprising the calculation.

To explain what the ‘Market price’ of crude oil or refined oil products is, it is necessary to examine the oil price negotiation that takes place when oil changes hands, and how both the Contract Price and the Market Price can each vary substantially.

In order to allocate damages fairly, judges and arbitrators typically want an answer from the expert that gives them a number, or a narrow range of numbers, pure and simple, on which to base their assessment of damages. In the words of Oscar Wilde, ‘The truth is rarely pure and never simple.’ This article attempts to explain why this is the case for oil prices and damages in oil trading disputes.

Formula pricing

The oil market abandoned fixed pricing, such as $A per barrel (‘$A/bbl’) or $A per metric tonne (‘$A/Mt’), in contracts for the majority of physical, or ‘wet’,2 cargoes of oil back in the 1980s.

The fall of the Shah in 1979 and the Iran–Iraq war in 1980 triggered rising and increasingly volatile prices that discouraged commitment to fixed prices for oil that was to be delivered some weeks or months later, when the market price could have changed out of all recognition. Consequently, there had been a rapid increase in the volume of oil traded under ‘spot’ contracts for one-off cargoes, rather than longer-term contracts for multiple cargoes delivered regularly over a period of time.

Flexibility became an important aspect of the price-setting process as the volume of oil in the spot market grew from somewhat less than 10 per cent of world production in the early 1980s to the many multiples of daily production that it is today. This is because cargoes change hands many times over before reaching the final buyer. Each transaction is a separate entry in the market’s oil price database.

As the volume of spot trade grew, prices for physical contracts and over-the-counter (OTC) forward contracts began to be assessed and published by a few Price Reporting Agencies (PRAs). Today, these assessments are central to trading activity and are driving the development of many trading instruments and contracts.

In response to the growing volatility and uncertainty of the 1980s, the oil market adopted formula pricing based on the price of one of a few fixed ‘benchmark’ contracts. Benchmarks are contracts in which the price continued to be a fixed number, rather than a formula.

In the case of crude oil, some early benchmarks were the OTC forward Brent and Dubai contracts and the exchange-traded futures contract in West Texas Intermediate (WTI). In the case of refined products, early benchmarks were the then International Petroleum Exchange’s3 (IPE) Gasoil contract or the New York Mercantile Exchange’s (NYMEX) Heating oil contract.

To qualify as a pricing benchmark, a grade of oil must have at least one of its contracts traded at a transparent fixed price, $A/bbl or $A/mt. This fixed number can be used to solve the oil price formula equation in non-benchmark contracts.

The price formula typically uses a benchmark price averaged over a number of publication dates plus/minus a grade differential (‘$G/bbl’ or ‘$G/Mt’) to reflect the value of any differences between the benchmark price and the oil in question that is the subject of the contract. This differential can be a fixed number or can itself be calculated from a formula made up of quality, freight, timing, and any other variables relevant to the cargo in question that differ from the benchmark.

In summary, non-benchmark contracts contain a formula that allows the trader to agree a differential, $G/bbl or $G/Mt, to the benchmark number, $A/bbl or $A/mt. The value of A in a non-benchmark price formula is the reported price of A, published by a PRA, averaged over a varying number of days.

PRAs and MOC

The most pervasive PRA is S&P Global Energy, commonly referred to as Platts in the oil community. Its largest competitor is the highly respected Argus Media. Oil companies and trading houses have supported the convolutions necessary to maintain a flow of publishable benchmark data to the PRAs, even when no actual deal evidence can be located.

These companies supply bids and offers into a widely consulted electronic platform at key 15-minute periods around global trading hubs each day. This is known as the Platts Market on Close (MOC) e-Window electronic data entry platform (‘the window’) managed by Platts and hosted by ICE. Price indications to buy or sell and actual deals may only be entered into the MOC process in the Platts-approved format by companies that have been pre-approved by Platts to participate.

Often, it is not actual deals for the grades of oil that form the benchmark database or the price assessment that gets published. It is often just price indications to buy or sell that do not result in an actual deal. Frequently, the published price is based on tiny 25,000 bbl or 5000 Mt parcels, depending on the specific crude oil or refined product agreed in the MOC window. Deals entered into in this platform must either be cash settled or consolidated into a number of other similarly sized parcels to accrue a deliverable volume.

An astonishingly large amount of crude oil and refined products that change hands every day contain a formula price that refers to a Platts oil benchmark derived from this MOC process. This includes spot and term contracts, government tax reference prices, and Official Selling Prices (OSPs) used by state oil companies in production sharing agreements that contain cost recovery and profit share calculations.

Is the MOC process open to manipulation? That is not the subject of this article, but it is interesting to note that in May 2022, the Commodity Futures Trading Commission (CFTC) issued an order filing and settling charges against Glencore ‘for manipulative and deceptive conduct...which spanned from least 2007 to 2018, involved manipulation and foreign corruption in the U.S. and global oil markets, including manipulation or attempted manipulation of four U.S. based S&P Global Platts physical oil benchmarks and related futures and swaps’. Glencore was required to pay a total of $1.186 billion.5 Similarly, in 2020, the trading company, Vitol, was fined $95.7 million by the CFTC for, among other infringements, ‘conduct, which spanned from 2005 to early 2020, involved foreign corruption and physical and derivatives trading in the U.S. and global oil markets, including attempted manipulation of two S&P Global Platts physical oil benchmarks’.

Over time, the benchmarks have altered out of all recognition. Production of some benchmark grades of oil has declined, trade routes and delivery points have transformed in response to environmental and other legislation, sanctions, destination restrictions, shifting seasonal consumer demand, and improvements in infrastructure. Typical efficient cargo sizes (and therefore freight costs) have also evolved. If the characteristics of a benchmark, A, change, the formula price differential, G, for physical contracts also has to change.

This is where it starts to get tricky for calculating damages in a legal dispute using the difference between a Market price and a Contract price.

The question for the purposes of this article is, does a Platts benchmark assessment of an oil price constitute ‘the market price’ that is relevant to the calculation of damages when compared with the contract price in a legal dispute?

The answer is undoubtedly no.

A benchmark is an assessment, albeit an influential one, of what the price should be of a cargo that mirrors the exact deal parameters assumed by the PRA in making its assessment. In the market any two parties can construct their contracts in any way they both agree, which may be wildly different from the standard used by Platts in assessing its benchmark prices.

No one forces independent counterparties to any transaction to use any particular benchmark or any other terms in their bilateral deals. There is no objective, universally recognized rulebook that determines what is, or what is not, the Market price. It is only if the counterparties to the contract wish their deal to be included in the Platts benchmark assessment process that their contract is required to conform to the Platts standards. Or that any differences between the contract terms and the Platts standard are reported at the time, so that Platts can make an adjustment to the Contract price before including it in their benchmark assessment database.

Often, no deals are done on which an assessment can be made. Or the Contract prices that are done are transacted on an entirely different basis than that assumed by the PRA.

The actual cargo contract may be for a different:

- Formula price averaging period;

- Delivery date and the date on which the deal is transacted;

- Cargo size;

- Delivery location;

- Grade and quality of oil; and

- Attributes such as optionality in delivery date and/or price averaging period, sanctions and destination restrictions, non-standard credit terms, etc.

It is necessary for any appointed expert required to opine on damages, to differentiate between the Contract price and the PRA benchmark assessment that may be held out as being the Market price.7 This can be a complex and data-intensive process.

Hitting the ‘G’ spot

The differential, $G/bbl or $G/Mt, to the benchmark, $A/bbl or $A/Mt, itself may be a formula that expresses a value for all the differences between the characteristics of the benchmark grade of oil that make up the price assessment, A, and the characteristics of the non-benchmark grade of oil in question that make up the value of G.

The price averaging period

The two counterparties to any trade have complete flexibility in choosing which benchmark, A, to use and the precise published price averaging period agreed to set the value of A.

Sometimes the Contract price formulae use the 5-day average of published prices around the bill of lading (B/L) date for physical oil delivered free on board (FOB) tankers at a loading port. This is so-called ‘2-1-2’ pricing. In the case of West African grades of crude oil and many refined products, the norm is to use the 5-day average of published prices after the B/L for FOB cargoes. In the case of cargoes traded on a cost insurance and freight (CIF) or Delivered at Place (DAP) basis, the price averaging period often relates to the cargo discharge date rather than the B/L date.

Not all actual deals done in the market are transacted on a 5-day average period, particularly in the case of refined products. Some agree using a whole month average (WMA) price averaging period, with the ‘month’ being determined either by the actual B/L date of a cargo, a deemed B/L date, or the date of the Notice of Readiness (NOR) to load or discharge the cargo. Others are done on a balance of the month average (BALMO) of published prices, often the remainder of the month following the deal date.

If the deals or indications that are reported in the 15-minute period on the electronic platform are on a different basis from a 5-day average or any other assumption made by the PRA for the particular benchmark used in the Contract price, the dealer is expected to report this to the PRA so that a further adjustment can be made. It is unclear if dealers actually report any such differences as assiduously as they might.

If the trader reporting to the PRA omits to mention the fact that its deal is not based on the same price averaging period relevant to the benchmark in use, this introduces a skew in the pricing. For example, if a deal for a late cargo in a month is entered into the MOC e-window electronic price discovery platform, described above, by a trader without mentioning that the pricing is WMA, rather than say, the 5-day average assumed by Platts for that benchmark, and the market is in backwardation, the reported price will be overstated. This is because earlier, higher price assessments will be included in the formula price averaging period. If the market is in contango, it will be understated.

The delivery date: a goalpost on wheels

Given the logistics of moving oil around the world in tankers, it is difficult to be certain in advance what the delivery date of any cargo will actually turn out to be. That may be because of loading or cargo documentation delays at a terminal; a ship may arrive early or late; the party in control of the tanker—the buyer in an FOB sale or the seller in a CFR, CIF, or DAP sale—may decide to slow steam to ensure as late a delivery date as possible, or alternatively to order full speed ahead to ensure as early a delivery date as possible.

Because the ultimate price formula is calculated, usually by reference to the B/L date or the discharge date, unsurprisingly, there is a temptation to tweak these delivery dates. This is particularly so around a month-end, when there may be a change in the host government’s Official Selling Price (OSP) for taxation purposes between the months.

Often, to provide certainty and to facilitate hedging, the parties will ‘deem’ the B/L or discharge date in advance. In other words, they agree on a likely delivery date and use that date in the Contract price formula, irrespective of what the actual delivery date turns out to be. Foreknowledge and certainty of the delivery date, and therefore which price averaging period will set the Contract price, reduces price risk by facilitating hedging.

These technical niceties are of considerable importance. Given the volatility in oil prices, a 2-1-2 price average will give a completely different value for A than a 5-day after-delivery price average, or a WMA or BALMO price average. Coupled with the ability to finesse the actual delivery date by control of the tanker, the variables in the Contract price formula can be very elastic. If the dispute involves the non-delivery of the Contract cargo, there is a wide range of possible delivery dates, each of which would have resulted in a different Contract price if the cargo had been delivered.

Hence, when considering the value of G used to adjust the benchmark value of A, the price averaging period used for the Contract price is of supreme importance in establishing the final Contract price, A + G. So also, is the actual delivery date of the cargo, which is open to tweaking by the charterer of the tanker that carries the oil.

Time is money

The same barrel of oil can be worth many dollars of difference in price depending on whether it is to be delivered next week, next month, or next quarter. This is not because oil prices are moving up and down all the time, although they are: it is because traders of oil will value identical oil at a higher or lower price today, depending on when it will be delivered.

Accordingly, the Contract oil price formula in a deal will usually include a discount or premium to the chosen published benchmark price to reflect, among other things, any difference in the delivery date range of the cargo in question and the delivery date range considered by PRA in assessing the benchmark price that the counterparties are using in their Contract price formula.

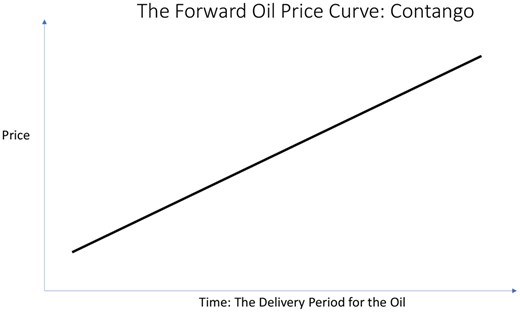

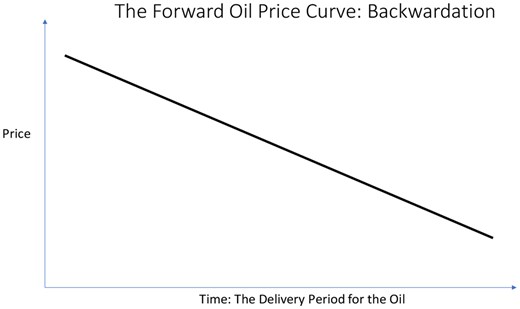

This concept is represented typically as a forward oil price curve, which is a graph showing the current benchmark price, shown on the Y axis, for the same barrel to be delivered at various future points, shown on the X axis. The slope of the curve may be upward sloping from left to right (‘contango’) or downward sloping from left to right (‘backwardation’). This is illustrated in Figures 1 and 2.

Figure 1. Price varies with the delivery date of the oil-contango.

Figure 2. Price varies with the delivery date of the oil-backwardation.

In the first case (Fig 1), contango, oil for prompt delivery is less valuable at that point in time than oil for delivery in a later period.

In the latter case (Fig 2), backwardation, oil for prompt delivery is more valuable at that point in time than oil for delivery in a later period.

Both these figures represent a single point in time and what traders are prepared to pay at that point in time for oil to be delivered on different future delivery dates. It is not a price forecast.

The difference in the Market price of a cargo at any single point in time, depending on its delivery date, differs from the concept of the difference in the Contract price of a cargo when the price formula is based on different price averaging periods. This is a difficult distinction to convey.

For example:

-

if a cargo is to be delivered 20 days forward from the price assessment date and the market is in backwardation, the cargo should attract a higher price differential today than the same cargo for delivery 45 days forward.

-

if a cargo is to be delivered 20 days forward from the price assessment date, the Contract price that emerges at the end of the price averaging period will be different depending on whether the Contract price formula is based on a price averaging period of 2-1-2, 5 after B/L, WMA, or BALMO, etc.

The slope of the forward oil price curve can be referred to as the time differential (‘T’) to distinguish it from the height of the forward oil price curve, the absolute price, determined by the benchmark price, A.

T may also be represented as one of the variables comprising the grade differential, G, along with quality, freight, cargo size, etc.

Clarity and precision about these abstruse concepts are needed when calculating damages in a disputed transaction.

The ‘normal’ dealing period

A further aspect of the time differential, T, is the forward benchmark cargo delivery date range assumed by the PRA in assessing the benchmark price compared with that of the cargo in question. If the cargo deal has been transacted before or after what is deemed by the PRA to be ‘the peak time’ for trading specific cargoes in the market, the reported deal may be excluded from the PRA deal database or have the price adjusted by the PRA to bring it in line with its own benchmark assumption.

The PRA usually specifies the delivery date range it is assessing for a benchmark cargo. If the delivery date range of the physical cargo being negotiated varies from the PRA’s benchmark delivery date assumption, an adjustment in the Contract price formula can be made in the form of a premium or discount to the benchmark price in assessing the value of G, the total grade differential. This time differential, T, is derived from the slope of the forward oil price curve.

In the case of crude oil, the peak trading period usually starts when the crude oil terminal operators agree a schedule of liftings for the forthcoming month with the users of shared storage facilities and berths at the terminal. This is usually performed on a monthly cycle. (But see WTIM below.) The peak trading period usually ends when it becomes too late to arrange and vet a tanker, put credit security in place and organize cargo documentation. Thereafter, a cargo is considered to be distressed, and its price is no longer deemed representative of the true market value.

If the benchmark grade price, A, is assessed by the PRAs for delivery, say, 45 days forward from the PRA publication, and the Contract price is for a cargo for delivery, say 20 days forward from that date, the grade differential, G, must contain an adjustment to reflect the value of T. In this scenario, if the market is in contango, T will be a negative number. If the market is in backwardation, T will be a positive number.

The value of the time differential, T, can be fixed upfront in a contract by agreement of the counterparties to the deal, usually, but not always, at the time the physical oil sales contract is agreed. This may be expressed generally as:

-

minus $T/bbl, indicating a contango market; or,

-

plus $T/bbl indicating a backwardated market.

In the case of refined products, the peak trading period operates on a shorter time fuse than crude oil. The start point typically varies with storage and berthing facilities at the port from which an FOB delivery is to be made and may include cargoes loading as early as 3 days forward from the deal date. In the case of CIF deliveries, deals can be arranged further in advance and are influenced by the sailing time from the refinery to the end-user’s delivery point. The endpoint again is determined by practical considerations of tanker or barge scheduling, credit security, and documentation.

Quality: basket cases

In the case of refined products, the quality of the oil delivered is highly specified in the contract. With some notable exceptions, usually involving politics and sanctions, the refinery from which the product originates is of secondary importance to ensuring that the oil delivered meets the detailed quality parameters set down in the contract.

In the case of crude oil, oil fields become depleted over time. The volume of production, and therefore the volume of trade, declines. This life cycle applies to many benchmark grades. The PRAs have included more and increasingly disparate grades of oil from different locations into the benchmark price discovery database to shore up the volume of oil that supports the established key crude oil benchmarks,8 such as ‘Dubai’ and ‘Brent’. This has been achieved by redefining single grade benchmarks as a range of grades of different oils that can be delivered instead of the headline benchmark grade.

Dubai

Dubai is a long-established benchmark that has been used in the contract price formulae of medium/heavy sour wet grades in the Far East, the Mediterranean and even in Russian Urals contracts, before the latter were sanctioned.

Dubai, now dubbed the Middle East Benchmark basket (‘MEC’), refers to a basket of different grades that may be delivered into the forward contract. The seller agrees to deliver a cargo during the course of a specified forward month. The seller has the option to supply to the buyer one of the five following basket grades:

-

Dubai, Fateh crude loaded offshore Dubai and assessed by Platts as trading in maximum cargo-sized lots of 500,000 bbls for one, two and three forward month contracts (‘M1, M2 and M3’) for cargoes loading M+2, M+3 and M+4. So, in January, what Platts calls M1 refers to March delivery contracts. The contract months roll forward on the first day of each calendar month:

-

Oman loads at Minah al Fahal, south of the Straits of Hormuz and is assessed by Platts in maximum cargo-sized lots of 500,000 bbls in three forward month contracts, M1, M2, and M3, as for Dubai. Parties trading Oman that wish their cargoes to be included in the Platts database must be prepared to accept a cargo of Murban, albeit with a Platts-determined price adjustment. There is a futures contract for Oman, which trades at a fixed price on the Gulf Mercantile Exchange platform. Oman is used as a stand-alone benchmark in medium sour wet cargoes.

-

Upper Zakum, is an Abu Dhabi crude that loads at Zirku Island in the Persian Gulf. It is lighter and slightly less sour than Dubai and tends to trade at a premium in the spot market. Platts assesses the price based on 500,000 bbl cargoes loading in M+2. As for Oman, companies trading Upper Zakum that wish their cargoes to be included in the Platts database must be prepared to accept a cargo of Murban, with a Platts-determined price adjustment.

-

Al Shaheen is loaded from floating storage in the Ultra Large Crude Carriers (ULCCs) ‘Asia’ and ‘Africa’ anchored offshore Qatar. In common with Upper Zakum, Platts assesses the price based on 500,000 bbl cargoes loading in M+2. Companies trading Al Shaheen that wish their cargoes to be included in the Platts database must be prepared to accept a cargo of Murban, with a Platts determined price adjustment; and,

-

Murban, from Abu Dhabi, is a relatively light, low-sulphur grade compared with the other oils in the basket. The Platts assessment reflects cargoes of up to 500,000 bbls loading from Jebel Dhanna in Abu Dhabi or from storage at Fujairah in M1, M2, and M3. Murban sits uneasily in the Dubai basket. Historically, if Murban is delivered into a ‘Dubai’ forward contract, a premium has been assessed by Platts to be applied to the Contract price. This is a condition for acceptance of the deal into the Platts price database. From the beginning of 2026, this adjustment will be based on the difference between Platts Dubai and Platts own independent Murban assessment averaged over the 5 days before publication, so it may be a premium or a discount to Dubai. There is a futures contract for Murban, which trades at a fixed price on the Gulf Mercantile Exchange platform. Left to its own devices, Murban could evolve into a benchmark in its own right.

The price published by the PRA each day refers to the lowest price in the basket on that day.

According to Platts, Upper Zakum was the grade of oil in this basket most regularly declared by sellers in their MOC window in the first 11 months of 2025, followed by Oman and Murban. Declarations of Murban for delivery into the Dubai basket have been on an increasing trend of such declarations since 2023.

Platts assesses the grades in the Dubai basket based on maximum cargo sizes of 500,000bbls. In 2024, 45 per cent of the Dubai basket grades exported went to China, 16 per cent to Japan, and 7 per cent to India. These were not transported in 500,000 bbl cargoes, which would have left dead freight on a typical Aframax tanker, which can load up to 800,000bbls. Typically, cargoes exported to long-haul destinations from the Persian Gulf are shipped in Very Large Crude Carriers (VLCCs), which can carry up to 2.2 million bbls. The larger capacity lowers the unit cost of freight, making VLCCs the more economic option for transporting wet oil. So, a Contract price for a VLCC has to contain some adjustment to reflect that the benchmark contained in the price formula reflects a smaller cargo size than the contract cargo size.

Brent and the Irish Screwdriver

The proverbial Irish Screwdriver is a hammer.

The situation is considerably more complicated when it comes to the ‘Brent’ basket. Brent is the most ubiquitous benchmark12 used in crude oil contracts in the market. This is because there is a range of different contracts and trading mechanisms that have evolved since the 1980s to provide a suite of sophisticated and flexible price discovery and risk management tools, which many major actors in the oil industry are bending over backwards to maintain.

While it is not necessary for those attempting to assess damages in litigation to absorb all the variations in the various Brent contracts, the complexity of this market framework is relevant to the calculation of damages in litigation. When it comes to the question of what is the correct ‘Market’ price or Brent benchmark to compare with a Contract price in calculating damages, each of these contracts may be claimed, rightly or wrongly, to have a role to play.

There is now no actual Brent, or more pedantically, Brent/Ninian Blend, exported from Sullom Voe in the Shetland Islands. The remaining pipeline operator, Enquest, is considering options for re-purposing the infrastructure. Brent is now no more than a brand name.

Buyers of wet oil that use the price of the Brent benchmark as published by the PRA, Platts, in a physical oil Contract price formula, must appreciate that the actual price they are getting is now the lowest of the prices for a basket of grades including Brent, Forties, Oseberg, Ekofisk, Troll or, since June 2023, WTI Midland (WTIM). Increasingly through 2023–25, the Dated Brent benchmark reflects the Platts-assessed price of Forties and WTIM, with the latter gaining ground rapidly.

Any two parties can agree on whatever they choose in their own contracts. But if they want their deal to be included in the Platts benchmark database, they must conform to the Platts criteria.

In its chosen role as the custodian of the world’s most influential crude oil benchmark, Brent, Platts has worked hand in glove with the Intercontinental Exchange (ICE) and Shell International Trading and Supply Company (STASCO), This is a powerful triumvirate that is, arguably, steering the development of price reporting and benchmark development.

ICE states that its WTIM delivery mechanism ‘enables participants to directly price and hedge the marginal domestic barrel of Midland quality crude that meets Platts Midland specifications accepted into Dated Brent. Moreover, it is deliverable in Magellan and Enterprise’s terminals; both are connected to water terminals included in Platts’ approved terminals list’.14

The STASCO general terms and conditions of trade (GTCs)15 define Midland crude oil as ‘Midland means crude oil loaded from the list of terminals that are currently accepted by S&P Global-Platts for inclusion into their respective Dated Brent assessments, the “Midland Load Ports” and meeting the S&P Global-Platts specification at the time of the deal, based on load port shore tank quality’.16

US Gulf Coast (USGC) export terminals have supported the efforts of these big three. Currently, 13 USGC terminals have been approved by Platts for inclusion of cargoes from their pipelines and export terminals into the Platts Brent benchmark price assessment process. In order to gain such approval, cargoes of WTIM oil must meet quality specifications set down by Platts. These specifications are intended to be typical of US Permian basin crude and are quite different from the quality of the WTI that is delivered to Cushing, Oklahoma, under the CME/NYMEX WTI futures contract.

The criteria for acceptance of a terminal by Platts are the ability to:

- Accommodate 700,000-barrel Aframax cargoes with ±1 per cent volume tolerance;

- Load oil whose quality meets Platts WTIM specifications;

- Show full transparency over terminal ownership structure;

- Demonstrate sufficient storage to meet the loading schedule; and

- Verify no receipt directly from any Cushing origin pipeline.

Forties, Oseberg, Ekofisk, and Troll are of different quality to ‘Brent’. When compiling the daily benchmark price quotation, a monthly sulphur price de-escalator is applied to the reported price of Forties and monthly quality premia are added to the prices of Oseberg, Ekofisk, and Troll sold FOB their loading ports. These premia/de-escalators are determined and announced monthly in advance by Platts. Which month’s sulphur de-escalator or quality premium is used depends on the actual or deemed B/L date. So, which party does the deeming can make a measurable difference to the Contract price for cargo deliveries, particularly around the turn of a month.

Historically, when Brent was a single pipeline grade, then called Brent System Crude Oil, one of the tools used to establish the quality component of the price differential between the Brent benchmark and other grades of oil, was to look at the value of the refined products that could be extracted from the physical oil and compare it with the refined products that could be extracted from Brent.

Refining assays, usually obtained by providing samples to a recognized independent laboratory, spell out the quantity and quality of finished and semi-finished products that can be derived from the contract grade under laboratory conditions. This is the starting point for evaluating the Gross Product Worth (GPW) of the contract crude oil.

GPWs are based on the sum of simple refined products yields multiplied by the prices of those refined products that can be derived from the crude oil in question.

The GPW of the physical contract oil is then compared with the GPW of the benchmark oil for which, by definition, a transparent published price exists. From this, a Market price differential for the physical oil may begin to be inferred.

This approach was never a panacea for several reasons, not least of which is that each refinery and each geographic region extracts different amounts of product from the same crude depending on the equipment of the refinery and consumer demand for end products in the region. Furthermore, there is more to price than quality. While a GPW comparison is a reasonable starting point for price differential negotiations, it is not a silver bullet.

However, in the case of the Brent benchmark, on any given day, the published benchmark price may be established, not by Brent, but by one of the other grades in the basket, Forties, Oseberg, Ekofisk, Troll, or WTIM. So, the GPW methodology attempts to solve two simultaneous equations with two unknowns: the GPW of the contract oil and the GPW of any one of six basket grades, all of very different quality, all with different refining assays.

Usually, this difficulty is addressed by performing a GPW comparison between the physical oil being evaluated and a different, more established, physical oil for which the price differential, G, to the Brent benchmark is known. The market price differential to Brent for the more established physical oil, it is hoped, will have been tested in the market over time. If the market for that established grade is limited either in volume or in the number of companies trading it, inserting its market price differential into the formula price for a different grade will merely perpetuate any inaccuracy.

In practice, this GPW method of establishing the quality component of the grade differential, G, to the benchmark price, A, does not feature in routine Contract price negotiations. It is too cumbersome, time-consuming, and subjective to help in a fast-moving market. It is usually confined to the negotiation of the Contract price of new grades of crude oil that have not yet found their place in the market.

Delivery location and freight

Platts started assessing the price of Brent basket grades delivered to Rotterdam in 2016. To boost the pool of transactions, or indications, that form the daily Dated Brent published price assessment, cargoes of these grades delivered CIF Rotterdam have been included in the Platts Brent database since 2019.

These CIF prices are adjusted by the PRA to net them back to an FOB North Sea basis using a freight adjustment factor (FAF). FAF is a 10-day rolling average of the North Sea to Rotterdam freight, calculated as explained below under the heading, ‘Freight’.

What we call ‘Brent’ now predominantly reflects WTIM delivered to Rotterdam and netted back to the North Sea. To achieve this, some precise rules have been introduced by the PRAs in their price assessments to shoehorn WTIM into this new Brent model.

What is WTI?

WTI, in particular the CME/NYMEX futures contract, has been a pricing benchmark in its own right since the 1980s. This very active futures contract has always been a pipeline contract deliverable inland in lots of 1000 barrels (‘bbls’) at Cushing, Oklahoma. But since the repeal of the US Congress ban on the export of domestic oil in 2015 and the increase in US production from about 13 million b/d in 2015 to about an estimated 20 million b/d in 2024, WTI has taken a different role in world trade and the price discovery process.

It is necessary to be precise about what is meant by WTI and WTIM. As mentioned above, the futures contract uses WTI delivered to Cushing as the underlying commodity, but WTIM is also gathered and traded at Magellan East Houston (MEH) and at Midland, Texas. It can be exported from an increasing number of locations along the USGC, including from Corpus Christi and from the Louisiana Offshore Oil Port (LOOP).

Cargo size

It would be most economically efficient to export WTIM to Europe or further afield to the Far East in big tankers such as VLCCs, which can transport up to 2.2 million bbls. This would bring down the unit cost of freight: usually, the larger the tanker, the lower the per-barrel cost of freight, as already mentioned in connection with long-haul freight from the Persian Gulf.

Brent started life trading in the 1980s, initially in cargo lots of about 500,000 bbls. This was in line with the Sullom Voe terminal lifting agreements between producers, represented by field operators, and the terminal and pipeline operators, then BP and Shell. This was increased to 600,000 bbls in 2016 when CIF Rotterdam cargoes began to be assessed and published by Platts and netted back to a North Sea FOB equivalent to boost the number of cargoes informing the Platts Brent database.

The inclusion in 2019 of North Sea grades in the Brent basket that were sold CIF Rotterdam, rather than FOB the loading terminal, was the first step in a process of guiding the Brent benchmark towards including oil from further afield than the North Sea in the future. This is an ongoing process, and the contents of the current basket are unlikely to remain constant going forward.

Since the inclusion of WTIM in the Brent basket in 2023, the ‘Brent’ contracts now specify a cargo size of 700,000 bbls. The North Sea terminals initially accommodated this increase in size without too much fuss, but there is some discomfort emerging as a result of the change. This is because the underlying physical oil production and transportation contracts have evolved in the North Sea over the last 40–50 years with little regard for the needs or preferences of the trading departments of the oil companies or of the wider oil trading community. These logistical deals started life to fulfil the needs of oil producers of varying size and influence.

Upstream, at the oil field ownership and operating end of the business, individual field operators have over time entered into transportation agreements and have signed lifting procedures with pipelines and terminals, usually on behalf of a number of joint venture partners. The rules which the field operator must observe in protecting and enforcing the interests of joint venture partners are usually set down in a Joint Operating Agreement (JOA) relevant to the field or licence in question. The transportation and pipeline operators are not parties to the JOAs.

Field operators and pipeline/terminal operators can do just about anything they deem necessary for safety or other operational reasons, such as berth/jetty constraints, storage limits, etc. However, it is difficult to argue that changing the minimum cargo size that can be loaded at a North Sea terminal to 700,000 bbls to accommodate the inclusion of WTIM into the Brent basket is anything other than a commercial decision. This decision can be prejudicial to the interests of the smaller joint venture partners. These have nothing more to protect them than their minority vote in joint operating committee meetings.

The larger oil companies that produce oil at North Sea terminals are not vocal on this issue. Typically, they have access to sufficient barrels to adjust to the larger cargo size, which they prefer anyway because it facilitates their participation in the 30-day market. Most are active risk managers and can hedge any differences they might perceive between the benchmark price applicable to any later delivery dates that accompany larger cargoes. In reality, this is not an issue that enters into the thinking of major players.

However, for smaller companies, the increase in the minimum cargo size has significant cash flow and price risk implications. For example, a producer of 3,000 b/d may expect to lift a cargo of 600,000 bbls accrued over 200 days. Increasing the minimum cargo size to 700,000 bbls means it would have to wait a further 33 days to lift its oil. A lot can happen in the market in that time. The relationship between price and delivery date has already been discussed above.

These minority producers tend not to be contracted directly with the terminal or pipeline operators, but with their own field operator and JOA partners. To appease these minority partners, ultimately, the field operators might well be put to seek proof from the terminal operators that the increase in the minimum cargo was put in place for safety or operational reasons. It is unlikely that it would be believed that the increase in cargo size at the same time that WTIM was included in the Brent basket, with the change in the standard size in the 30-day market, was no more than coincidence.

If the terminal operators had simply allowed 700,000 bbls cargoes to be nominated and loaded but continued to accommodate the occasional smaller cargo from minority producers without sticking rigidly to 700,000 bbls as a minimum, this difficulty would not arise. But this is not the stance taken by all of the terminals relevant to the Brent basket.

Other North Sea terminals, where the oil is not included in the Brent basket, such as Flotta Gold, Duc, Grane, or Johann Sverdrup, continue to permit cargoes smaller than 700,000 bbls. Platts continues to assess these grades based on their assumed cargo size of 600,000 bbls.

Even with the increased North Sea cargo size to 700,000bbls, there remain drawbacks from including WTIM in the Brent basket. The 700,000 bbls cargo size is sub-optimal for transatlantic voyages. Transport can be made in, usually more expensive, Aframax tankers rather than the logical VLCC choice. Alternatively, a tanker charterer delivering WTIM into the Brent basket could in theory decide to use a VLCC anyway and incur dead freight costs on a larger tanker by sailing partly laden with only 700,000 bbls onboard. This is unlikely for economic reasons. So, the charterer may have to organise two port loadings and/or discharges or other non-standard contractual arrangements with other shippers to ensure that their cargoes can be delivered into the Brent complex.

Platts dictates currently that ‘sellers may deliver from an Aframax that has performed a ship-to-ship transfer from a larger vessel provided all the oil on board that vessel has demonstrably loaded at a single Platts-approved US Gulf Coast terminal’. Not all of the Platts-approved USGC terminals can accommodate VLCCs. In practice, VLCCs actually can load from more than one terminal. Platts intends to remove the single terminal loading provision from May 2026.

From May 2026, Platts proposes ‘to remove the single terminal origin requirement for WTI Midland supplied via ship-to-ship transfer with a larger vessel in the Dated Brent assessment process. Under the proposal, Platts would expect all parcels on board the larger vessel to:

- Be carried in segregated cargo tanks and have separate Bills of Lading.

- Meet Platts’ global WTI Midland specification.

- Have demonstrably loaded from one, or a combination of, US Gulf Coast Terminals approved by Platts.

- Existing methodology around quantity, quality and deviation would remain unchanged with respect to final delivery on an Aframax.

This will make it considerably easier to break bulk in a transatlantic VLCC to produce 30-day Brent contract-sized cargoes of WTIM. So, arguably, it was unnecessary to increase the Brent cargo size to 700,000 bbls to improve freight economics for WTIM. In theory, now the contract could revert to 600,000 bbls. But once the eggs have been scrambled, it is difficult to get them back in their shell. So, this is unlikely to happen.

Sailing time

Once the WTIM price is assessed by the PRAs delivered to Rotterdam, it is netted back to an FOB North Sea basis in the same way as CIF delivered cargoes of the other basket grades. Platts assumes that contracts for the FOB basket grades in the North Sea reflect a price averaging period of 2-1-2 around the B/L. So, for CIF deliveries, a commensurate adjustment is made to the 2-1-2 price averaging period around a deemed B/l. This deemed B/L reflects a 1–2 days sailing time from the North Sea to the continent.

In the case of WTIM, this adjustment is a bit more complicated.

Rolling schedules versus monthly schedules

The North Sea has historically scheduled its cargo liftings from the various shared terminals on a monthly cycle. WTIM had hitherto operated on a rolling basis with liftings agreed ad hoc between producers and the various pipeline/terminal operators.

In the North Sea, the producers nominate their preferred cargo lifting dates in month M to the terminal operator usually by about 20–25th M-2. The allocation of cargoes to individual lifters by the terminal operator is determined by the last day of M-2.

This process has become earlier and earlier over the years to fit with the market’s need to comply with the notice period that a seller must give a buyer before delivering a forward Brent contract. This was initially 15 days, then increased to 20 days, then to 21 days, and now to 30 days. The North Sea terminal operators have repeatedly amended their cargo scheduling timetable to comply with the needs of the forward Brent market.

The Brent forward contract, sometimes referred to as ‘cash’ Brent, allows a buyer and seller to trade a Brent cargo for delivery at any time during a specified future month up to several years ahead. The seller must tell the buyer which of the grades in the Brent basket—Brent, Forties, Oseberg, Ekofisk, Troll, or WTIM—it will deliver and on which 3-day delivery date range in the specified month it will deliver it, by 30 days before the first day of that particular delivery date range. So, to ensure that the first physical cargo loaded in month M can be delivered into the forward contract for month M, the schedule of liftings must be known at least 30 days before 1st–3rd Month M.

STASCO’s GTCs for BFOETM state that the cargo declaration deadline for FOB grades is defined as ‘The FOB Last Day of Nomination shall be One Full Month prior to the first day of the Laydays, where One Full Month is defined as the number of calendar days in the month prior to the Specified Month.’ If the seller is a prime supplier, usually a producer, the deadline is 2 pm London time, but otherwise this must be done not one second later than 4 pm London time.

This timetable does not sit easily with the rolling date ranges employed, and historically kept confidential, by USGC terminals sitting 2–3 weeks away from Europe.

Platts initially assumed that it takes 17 days to cross the Atlantic from the USGC to Rotterdam. That is the case for a speed of about 12.5 knots, but the time can be pared down to 15 days at 14 knots or extended to 21 days at the environmentally friendlier rate of 10 knots. STASCO assumes a voyage time of 17 days. It seems likely that Platts will increase its sailing time assumption to 19 days too when it updates its price assessment methodology in May 2026.

While North Sea cargo schedules are freely available and individual cargoes are tracked assiduously, it is the first supplier of a WTIM cargo into the 30-day market that assigns the cargo a number for declaration purposes.

It has been very difficult to track how many cargoes of all grades are potentially deliverable into the Brent cash contract, because the WTIM cargo scheduling timetable marches to a different drum than the North Sea FOB grades. To declare a Midland cargo into the 30-day contract, STASCO specifies that ‘the Loading Terminal Authority must publish an official document stating the official Laydays of the Midland Cargo and Seller shall provide Buyer with Evidence of this at the time the Seller declares a Midland cargo to Buyer.’ The fact that this only happens when the cargo enters the 30-day supply chain, and not when it is scheduled publicly in advance to sail from the USGC, leaves some ambiguity as to how many cargoes of all the relevant basket grades are eligible for delivery into the 30-day market. This is a significant unknown in traders’ analysis of the 30-day price.

The trader selling a WTIM cargo has considerable flexibility to speed up or slow down cargoes coming from the USGC to allow them to be delivered into an earlier or later month cash 30-day contract. The buyer is supposed to be included in any discussion of amendment to the Midland loading date range for the purposes of making a cargo eligible for the 30-day market. If this does not happen, the seller acquires valuable optionality to profit from the slope of the forward oil price curve.

Freight

As mentioned above, the prices of North Sea basket grades that are sold CIF Rotterdam are adjusted by the PRA to net them back to an FOB North Sea basis using a freight adjustment factor (FAF). WTIM cargoes delivered CIF Rotterdam find their way into the Platts Brent price database similarly by netting back the CIF price to an FOB North Sea basis by Platts, assuming one day’s sailing time from Rotterdam to the North Sea. The WTIM cargo is not actually transported back to any point in the North Sea. Rather, its CIF price is adjusted to a North Sea basis by the Platts FAF.

The FAF that Platts applies to CIF North Sea basket grades is calculated on the basis of the Worldwide Tanker Nominal Freight Scale, dubbed Worldscale (WS), flat rate, or WS100, published annually for voyages between the relevant North Sea ports and Rotterdam. The WS 100 rate for a given year reflects a standard reference voyage for a standard tanker between each of two ports. This is analogous to a benchmark price.

The actual freight rates agreed between charterers and owners during the course of the WS year is agreed at the time any individual charterparty is agreed and reflect market conditions at that time. The rate agreed is often, but not always, expressed as a percentage of the WS100 rate. This is analogous to the grade differential for oil cargoes.

In netting back CIF Brent basket prices to a North Sea basis, Platts uses the WS 100 rate for each terminal, analogous to the benchmark, A, adjusted for the freight rates assessed by Platts on a rolling basis, averaged over the previous 10 days, analogous to the differential, G.

In the case of CIF WTIM, the benchmark WS 100 rate to which this rolling average is applied is a volume-weighted average of other basket grades’ WS100 flat rates.

Conclusion

Often lawyers, and almost always judges and arbitrators, want the appointed experts to produce a straightforward single number, or at least a narrow range of prices, relevant to the calculation of damages in an oil trading dispute. Simply using a published unadjusted benchmark as a proxy for the Market price and comparing that with the Contract price is misleading and inaccurate.

This article has described the most regularly quoted and employed method of establishing publishable benchmark prices used by oil companies and traders, namely Platts published prices.

The message to be conveyed is that Platts, and its MOC e-window in particular, is not ‘the Market’. Nor does it purport to be, although it is often easier for parties to a dispute to imply that it is when calculating damages in litigation. Benchmark prices are often part of a Contract price formula for physical, “wet”’ cargoes. But very little oil, if any, changes hands at the benchmark price, so care should be taken if this is put forward as the Market price in calculating quantum.

If a benchmark is used as a proxy for Market price in the calculation of damages, a detailed comparison must be made between the attributes of the benchmark compared with the cargo in dispute. This will include close and detailed examination of:

- The contract formula price and the benchmark price averaging period specified in the formula;

- The delivery date, particularly if there is any opportunity to alter the delivery date range by influencing tanker speed;

- The date on which the deal is transacted relative to the peak trading period for the oil in question,

- The cargo size relative to the tanker size and the impact on freight costs;

- The delivery location;

- The type and quality of contract oil; and

- Any other attributes such as optionality in delivery date and/or price averaging period, sanctions and destination restrictions, non-standard credit terms, etc. that have an influence on price.

Pity the poor expert required to conjure up quickly a single number that reflects the difference between the Market price and the Contract price when all these factors have to be considered. It is unwise to delay consulting an expert until the case preparation has become too far advanced. But, as a practising independent expert, you may think that I would say that, wouldn’t I?

Original article l KeyFacts Energy Energy Industry Directory: Consilience Energy Advisory Group