By Oberon Houston, Oil & Gas Investment Banking

The rise and fall of Hurricane Energy offers one of the most revealing case studies in modern upstream oil & gas investing. At first glance, the company appears to represent a familiar narrative: a technically ambitious exploration company that attracted substantial investor enthusiasm before ultimately disappointing on reservoir performance. Viewed through the lens of fund management, however, Hurricane’s history reveals something far more sophisticated and instructive.

Over nearly a decade as a listed company, Hurricane became a laboratory for several distinct forms of deployed capital:

- major oil company securing offtake via participation in the IPO

- speculative public-market capital

- specialist technical private equity capital

- activist distressed investing and residual-value monetisation.

Most importantly, the Hurricane story demonstrates that realised investment outcomes in upstream oil and gas are often determined less by the ultimate fate of the field itself than (i) when capital is deployed relative to key technical information events, and (ii) how investors manage their holding when reserve downgrades materially impact valuation.

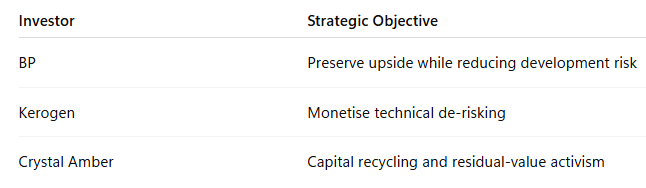

Three very different investors illustrate this dynamic particularly well: BP, Crystal Amber Fund, and Kerogen Capital. Each interacted with Hurricane Energy differently. Each faced different forms of geological and financial risk and managed them accordingly.

Origins of Hurricane Energy

Hurricane Energy was founded in 2005 to pursue a controversial geological thesis: that naturally fractured basement rocks west of Shetland could produce oil commercially at scale.

This was highly unconventional. Most North Sea production historically came from conventional sedimentary reservoirs. Hurricane instead focused on fractured basement reservoirs, particularly the Lancaster Field, discovered by Shell in 1974.

Given the unconventional nature of the reservoir and the uncertainties inherent in fractured basement fields, Shell chose not to progress the Lancaster discovery into development.

This would become the first important capital-allocation lesson in the Hurricane story.

IPO: Public Markets Capitalise Geological Narrative

Hurricane floated on AIM in February 2014 at an implied market capitalisation of approximately £272 million. This occurred before Lancaster had been commercially validated, meaning investors were effectively valuing the high upside potential of the acreage against the substantial uncertainty associated with the reserves. In order to secure the crude offtake, BP also participated in the IPO.

The market’s willingness to capitalise the fractured basement thesis reflected broader conditions in London E&P markets at the time:

- strong appetite for frontier concepts

- low interest rates

- and investor willingness to fund technically ambitious independent explorers.

Crystal Amber: Early Speculative Capital

One of the earliest and most committed institutional investors to build a strategic public-market position in Hurricane Energy was Crystal Amber.

Crystal Amber crossed the 3% disclosure threshold on 21 November 2014, shortly after Hurricane’s first year as a listed company, and continued to accumulate its position during a prolonged weak trading phase materially below the IPO price. The eventual economics of Crystal Amber’s investment therefore depended not on the 43p IPO valuation, but on a significantly lower blended acquisition cost established during a period of market scepticism.

Kerogen Capital: Specialist Technical Capital

The defining event in Hurricane’s corporate history occurred in April 2016, when Kerogen materially participated in a large placing that enabled Hurricane to drill a Lancaster appraisal well.

Crucially, unlike Crystal Amber’s earlier speculative accumulation, Kerogen’s investment was directly tied to a clearly defined technical catalyst: appraisal drilling and testing intended to de-risk a future development. This placing funded Hurricane’s transition from speculative geological concept to apparent commercial validation.

This distinction is critical.

Although Crystal Amber also participated in the raise, it did so to a lesser extent and had already invested materially before a clearly defined technical catalyst existed. Kerogen, by contrast, invested specifically into the catalyst itself. That made Kerogen’s investment fundamentally different in both risk profile and likely intended monetisation strategy.

When the placing was announced with the associated appraisal well work program, Hurricane's share price jumped significantly. BP exited their position at this point.

Appraisal Success and Institutional Validation

Initially, events developed positively. Between 2016 and 2018, Hurricane achieved a series of operational milestones:

- successful appraisal wells

- high-impact flow tests

- Lancaster development progress

- and increasing institutional validation.

In 2018, Spirit Energy farmed into the Greater Warwick Area assets, providing further external validation. As a result, the market increasingly interpreted Hurricane not as a speculative explorer, but as a future producing company with potentially basin-scale upside.

This drove a major rerating. Hurricane’s shares rose from 20p to peaks above 60p during 2018. Importantly, this rerating phase represented the principal value-creation window for many investors.

Kerogen Partially Monetises

As Hurricane rerated amid appraisal success, development progress, and first-oil optimism, Kerogen reduced its holding. Based on public disclosures and reconstructed economics, Kerogen appears to have recovered its original investment and generated an approximate 10% return. The realised return may have been somewhat higher, but the critical point is that Kerogen monetised much of its exposure before Hurricane’s long-term reservoir thesis fully deteriorated.

This is an extremely important distinction.

Kerogen’s investment may therefore be interpreted as a successful catalyst-driven strategy that generated returns while still retaining some speculative upside exposure. Despite the eventual disappointment of Hurricane’s flagship Lancaster Field, Kerogen was able to participate in a high-risk opportunity without full exposure to that risk.

First Oil and the Beginning of the End

In June 2019, Hurricane achieved first oil from Lancaster via the Aoka Mizu FPSO. Operationally, this was a major milestone. The market viewed the arrival of the FPSO as validation of the fractured basement reservoir thesis.

However, it was not long before concerns surrounding reservoir quality proved justified, as water soon appeared in the production stream.

In early 2020, Hurricane announced a severe reserve downgrade. The market reaction was catastrophic and the share price collapsed.

Crystal Amber’s Distressed Activist Re-Entry

One of the most fascinating aspects of the Hurricane story is what happened next.

Rather than abandoning the company following the reserve downgrade, Crystal Amber aggressively rebuilt its position, but from a dramatically lower share price. At this stage, Crystal Amber’s investment thesis had fundamentally changed. The fund was no longer underwriting basin-scale upside or future production growth.

Instead, the thesis had become one of activist residual-value preservation, restructuring influence, and monetisation of the remaining producing assets. This was now fundamentally a distressed-value investment strategy.

Prax Acquisition and Final Monetisation

In 2023, Hurricane agreed to a take-private acquisition by Prax Group. The final headline value was approximately 6p/share, plus contingent upside through DCUs.

While a precise reconstruction of all acquisition and disposal prices is not possible using public disclosures alone, the available evidence strongly suggests that Crystal Amber likely generated a positive overall realised return across the full Hurricane lifecycle despite being aboard for the entire roller-coaster journey.

This is highly significant because it contradicts the simplistic assumption that all Hurricane investors necessarily lost money following the reserve downgrade.

The Three Capital Models

The Hurricane story ultimately reveals three distinct models of upstream capital allocation.

BP: IPO participation for associated business

BP secured the crude offtake agreement by participating in the IPO. Although the gains from this turned-out to be modest, had the fractured basement concept worked, it could have been much more lucrative. It was also interesting that BP, a technically competent shareholder, exited its position once the placing to drill the appraisal well was announced, which lifted the price. It could be argued that they should have waited until the appraisal well results were announced and the share price multiplied as this well was drilled as a crestal producer and had a high chance of being successful, which it was.

Kerogen: Technical Catalyst Capital

Kerogen deployed specialist upstream private-equity capital directly into:

- appraisal activity

- producer wells

- and technical de-risking.

Its monetisation window was likely the rerating associated with institutional validation.

Crystal Amber: Multi-Phase Public-Market Capital

Crystal Amber evolved through multiple investment identities:

- speculative accumulation

- conviction participation

- rerating monetisation

- distressed activist re-entry

- and residual-value monetisation.

This is what makes the fund’s involvement so intellectually interesting.

Crystal Amber was not merely an early speculative investor or a trapped long-term shareholder. Instead, it appears to have actively recycled capital across multiple stages of Hurricane’s corporate lifecycle.

Lessons for Fund Managers

Hurricane Energy offers several important lessons for upstream oil & gas investors.

1. Timing Relative to Technical Catalysts Matters More Than Narrative

The principal value-creation event may occur during appraisal, validation, or rerating rather than during ultimate long-term field development.

2. Different Forms of Capital Optimise for Different Risks

3. Geological Failure Does Not Necessarily Mean Investment Failure

Hurricane ultimately failed to deliver the connected oil volumes implied by peak market expectations for the Lancaster reservoir. Yet:

- BP reduced risk exposure by exiting early

- Kerogen appears to have generated a positive realised return

- and Crystal Amber likely monetised profitably across multiple phases.

That is an extraordinarily important distinction.

Conclusion

Hurricane Energy is often remembered as a failed North Sea growth story. In reality, it was something far more revealing:

- a case study in how different forms of capital interact with uncertainty

- how technical events reshape valuation

- and how investment timing determines realised outcomes.

The ultimate reservoir thesis may have disappointed, but the capital-allocation behaviour surrounding Hurricane was frequently sophisticated, rational, and economically successful.

That is what makes Hurricane Energy one of the most instructive fund-management case studies in recent UK upstream history.