By Catherine McBride, OBE

Why the North Sea is not a spent resource, and exported oil still benefits the UK

Last week, the former Green Party MP, Caroline Lucas, demonstrated on Good Morning Britain how little she knows about energy, trade, and oil and gas production. The Green Party is so proud of this exchange that they clipped it and posted it on X. Another commentator has posted a longer clip.

So what needs rebutting:

Myth 1. It’s not worth recovering because ‘we export 80% of the oil’

GMB presenter: ‘what we do get out, we export 80% of...’

Lucas: ‘Exactly because the oil, for example, that we get out is not the kind of oil we use in our refineries. So it’s not going to do anything.’

Lucas and Garaway will no doubt be surprised to learn that 80% of the cars produced in the UK are also exported. Car exports provide many skilled jobs in the UK, both directly and indirectly through the production of materials, parts, and services, as well as providing tax and export revenue. Which is probably why no sane person has ever claimed on breakfast television that the UK should stop producing cars because ‘we will only export them’.

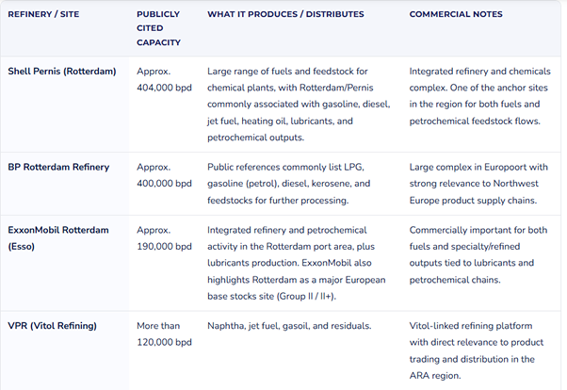

It is true that companies operating on the UK side of the North Sea do ‘export’ about 80% of the crude oil they extract to refineries in Rotterdam, Poland and Germany. This is probably because Rotterdam has a larger refining capacity than the entire UK; Rotterdam refineries are the largest and most modern in Europe and are configured to refine light, sweet crude efficiently as well as other crude grades. The majority of UK North Sea production is light sweet crude. Incidentally, the two largest refineries in Rotterdam are owned by Shell and BP, both UK companies. They refine about 400,000 barrels a day each, while the largest UK refinery refines only 270,000. So this isn’t quite the ‘export’ the Greens like to imply, more of an internal company transfer, and a lot of the resulting refined products: petrol, diesel and jet fuel, will come back to the UK, and some will be sold in Shell and BP service stations.

The four main Rotterdam refineries

Polish refineries are now the UK oil company’s second-largest customers, following Poland’s suspension of imports of Russian crude via the Druzhba pipeline. Poland’s refineries are state-owned, a legacy of Poland’s Soviet past, which allows them to circumvent the EU’s state aid rules, but the Polish government believes that refining capacity is a national security asset, so its refineries operate on narrow margins. I wonder if Lucas would prefer that Poland continue to import Russian oil instead?

At least 60 countries have introduced emergency measures due to fuel shortages caused by the closure of the Strait of Hormuz and by damage to LNG plants and refineries in Bahrain and Qatar. Only the UK’s smug middle-class ‘Greens’ would object to exporting oil to these countries. But no doubt the same Greens will organise a charity concert for them after their populations are starving and unemployed.

Myth 2. The North Sea ‘is a declining basin’

Lucas: ‘We don’t have 100s of years’ worth of oil and gas left in the North Sea, it is a declining basin’ and ‘In spite of all the licences that have been given out over the last 14 years or so, we are still getting a tiny amount from the North Sea.’

Interestingly, according to the UK’s trade data, Norway is the largest supplier of crude oil to UK refineries, accounting for about 40% of UK crude imports. Obviously, the North Sea cannot be the ‘declining basin’ the Greens like to claim if the Norwegian side is supplying 40% of UK oil imports and 75% on UK gas imports. According to the Norwegian Offshore Directorate, in 2025, there were 21 new oil and gas discoveries across the Norwegian shelf, totalling 424 million barrels of recoverable oil and gas. About two-thirds of these were new oil fields, and one-third were new gas fields. There was also a new discovery in January 2026 with up to 4.5 million cubic metres of recoverable oil equivalent. This is hardly a declining basin.

The difference between the UK and Norwegian sides of the North Sea is that the Norwegian government encourages oil and gas exploration and development, while the UK government seeks to prevent it. UK production has been declining since the Windfall Tax was introduced, which increased the total tax rate on oil and gas companies to 78%. It shouldn’t surprise anyone that companies are choosing to keep their oil under the UK side of the North Sea and focus on their production in other parts of the world.

Myth 3. The purpose of production is to lower prices

Lucas: ‘We need to knock on the head the idea that drilling more oil and gas is going to get our own prices down, our own fuel prices down,… because it is sold on international markets at global prices, so it doesn’t do anything for our own prices.

Just like oil companies, car companies are private companies, and if they want to invest in plant and equipment in the UK, they are free to do so, and if they can make more vehicles than needed or wanted by UK consumers, they are free to export cars to countries where consumers do want to buy them. This really isn’t rocket science.

Not only does the UK export 80% of the cars it produces, 85% of cars purchased in the UK are also imported. So, the car market resembles the oil market more than people may imagine. Consumers buy the cars they want, need or prefer, just as oil refineries buy the oil that suits their refinery’s configuration and production.

North Sea oil is produced by private, mostly listed companies, and, like all listed businesses, they have a fiduciary duty to maximise their profits. So, if refineries in Rotterdam are willing to pay more for UK oil than UK refineries are, UK producers will sell to them. If oil production companies also own refineries in Rotterdam, such as BP and Shell, they are even more likely to sell their oil to them, though they are not obliged to do so. Crude sales are determined by grade and end product demand. For example, if a UK refinery has clients who need bitumen, it will buy heavy sour crude oil to produce bitumen. This crude will probably be imported from Saudi Arabia, Mexico, or, possibly, Venezuela.

This is why people trade: to get the products they need or want at a price they can afford. Trade is determined by importer demand. But importantly, imports are paid for by exports. Producing cars, aircraft parts, chemicals, pharmaceuticals, and oil for export helps the UK’s trade balance. However, the UK is still running a trade deficit, which could be reduced if it develops new oil production.

Gas is completely different: the UK can only export gas to countries connected to it by pipeline; the UK does not have a plant to convert natural gas to LNG, as I have explained many times. You can read about it here. But producing more gas in the North Sea does increase UK gas security and reduce the UK’s need to import gas from Norway or LNG from the US. This also helps the UK’s trade balance. But if US LNG is cheaper than UK natural gas because the US keeps finding and opening new wells, don’t be surprised if the UK keeps importing it.

Myth 4. Energy security will come from renewables

Lucas: ‘if we want to get more energy sovereignty, we need to be going even more for the renewables,’ and energy security is ‘done more cheaply and more effectively through renewables,’

Like so many people, Lucas is confusing energy with electricity. They are not the same things. Three-quarters of the UK’s energy needs are supplied by oil, gas, and coal. Renewables only supply electricity, mostly intermittently, so they also need backup electricity made from gas. Energy sovereignty or energy security will not come from more renewables, and renewables are not cheaper.

Renewable electricity cannot supply petrol, diesel, jet fuel, bunker fuel, heating oil, bitumen, carbon fibres, or chemical feedstocks for plastics, fertilisers, and pharmaceuticals, or the industrial heat needed to produce cement, ceramics, glass, steel, or aluminium.

Renewable intermittent electricity is heavily subsidised, but also requires stand-by backup power. Intermittent electricity increases the cost of balancing the grid, as it is unpredictable, requiring curtailment payments when the wind is too strong or there is too much solar electricity. Solar is difficult to curtail; so other suppliers are required to shut down. Intermittent electricity also increases the Transmission Network Use of System costs, as wind turbines are often located far from demand centres.

It is a beautiful, sunny day today, 19th April 2026, but at 6 pm, only 9.4% of UK electricity is coming from solar, 11.8% from wind, 28.9% from gas, and 22.1% from continental Europe. In an hour, gas will have to be ramped up to replace all the solar and to cover the additional demand from people turning on their lights.

Myth 5. If the new fields can’t supply total UK demand, they shouldn’t be allowed to supply any

Lucas: ‘new fields like Jackdaw and Rosebank will take years to come online,’ and ‘All of the new fields licences given out by the Conservatives will only produce 6 months of UK gas demand’

Jackdaw was granted permission in 2022 and was preparing for production by Q3 of 2025, but its permission was called into review in January of that year. If Ed Miliband supports the project, they could be in production very quickly as Shell has already drilled the wells, installed a platform support structure and laid a ‘tie-back’ pipeline to Shell’s Shearwater site. So, the physical production was over 90% complete. However, production could be delayed by UK Red tape: the requirement to resubmit their updated environmental assessment, triggering new statutory consultation before receiving approval from the North Sea Transition Authority. It is no surprise that oil and gas companies are fed up with dealing with the UK. It is hard to believe there is an international gas shortage due to damage to the Qatari LNG plant when you read about the UK gas approval processes. But if the Jackdaw site does take ‘years to come online’, this is entirely down to UK politicians and green activists, not to any structural issues.

But why does Lucas claim that the new fields would only supply 6 months of UK demand, and so there is no point in allowing them? This statistic is false. It comes from ‘Uplift’, an activist group hell-bent on closing down North Sea oil and gas (from their nice warm office). Uplift apparently only counted the gas licences approved in the 33rd licence round, then claimed these licences would produce only 40 to 50 bcm of gas, when the UK uses 75 bcm annually. The North Sea Transition Authority (NSTA) believes the new fields from the 33rd licensing round would supply 12 to 18 months of UK demand, and this is from only one licensing round. NSTA believes there are reverse of between 560 and 1000 bcm remaining in the UK continental shelf.

But regardless of the amount of reserves, if a private company wants to buy a licence to explore the UK’s continental shelf for oil and gas reserves and then is willing to pay the UK 78% tax on its profits, why would we want to stop this? We don’t subsidise oil and gas companies, unlike wind and solar production. So, where is the downside?

There are 106 companies in the Oil and Gas Producers sector listed on the London Stock Exchange (LSE), according to the Barclays Smart Investor sector list. These range from massive vertically integrated companies such as Shell and BP, smaller North Sea independent producers such as Harbour Energy, and small-cap explorers and AIM-listed firms. This number includes nine major producers with dual listing on the LSE, such as TotalEnergies, Equinor, Eni, Marathon Petroleum, Occidental Petroleum and Repsol. There are also companies in related sectors, such as Oil Equipment and Services, Pipeline Operators, and Refiners & Petrochemical Companies, listed on the LSE. In total, 362 companies in the oil and gas industry are listed on the LSE. Even if the companies export the oil they find, UK investors benefit. If the companies are UK tax residents, as BP and Shell are, they will pay corporation tax on their worldwide profits. Only smug middle-class greens would want to limit this industry.

The UK needs oil and gas and will buy it from somewhere, so why not produce it? Even if the oil produced is exported, the UK still gains employment, licence fees, and tax revenue. It would also help our trade balance. If we don’t export it but use it domestically, it will reduce UK imports and again help the UK’s trade balance.

But the idea that we should not allow a company to mine in the North Sea because we don’t think there is enough to provide all of the UK’s gas demand is bonkers. The UK currently has about 80 producing gas fields – none of them provides all of the UK’s needs, but together they provide half of it. Why would we not allow more companies to add to this supply?

Myth 6. UK oil and gas production is harmful to the environment, but imported oil and gas isn’t

Lucas’s on climate change: ‘There is a real risk of all kinds of shortages and all kinds of vulnerability because of what we are doing to our global environment.’

The only difference between the emissions from domestic oil and gas production and imported oil and gas is the emissions accounting standards set by the United Nations Framework Convention on Climate Change (UNFCCC) and the Intergovernmental Panel on Climate Change (IPCC), which established the rules for how and what is counted as part of a country’s territorial emissions. The UK has only done 3 things that made a difference to its territorial CO2 emissions:

- It replaced coal-fired electricity with gas-fired electricity, halving emissions.

- It reduced its methane emissions from the waste management sector by 71% between 1990 and 2019[1] by improvements in landfill standards, changes in the types of waste sent to landfills, and increased use of landfill methane for energy.

- It deindustrialised by taxing and regulating emission-intensive industries, prompting them to move their manufacturing out of the UK. The UK continued to import the goods it used to make, resulting in 180 million tonnes of CO2 emissions in 2023, but these emissions are not counted as UK emissions by the UNFCCC.

For Lucas to claim to be worried about climate change while the UK continues to import goods that emit 180 million tonnes of CO2 somewhere else is untenable. Since 2019, the UK has lost between 150,000 and 200,000 industrial jobs due to deindustrialisation and high energy prices, with the steepest declines in energy-intensive sectors such as steel, chemicals, ceramics and paper. But soon, if Lucas and her ilk have their way, thousands of oil and gas workers will be joining them.

Global emissions have increased by over a trillion tonnes since 1990. UK territorial emission reductions total just 290 million if we exclude UK imported emissions and pretend UK emission reductions are real. This is just 0.03% of the global increase. Lucas is very wrong to talk about shortages and vulnerabilities because of what we are doing to our global environment.’

‘We’? The UK has not produced an additional trillion tonnes of CO2 emissions since 1990. ‘We’ are not the problem, nor, I suspect, are CO2 emissions – if they were, the massive increase should have made the harms very obvious by now.

The rest of the world has moved on. Even Germany’s Minister for energy and economy, Katherina Reiche, told a major oil and gas conference, CERAWeek in Texas, that the European Union should loosen its “rigid” adherence to climate neutrality and allow itself to miss its 2050 net-zero goal by up to 10%. Reiche stressed that economic growth must come before green targets, stating correctly that Germany and Europe can’t afford to lose their energy-intensive industries. She also told the Texas audience that Germany should drill for fossil fuels in the North Sea, saying: “We have a gas field in the North Sea, which we don’t want to explore. I think we can’t stick to this attitude. We have to also go into our own reserves.” To back this up, Reiche has unveiled plans to build new gas power plants, scrap Germany’s gas boiler phaseout, remove subsidies for rooftop solar panels, and deprioritise the connection of renewables to the country’s power grid.

It is time for the UK and the Green Party to move on as well.

For more information about how Net Zero is measured, the potential of the North Sea to provide the UK with energy security, employment and tax revenue, read the Great British Business Council’s paper, Premeditated Industrial Destruction.

[1] BEIS, Feb 2021, 2019 UK Greenhouse Gas Emissions, Final Figures

Catherine McBride, OBE

Catherine McBride is an economist specialising in trade. Catherine received her OBE for her work explaining economics and trade to both politicians and the public. Before working in trade policy, she was a derivatives trader covering global commodity markets from London. Catherine has written several think tank papers on economics, trade, and taxes; writes a Substack, Catherine McBride’s Substack; writes for the websites Briefings for Britain, Global Britain, and The Critic; and regularly appears on TV, radio, and podcasts.

Original article l KeyFacts Energy: Commentary