WTI (Aug) $68.58 -92c, Brent (Sep) $71.57 -$1.38, Diff -$2.99 -46c

USNG (Aug) $3.22 -6c, UKNG (Sep) 103.75 -0.83p, TTF (Aug) €43.68 -€0.045

Oil price

Oil is down again today, just under a dollar as yet again the market is pricing in perfection which it will surely be disappointed with. The strait is indeed open-ish, but at the moment exit only, it will take more than that to get markets back to equilibrium.

Looking at the EIA stats they weren’t a mile away from the API numbers yesterday, crude drew 3.775m barrels against the 4.5m whisper whilst gasoline drew 2.333m, bigger than the -1m guess. More importantly perhaps, the SPR drew another 5.5m b’s taking it down to around 350m which will take some rebuilding, as the President has promised, capacity is a mere 700m barrels….

Genel Energy

The boards of Genel, Bidco and Capricorn have announced that they have reached agreement on the terms of a recommended cash acquisition of the entire issued and to be issued ordinary share capital of Capricorn by Bidco. The Acquisition is to be effected by means of a Scottish scheme of arrangement under Part 26 of the Companies Act.

- Under the terms of the Acquisition, each Capricorn Shareholder shall be entitled to receive, in aggregate:

US$4.74 in cash for each Capricorn Share held (the “Acquisition Value”).

- The Acquisition Value comprises, for each Capricorn Share:

- US$3.75 in cash (the “Acquisition Price”); and

- a special dividend of US$0.99, which is intended and expected to be declared prior to the Effective Date (the “Permitted Dividend”).

- The Sterling equivalent value of the Acquisition Value, being 357 pence per Capricorn Share based on the Announcement Exchange Rate, represents a premium of approximately:

- 34 per cent. to the closing price per Capricorn Share of 266 pence on 10 March 2026 (being the day prior to the start of the Offer Period (the “Undisturbed Date”)); and

- 48 per cent. to the volume weighted average price per Capricorn Share of 241 pence during the three-month period ended on the Undisturbed Date.

- The Acquisition Value (assuming the Permitted Dividend is declared and paid in full) implies a value for the entire issued and to be issued ordinary share capital of Capricorn of approximately US$360 million on a fully diluted basis, which is equivalent to £271 million based on the Announcement Exchange Rate.

- The Acquisition Price payable under the Acquisition is expressed in US$. The US$ denominated Acquisition Price reflects the underlying characteristics of Capricorn’s business activities, which are largely denominated in US$.

- A facility will be made available under which Capricorn Shareholders will be able to elect (subject to the terms and conditions of such facility) to receive the cash consideration payable in connection with the Acquisition Price in Sterling (after, if applicable, deduction of any transaction or dealing costs (including any taxes) associated with the currency conversion) at the applicable market exchange rate at which the conversion takes place (the “Foreign Exchange Facility”). The applicable market exchange rate will be fixed on the latest practicable date prior to the relevant payment date. The amount received by any Capricorn Shareholder validly electing to be paid their cash consideration payable in connection with the Acquisition Price in Sterling may therefore be below or above 282 pence per Capricorn Share depending on the applicable market exchange rate that is applied and the deduction of any transaction or dealing costs (including any taxes) associated with the currency conversion. Further details of the Foreign Exchange Facility and the election to be made by Capricorn Shareholders who wish to receive their cash consideration payable in connection with the Acquisition Price in Sterling using the Foreign Exchange Facility will be set out in the Scheme Document and the applicable Form(s) of Election.

Permitted Dividend

- As part of the Acquisition, the boards of Genel, Bidco and Capricorn have agreed to the declaration and payment of the Permitted Dividend. The Permitted Dividend is intended and expected to be declared by the Capricorn Board prior to the Effective Date, and will only be payable if the Scheme becomes Effective (or, if the Acquisition is implemented by way of a Takeover Offer and continues to be recommended by the Capricorn Board, the Takeover Offer becomes or is declared unconditional) to Capricorn Shareholders on the register of members at the Scheme Record Time (or, if the Acquisition is implemented by way of a Takeover Offer and continues to be recommended by the Capricorn Board, on the register of members on the date on which the Takeover Offer becomes or is declared unconditional).

- Capricorn Shareholders will note that the quantum of the Permitted Dividend represents an aggregate payment to shareholders of approximately $75 million. Although subject at the relevant time to compliance with applicable statutory requirements, the Capricorn Board has concluded, based on analysis carried out prior to the date of this announcement, that in all reasonable circumstances Capricorn will have available to it sufficient cash resources to pay the Permitted Dividend in full.

- However, Capricorn Shareholders should note that the ability of the Capricorn Board lawfully to declare and pay the Permitted Dividend is subject to various factors outside their control and events may occur that result in the Capricorn Board concluding that it is no longer able to declare and pay the Permitted Dividend in full. If certain circumstances as set out in further detail in paragraph 13 of this announcement were to occur, the Capricorn Directors would consider all options available to them, including whether it is in the best interests of Capricorn Shareholders to continue to implement the Scheme, which may result in the Scheme not becoming Effective. If, whether as a result of the Permitted Dividend not being paid in full or otherwise, the Acquisition does not become Effective, the Permitted Dividend will not be paid.

- Genel, Bidco and Capricorn have agreed that the Capricorn Board may declare and pay the Permitted Dividend without any reduction to the Acquisition Price. If, on or after the date of this announcement and prior to the Effective Date, any dividend, distribution, or other return of value or excess is declared, made, or paid or becomes payable by Capricorn (other than, or in excess of the amount of, the Permitted Dividend), Bidco reserves the right to reduce the Acquisition Price payable under the terms of the Acquisition for the Capricorn Shares by an amount equal to the amount of any such dividend, distribution or other return of value or excess. In such circumstances, the Capricorn Shareholders shall be entitled to retain any such dividend, distribution, or other return of value declared, made, or paid.

- If declared, the Permitted Dividend will be paid to Capricorn Shareholders in Sterling, with the amount paid to Capricorn Shareholders being the Sterling equivalent of US$0.99 per Capricorn Share based on the prevailing exchange rate on the latest practicable date for fixing such rate prior to the relevant payment date.

- If declared, the Permitted Dividend will be paid not more than 14 days after the Effective Date and in the manner to be specified in the Scheme Document. Further details are set out in paragraph 13 of this announcement.

Timetable and conditions

- It is intended that the Acquisition shall be effected by means of a Scottish Court-approved scheme of arrangement between Capricorn and Capricorn Shareholders under Part 26 of the Companies Act although Bidco reserves the right to implement the Acquisition by means of a Takeover Offer (subject to Panel consent and the terms of the Co-operation Agreement).

- The Acquisition is conditional on the approval of Capricorn Shareholders and subject to the further Conditions and terms set out in Appendix I to this announcement (which shall be set out in full in the Scheme Document).

- The Acquisition shall be put to Capricorn Shareholders at the Court Meeting and at the General Meeting. In order to become Effective, the Scheme must be approved by a majority in number of the Capricorn Shareholders voting at the Court Meeting, either in person or by proxy, representing at least 75 per cent. in value of the Capricorn Shares voted. In addition, a special resolution implementing the Scheme must be passed by Capricorn Shareholders representing at least 75 per cent. of votes cast at the General Meeting.

- The Scheme Document, containing further information about the Acquisition and notices of the Court Meeting and the General Meeting, shall be published within 28 days of the date of this announcement.

- Consistent with Genel’s approach to constructive, collaborative and respectful stakeholder relationships, Bidco and Genel (in co-operation with Capricorn) have already initiated discussions with the Egyptian Government to emphasise Bidco and Genel’s commitment to Egypt and to developing a good working relationship with the Egyptian Government. In the context of the importance of developing a good working relationship with the Egyptian Government, Genel and Bidco will be seeking the consent of EGPC to the Acquisition. Notwithstanding the positive engagement with the Egyptian Government to date, Capricorn Shareholders’ attention is specifically drawn to the Egyptian Condition, its importance to Bidco and Genel and the rationale for its inclusion (as set out in more detail in paragraph 15 below).

- The Egyptian Condition has been included at Genel’s request, for the reasons stated above and to take account of the particular circumstances of the Acquisition following negotiation between Genel and Capricorn.

- Capricorn Shareholders and Genel Shareholders should note that Genel intends to seek the Panel’s consent to invoke the Egyptian Condition in accordance with Rule 13.5(a) of the Takeover Code if the Egyptian Condition is not satisfied or capable of being satisfied by the Long-stop Date. A decision by the Panel whether to permit Genel to invoke a Condition would be judged by the Panel by reference to the facts at the time that the relevant circumstances arise, including the views of the Capricorn Directors at the time.

- It is expected that the Scheme will become Effective (subject to the satisfaction of the Conditions) during the second half of 2026.

Capricorn recommendation

- The Capricorn Directors, who have been so advised by Canaccord Genuity as to the financial terms of the Acquisition, consider the terms of the Acquisition to be fair and reasonable. In providing its advice to the Capricorn Directors, Canaccord Genuity has taken into account the commercial assessments of the Capricorn Directors. Canaccord Genuity is providing independent financial advice to the Capricorn Directors for the purposes of Rule 3 of the Code.

- Accordingly, the Capricorn Directors intend to recommend unanimously that Capricorn Shareholders vote in favour of the Scheme at the Court Meeting and the resolutions to be proposed at the General Meeting, as the Capricorn Director who holds Capricorn Shares has irrevocably undertaken to do in respect of his own beneficial holdings of 4,395 Capricorn Shares representing, in aggregate, approximately 0.006 per cent. of the share capital of Capricorn in issue on 1 July 2026 (being the latest practicable date prior to this announcement).

- Bidco has also received irrevocable undertakings to vote in favour of the Scheme at the Court Meeting and the resolutions to be proposed at the General Meeting from Palliser Capital (UK) Ltd, Newtyn Management, LLC, Kite Lake Capital Management (UK) LLP, and Madison Avenue Partners, LP in respect of a total of 27,749,043 Capricorn Shares representing, in aggregate, approximately 39.3% of Capricorn’s issued share capital.

- Bidco has therefore received irrevocable undertakings in respect of a total of 27,753,438 Capricorn Shares representing, in aggregate, approximately 39.3% of Capricorn’s share capital in issue on 1 July 2026 (being the latest practicable date prior to this announcement).

Background to and reasons for the Acquisition

- Genel’s strategy is to build a business with resilient diversified cash flows that deliver sustainable value to shareholders. The Genel Board and Genel management are resolute in their belief that this can best be achieved through strategic acquisitions which add substantial high-quality producing assets to its existing portfolio.

- Genel’s existing production base consists of its 25% non-operated working interest in the Tawke PSC, located in the Kurdistan Region of Iraq, which generates significant free cash flow from production averaging 17,520 bopd for the full year of 2025 (20,000 bopd exit rate in December 2025) and industry leading operating costs of around $4/bbl. It is comprised of two very high-quality fields, Tawke and Peshkabir, which in combination represent a world class licence.

- Genel has been seeking to acquire new production assets in preferred geographies that it has identified to build-out a significant and diverse strategic footprint.

- Egypt was identified as one of Genel’s focus countries to expand its footprint and Genel has tracked and evaluated numerous opportunities in the country.

- After conducting a detailed review of Capricorn’s assets and operations, the Genel Board and Genel management have determined that an acquisition of the Egyptian Western Desert portfolio represents an attractive strategic pillar to its business. The combined business is a larger, more diversified MENA-focused exploration & production company with a strong, resilient production base from a number of significant oil and gas fields. The cash generation from the baseline production business is significant, with an expectation that 2P reserves will be replaced and increased from the extensive portfolio of further resource opportunities.

- More specifically, key benefits include:

- Scale and diversification:

- The Acquisition will create an independent energy company of scale in the MENA region with a strong, low leverage balance sheet, significant production, reserves and resource upside.

- The Enlarged Group will hold a geographically diversified production base, with pro-forma 2P reserves of 117 mmboe and production of 41,003 bopd (combined December 2025 exit rate) (split evenly between Kurdistan and Egypt).

- The addition of the Egyptian portfolio to Genel’s existing Kurdistan production adds material production of both oil and gas in a new country, with a well-established regulatory regime, stable contracts and attractive fiscal terms. This represents a significant step towards its targeted diversification of resilient, sustainable cash generation.

- Reserves and Resources growth:

- The resources and potential resources of the Enlarged Group offers significant opportunity for reserves replacement and growth in Egypt and Kurdistan, as well as the build-out of a further production hub in Oman and/or Somaliland.

- The Enlarged Group will have the financial capability and appetite to allocate capital to derisking the potential asset base in an efficient and timely manner in order to maximise value delivery to its shareholders.

- The Enlarged Group is well positioned to pursue further value-accretive M&A within Egypt and the MENA region more generally.

- Complementary technical capabilities:

- Genel has extensive experience across its operated and non-operated assets in MENA and Africa throughout its 20+ year history in the region, as well as experience from senior staff in other jurisdictions. Its team has experience in delivering complex projects on time and on budget, with key features being pace of development and maximisation of capital efficiency.

- It has developed a deep understanding of the technical, commercial and stakeholder dynamics that characterise operating in government-partnered upstream environments. Genel’s experienced technical and operational teams are well placed to work constructively with Capricorn’s partner Cheiron, and with EGPC and BAPETCo, to support the continued development and optimisation of the Egyptian portfolio.

- The Enlarged Group will benefit from the skill sets of both management teams, with Genel’s track record of reservoir management, production optimisation and non-operated asset stewardship providing a complementary platform to Capricorn’s existing technical engagement with its Egyptian partners.

- Together, the Enlarged Group will be better positioned to accelerate development activity across all Egyptian concessions, working with EGPC to develop the appropriate subsurface and operational activity set to commercialise both the currently estimated remaining 2P reserves and the significant contingent resource base that remains to be converted into 2P reserves.

- Scale and diversification:

Information on Genel and Bidco

Bidco

Bidco is a limited company registered in England and Wales and incorporated on 19 May 2026. Bidco is a wholly owned indirect subsidiary of Genel. Bidco was formed for the purposes of the Acquisition and has not traded since its date of incorporation, nor has it entered into any obligations other than in connection with the Acquisition. Further details in relation to Bidco will be contained in the Scheme Document.

Genel

Genel is a socially responsible oil producer, with a portfolio of production and exploration assets, including production assets in the Kurdistan Region of Iraq and exploration licences in Oman and Somaliland.

Genel’s strategy comprises three objectives designed to build a business with resilient and diversified cash flows that deliver sustainable value to shareholders, and with the aim of restarting the payment of a regular dividend: (i) a strong balance sheet, (ii) diversified and resilient cash generation, and (iii) investment in new cash flows.

The Genel business is a resilient, cash-generative platform with significant unvalued potential. For the financial year ended 31 December 2025, Genel generated 17,520 bopd in working interest production, with an EBITDAX of US$43 million (2024: US$1 million).

Genel Shares are listed on the Official List and admitted to trading on the Main Market of the London Stock Exchange.

Information on Capricorn

Capricorn, a Scottish public limited company, headquartered in Edinburgh, is an independent energy company which has been listed on the Main Market of the London Stock Exchange for more than 30 years.

Currently, Capricorn’s core operations are in Egypt’s Western Desert, where it holds a portfolio of onshore development and production assets. In May 2025, Capricorn agreed with EGPC to consolidate eight of its 50:50 jointly owned concessions into a single, integrated licence with enhanced commercial terms, providing a platform for future growth. On 30 March 2026, Capricorn announced that it had received formal parliamentary ratification of this agreement.

In addition to maximising value from its assets in Egypt, from 2023 onwards Capricorn has been focused on streamlining operations, reducing costs and has returned around $600 million to shareholders.

Furthermore, Capricorn has a stated strategy to explore new value-accretive opportunities, in Egypt, the UK North Sea and the broader MENA region.

Commenting on the Acquisition, Randy Neely, Chief Executive Officer of Capricorn, said:

“Since my appointment three years ago, the team has delivered strongly against our strategic priorities — returning approximately US$600 million to shareholders, reducing costs, and maximising value from our Egyptian asset base through the recently signed merged concession, establishing a sustainable long-term business. However, Capricorn requires greater scale to materially improve trading liquidity. We believe the transaction with Genel crystallises the value created by Capricorn while providing shareholders with a clear and efficient exit.”

Commenting on the Acquisition, Paul Weir, Chief Executive Officer of Genel, said:

“Today we announce a landmark transaction to acquire a leading oil and gas portfolio in Egypt — a move that delivers our strategic intent, reshapes our company’s growth trajectory, diversifies our portfolio of oil and gas fields and begins our role as a partner in Egypt’s energy future. The acquisition of Capricorn Energy and its portfolio brings high‑quality assets, material reserves, and a talented local workforce that together create immediate scale and opportunity for further onward investment and growth. By applying our technical and operational capabilities to these assets, we will work with the operator to accelerate production optimisation, replace reserves, reduce unit costs, and capture significant near‑term cash flow while preserving optionality for future development.

Equally important, this transaction commences the start of a relationship with and commitment to Egypt and its communities. We will work closely with government partners and host communities to ensure safe, environmentally responsible operations and to maximise local content and job creation.

For our shareholders, the acquisition is expected to realise accretive cash flow and returns over the coming years. For our employees and those joining from the Capricorn team, it creates new opportunities to grow and to apply best practices across a larger, more diversified asset base.

We enter this next chapter of further value creation with resolve and determination. Delivering on the promise of this transaction will require a high degree of expertise, rigorous execution, transparent engagement with stakeholders, and an unwavering commitment to safety and sustainability. I am confident that we will realise the full potential of these assets and create sustainable value for all our stakeholders.”

I am delighted to see this deal by Genel which is a very wise one, it ticks a number of boxes that the company has been planning with regard to its M&A activity and diversifies them away from Kurdistan into Egypt. Another deal in Egypt which is becoming more popular as it satisfies any previous receivable issues and of course has consolidate the PSC’s which make the venue more attractive.

Having watched developments in Egypt closely, and having visited the oil facilities there twice in recent years, I can attest that it should be an ideal place for Genel to invest, a combination of significant potential and an existing high quality team in-country to add to.

The bid is worth 357p equivalent, £271m in total and is a 34% premium for Capricorn shareholders and in my view gives plenty of potential upside for Genel’s investment and with 0ver 39% of irrevocables looks highly likely to succeed. My target price for Genel is 100p which with the stock at 55p gives plenty of headroom and I remain very confident that its place in the Bucket List is fully justified.

Union Jack Oil/ Reabold Resources

The Board of Reabold yesterday announced that they have reached agreement on the terms of a recommended all share offer by Reabold for Union Jack to be effected by means of a UK Takeover Code offer within the meaning of Part 28 of the CA 2006.

The boards of Union Jack and Reabold believe that the Offer has a compelling strategic rationale, creating a more substantial and better capitalised oil and gas investment company with complementary assets and aligned objectives. The Offer is expected to deliver benefits to shareholders and other stakeholders of both companies, including enhanced scale, improved access to capital and a broader, more diversified portfolio. The all-share nature of the Offer enables Union Jack Shareholders to participate in the future value creation of the Enlarged Group, while Reabold Shareholders are expected to benefit from increased exposure to producing and development assets and the potential for operational efficiencies and disciplined capital allocation across a combined asset base.

In addition, having undertaken an extensive review of Union Jack’s strategic and financing options, and having carefully considered the alternatives available, the board of Union Jack has concluded that no alternative proposal capable of providing the funding required to execute Union Jack’s strategy is currently available on acceptable terms.

In the absence of such funding or the Offer, the board of Union Jack is of the view that Union Jack will, in the short term, be unable to meet its licence commitments, which, in accordance with the licence terms, may result in the forfeiture of key assets within the Union Jack portfolio.

The board of Union Jack believes that the Offer provides the only financing option to prevent this outcome and is therefore of the view that the Offer is in the best interests of shareholders.

Given the foregoing, the board of Union Jack welcomes that the Acceptance Condition has been set at a level that requires Reabold to acquire or contract to acquire shares carrying only approximately 75 per cent. of the voting rights normally exercisable at a general meeting of Union Jack.

Summary

- Under the terms of the Offer, each shareholder of Union Jack (“Union Jack Shareholders”) will be entitled to receive:

0.051 New Reabold Share(s) in exchange for every 1 Union Jack Share(s)

- The terms of the Offer value each Union Jack Share at approximately 4.19 pence, based on an exchange ratio of 0.051 new Reabold Shares for each Union Jack Share and Reabold’s closing share price of 81.0 pence on the Latest Practicable Date (the “Offer Value”) prior to the publication of this announcement (being 30 June 2026) (the “Announcement”).

- The Offer Value implies Union Jack’s entire issued, and to be issued, share capital is valued at approximately £6.14 million on a fully diluted basis.

- Upon Completion of the Offer, the Enlarged Group will have a combined market capitalisation of approximately £17.80 million (assuming full acceptance of the Offer), with Union Jack Shareholders expected to own approximately 34.01 per cent. of the Enlarged Group.

The Offer Value represents a premium of approximately:

- 25.0 per cent. to Union Jack’s closing share price of 3.35 pence on 12 June 2026, being the latest trading date prior to the publication of the statement regarding a possible offer from Reabold (the “Relevant Date”); and

- 6.1 per cent. to the volume weighted average price of 3.95 pence per Union Jack Share for the three months ended on the Relevant Date.

The share-for-share offer provides Union Jack Shareholders with the opportunity to participate in the future upside of the Enlarged Group through ownership of shares in a larger, more diversified and more liquid AIM-listed company.

Background to and reasons for the Offer

Reabold submitted a non-binding indicative proposal to the Union Jack Board on 5 June 2026 regarding a possible all-share offer, following which the parties engaged in discussions and Reabold conducted confirmatory due diligence on Union Jack’s business and assets. Following this process, the boards of Reabold and Union Jack reached agreement on the terms of a recommended all-share offer.

The Reabold Board believes the Offer has a compelling strategic rationale, combining two complementary UK-focused onshore oil and gas businesses to create a larger, more diversified and better capitalised group. The Enlarged Group is expected to benefit from increased scale, broader asset exposure (including producing and development assets), improved access to capital and enhanced ability to progress key projects.

The combination is also expected to deliver operational and corporate efficiencies, including optimised development planning across shared assets and more effective capital allocation, allowing a greater proportion of capital to be deployed directly into asset development and value creation. The all-share structure allows Union Jack Shareholders to participate in the future upside of the Enlarged Group, while providing Reabold Shareholders with increased exposure to a broader portfolio with enhanced near-term cash flow potential.

Reabold is well-funded for its upcoming work programme, including the West Newton recompletion, and has recently demonstrated continued access to capital through the successful raising of £4.16 million through the issue of equity at the prevailing market price. For Union Jack Shareholders, the Offer provides an opportunity to realise an immediate premium while also gaining increased exposure to the development upside of West Newton as well as the broader Reabold portfolio within a larger, better capitalised platform.

Recommendation

The Union Jack Directors, who have been so advised by Gneiss as to the financial terms of the Offer, consider the terms of the Offer to be fair and reasonable. In providing its advice to the Union Jack Directors, Gneiss has taken into account the commercial assessments of the Union Jack Directors. Gneiss is providing independent financial advice to the Union Jack Directors for the purposes of Rule 3 of the Code.

In addition, having undertaken an extensive review of Union Jack’s strategic and financing options, and having carefully considered the alternatives available, the board of Union Jack has concluded that no alternative proposal capable of providing the funding required to execute Union Jack’s strategy is currently available on acceptable terms.

In the absence of such funding or the Offer, the board of Union Jack is of the view that Union Jack will, in the short term, be unable to meet its licence commitments, which, in accordance with the licence terms, may result in the forfeiture of key assets within the Union Jack portfolio.

The board of Union Jack believes that the Offer provides the only financing option to prevent this outcome and is therefore of the view that the Offer is in the best interests of shareholders.

Given the foregoing, the board of Union Jack welcomes that the Acceptance Condition has been set at a level that requires Reabold to acquire or contract to acquire shares carrying only approximately 75 per cent. of the voting rights normally exercisable at a general meeting of Union Jack.

Accordingly, the Union Jack Directors intend to unanimously recommend that the Union Jack Shareholders accept the Offer, as all of the Union Jack Directors who are interested in Union Jack Shares have irrevocably undertaken to do (or procure to be done) in respect of their own holdings (and those of their connected parties) of, in aggregate, 3,132,144 Union Jack Shares, representing, in aggregate, approximately 2.14 per cent. of the issued ordinary share capital of Union Jack as at the Latest Practicable Date. These undertakings will remain binding in the event of a competing offer being made.

Considerations for the Recommendation

The Union Jack Directors believe that the combination of Union Jack and Reabold will create a strengthened onshore oil and gas company with a balanced portfolio of near-term production, appraisal and high-impact development opportunities. The Enlarged Group would benefit from enhanced scale, a simplified corporate structure, and an improved platform.

Specific other considerations for the recommendation of the Offer include:

Portfolio consolidation and enhanced exposure to core UK assets

- A combined portfolio centred on a number of high-quality UK onshore licences, including material interests in producing and near-production assets including Wressle and West Newton, providing increased exposure across a range of development stages.

- Greater alignment of interests across certain key licences where both companies currently hold positions, enabling more efficient decision-making, streamlined governance and accelerated development execution.

- A diversified portfolio spanning cash-generative production, appraisal upside and longer-term development opportunities, enhancing resilience across commodity price cycles.

Improved scale and funding flexibility

- The Enlarged Group is expected to benefit from increased market capitalisation and liquidity, positioning it as a more relevant and investable vehicle within the UK small-cap E&P sector.

- Enhanced financial flexibility, supported by a combined cash position, production revenues and reduced duplication of corporate overheads, enabling more efficient capital allocation across the portfolio.

- Greater capacity to access external funding, including both equity and debt markets, on more favourable terms, supporting the advancement of key development projects.

Acceleration of value realisation from core projects

- Increased working interests in key projects are expected to enhance exposure to production and development upside.

- A more coordinated strategy for progressing appraisal and development assets, with the aim of unlocking material contingent resource potential through technical de-risking and development planning.

Strategic and operational synergies

- A strong strategic fit between the two companies, with highly complementary asset bases, overlapping geographic focus and aligned operational priorities.

- Opportunities to realise cost synergies through the elimination of duplicated corporate functions and the rationalisation of administrative and public company costs.

Enhanced market positioning

- The creation of a larger, more diversified entity is expected to improve visibility with institutional investors, potentially increasing trading liquidity and broadening the shareholder base.

- A more compelling investment proposition, combining production cash flow with significant development and appraisal upside, positioning the Combined Group as a differentiated onshore E&P platform.

Attractive transaction terms

- The terms of the Offer provide Union Jack Shareholders with exposure to a broader and more diversified portfolio, together with the potential for enhanced long-term value creation through the Enlarged Group.

The implied valuation of the Offer represents a premium of approximately 25.0 per cent. to Union Jack’s closing share price of 3.35 pence on the Relevant Date with material upside potential through ownership of the Enlarged Group.

Irrevocable Undertakings

All of the Directors of Union Jack who currently beneficially hold or control Union Jack shares have provided irrevocable undertakings to accept the Offer in respect of 3,132,144 Union Jack Shares, representing approximately 2.14 per cent. of the issued ordinary share capital of Union Jack as at the Latest Practicable Date.

These irrevocable undertakings remain binding in the event a higher competing offer is made for Union Jack.

Further details of these irrevocable undertakings, including the circumstances in which they may lapse, are set out in paragraph 8 of this Announcement and in Appendix III to this Announcement.

Structure and Level of Acceptances

It is intended that the Offer be effected by means of a takeover offer within the meaning of Part 28 of the CA 2006.

The Offer is conditional upon Reabold having received valid acceptances (which have not been withdrawn) by no later than 1.00 p.m. (London time) on the Unconditional Date (or such later time(s) and/or date(s) as Reabold may specify, subject to the rules of the Code and, where applicable, with the consent of the Panel) in respect of not less than 75 per cent. (75%) (or such lower percentage as Reabold may decide) in value of the total Union Jack Shares to which the Offer relates and of the voting rights attached to those shares (the “Acceptance Condition”), provided that Reabold has acquired or agreed to acquire pursuant to the Offer or otherwise more than 50 per cent. (50%) of the voting rights then exercisable at a general meeting of Union Jack (the “Minimum Acceptance Threshold”). The Offer will also be subject to the NSTA Condition, the passing of the Reabold Shareholder Resolution at the Reabold General Meeting, the Admission Condition and all the other Conditions and certain further terms set out in Appendix I to this announcement being satisfied or (if capable of waiver) waived.

Information on the full details of the Offer and the expected timetable is set out in Appendix I and will be set out in an offer document, which Reabold will despatch to Union Jack Shareholders in due course (subject to certain restrictions relating to persons residing in Restricted Jurisdictions) (“Offer Document”). Subject to the same restrictions, the Offer Document will be made available by Reabold on its website at www.reabold.com and the website of Union Jack at www.unionjackoil.com.

Commenting on the Offer, Jeremy Edelman, Chairman of Reabold, said:

“We believe the proposed combination with Union Jack represents a compelling opportunity for Reabold shareholders. It would create a larger, more diversified and better capitalised company with a strengthened UK onshore oil and gas platform, providing balanced exposure to producing and development assets, improved access to funding, and the potential to deliver long-term shareholder value through increased scale, operational efficiencies, strategic synergies and disciplined capital allocation.”

Commenting on the Offer, David Bramhill, Executive Chairman of Union Jack, said:

“The Offer has a compelling strategic rationale, creating a more substantial and better capitalised oil and gas company with complementary assets and aligned objectives. The combination of Union Jack and Reabold will create a strengthened onshore oil and gas company in both the UK and internationally with a balanced portfolio of near-term production, appraisal and high-impact development opportunities in the pursuit of future value creation. The combination will deliver a better capitalised business and more diversified portfolio with enhanced scale in the UK and increased international reach and the Offer will enable Union Jack Shareholders to participate in the future value creation of the Enlarged Group.

In addition, having undertaken an extensive review of Union Jack’s strategic and financing options, and carefully considered the alternatives available, the board of Union Jack has concluded that no alternative proposal capable of providing the funding required on acceptable terms to execute Union Jack’s strategy is currently available. In the absence of such funding or the Offer, the board of Union Jack is of the view that Union Jack will, in the short term, be unable to meet its licence commitments, which in accordance with the licence terms, may result in the forfeiture of key assets within the Union Jack portfolio. The board of Union Jack believes that the Offer provides the only financing option to prevent this outcome and are therefore of the view that the Offer is in the best interests of shareholders.”

I will only be able to comment in due course after I have spoken to both parties, I have calls booked in and hope to write up next week.

Zephyr Energy

Zephyr has announced a further increase in its operated land position in the Paradox Basin, Utah, U.S. through the successful acquisition of an additional 2,294 acres of Utah Trust Lands Administration leases.

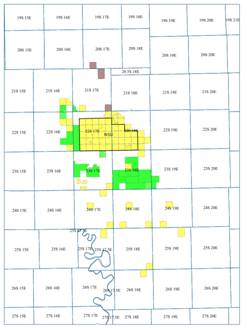

This new acquisition gives Zephyr an increased acreage footprint immediately to the north of its White Sands Unit (the “WSU”) (see Figure 1).

The acreage was nominated for auction by Zephyr and was acquired through a sealed-bid process conducted by the TLA. The related leases have a five-year primary term and a 16.67% lease royalty.

The acquisition cost associated with the TLA leases was paid from the Company’s existing cash resources.

This latest acquisition follows the Company’s recent acquisition of circa 27,000 acres, announced on 26 June 2026. Inclusive of the new acreage, the Company now operates more than 72,000 gross acres in the Paradox Basin, the majority in which the Company holds a 100% working interest.

Colin Harrington, Zephyr’s Chief Executive, said:

“I am pleased with the successful outcome from the TLA auction, the results of which further enhance the scale of our Paradox project. With every acquisition of regional acreage, we consolidate and increase the attractiveness of our regional holdings.

“We will continue to be opportunistic in building out a greater Paradox land position as we look to advance the substantial underlying value of our position in the northern Paradox Basin.”

Following last week’s announcement of further land acquisitions in the Paradox Basin, Zephyr has revealed that it has acquired another 2,294 acres of Utah Trust Lands Administration leases in the recent auction. Today’s acquisition gives Zephyr an increased acreage footprint immediately to the north of White Sand Unit.

Zephyr now commands a significant 72.000 acres in the Paradox and in my view can only add to the value of this world class asset. AS CEO Colin Harrington notes above ‘every consolidation increases the attractiveness of our regional holdings’.

I expect plenty of newsflow from Zephyr in the coming months and as I said in my recent note, ‘Expect plenty of news then in the coming months, the farm-out discussions continue along with gas marketing negotiations and with a forward looking programme as exciting as this I am not worried at all about my aggressive 20p target price’.

This announcement merely cements my view, Zephyr remains a fantastic play in the sector with lots of good news to come.

Figure 1: Map showing Zephyr’s Paradox project acreage with the new TLA acreage highlighted in brown. The Company’s original acreage is highlighted in yellow, and the recently acquired acreage (as announced on 26 June 2026) is highlighted in green. The WSU is the yellow highlighted acreage surrounded by the black border. Zephyr has nominated a substantial number of additional leases to the north of the WSU, which are expected to be auctioned in September 2026.

Sintana Energy

Sintana has provided a mid-year operational and corporate update covering the six-month period to 30 June 2026.

Over the past six months, there have been multiple tangible achievements across Sintana’s entire portfolio. These milestones have been supplemented by a number of value-positive developments across surrounding blocks and jurisdictions, reflecting the quality and strategic positioning of the Company’s asset base.

Sintana’s management therefore believes that, in aggregate, the Company is delivering precisely in line with its stated commitments. A number of important value catalysts are anticipated in the coming six-month period.

Robert Bose, Chief Executive Officer of Sintana Energy said:

“The first half of 2026 has been a period of substantial delivery across every pillar of our business. From the TotalEnergies farm-in and resource upgrade at PEL 83 in Namibia, to the completion of the first season of 3D seismic acquisition at AREA OFF-1 in Uruguay, to the corporate housekeeping that leaves us fully funded and operationally ready, we are doing exactly what we said we would do. We remain focused on continuing to deliver against our commitments, and look forward to a second half that we anticipate will see a number of further important milestones reached across the portfolio.”

This has been a busy period for Sintana with a great deal of activity going on behind the scenes to be fair, this update, coupled with the Capital Markets presentation last month which enabled the company to offer its up-to-date thoughts to the analysts in London.

Having said that the upcoming six months may put that in the shade although events may now become more visible as activity will be more obvious and that all is on track for delivery of its key strategic commitments and significant, fully funded developments.

The review below gives details of serious progress in its key areas, Namibia has seen many significant developments within and without the Sintana portfolio as the country fires up its ambitions to move ahead rapidly with its great opportunities.

Elsewhere I remain very excited about progress in Uruguay as first seismic is completed on AREA OFF-1 with results expected in H2and second tranche starting in Q4, all fully carried by Chevron here. In AREA OFF-3 the farm-out continues and with what I think is an exciting range of potential suitors which is accentuated by the corporate activity in the area including farm-ins locally and with key players such as Shell, QatarEnergy and ENI getting involved making a ‘strong endorsement of the prospectivity of the company’s Uruguayan assets’.

I remain totally convinced that Sintana is full of value that the market has yet to fully appreciate, there is so much going on in some of the energy world’s hottest post codes that my 75p target price looks eminently achievable when the market wakes up, a banker in the updated Bucket List…

NAMIBIA

Sintana’s core Namibian portfolio has seen several material milestones achieved during the period.

PEL 83 (Orange Basin)

- TotalEnergies farm-in announced: TotalEnergies farm-in to PEL 83 was announced, which once completed will encompass TotalEnergies assuming operatorship, undertaking a fully carried three well exploration and appraisal campaign (expected to commence in 2H 2026), and providing a clear pathway to a Final Investment Decision (FID) (target 2028), development of the Mopane project, and first oil (target 2032).

- 57% resource upgrade: Galp Energia announced a 57% resource upgrade for PEL 83’s Mopane project, materially increasing the independently assessed scale of the asset. The previously reported 3C contingent resource of 875 mmboe (gross) was upgraded to 1.38 bnboe (gross; Sintana’s 4.9% indirect interest ~67 mmboe).

- Value guidance: Data and technical guidance provided in various public disclosures by TotalEnergies has enabled a significantly more accurate assessment of the financial scale, value and forward timeline of PEL 83.

PEL 90 (Orange Basin)

- Well decision from Chevron: Chevron, the operator of PEL 90, indicated it intends to commence drilling of a high-impact exploration well on PEL 90 by end of 2026. The Company is fully funded for its share of anticipated costs associated with participating in this well.

PEL 82 (Walvis Basin)

- Chevron well guidance: Chevron, the operator of PEL 82, indicated that a high-impact exploration well on PEL 82 well will likely be drilled during 2027. The Company is fully carried for its share of costs associated with this well.

PEL 37 (Walvis Basin)

· Exclusivity secured: Sintana entered into a Letter of Intent providing for an exclusivity to acquire a significant position in PEL 37, at modest cost. PEL 37 is a high prospect block immediately adjacent to PEL 82, and the value of which is leveraged to the outcome of the planned exploration well on PEL 82. The Company expects to complete the transaction to acquire the interest in PEL 37 in the near-term.

Adjacent Namibian Blocks

- Orange Basin adjacent drilling success: Continued drilling success on a number of adjacent blocks over the past six months, including by Shell and Rhino, continues to provide additional technical and commercial encouragement for Sintana’s acreage.

- Walvis Basin BP farm-in: BP has farmed-in to blocks adjacent to PEL 37, a further validation of the prospectivity of the broader Walvis Basin.

URUGUAY

Sintana’s Uruguay offshore position has progressed materially during the period.

- Area OFF-1 first seismic season completed: The first season of 3D seismic acquisition on the AREA OFF-1 block was completed, representing a significant operational milestone. Initial fast track results are expected during 2H 2026, and the second season of seismic acquisition is on track to commence in Q4 2026. Sintana is fully carried by Chevron, the operator, for all anticipated costs associated with this seismic acquisition program, which is being undertaken in support of an eventual well decision.

- AREA OFF-3 farm-out process: A farm-out process in relation to AREA OFF-3 has continued throughout the past six months, with a number of international oil companies showing interest – the process is ongoing.

- Major IOC entry into adjacent acreage: QatarEnergy has entered Uruguay and farmed into two blocks adjacent to the Company’s AREA OFF-3 block; Chevron has expanded its presence in Uruguay by farming into one adjacent block; and ENI has made a new country entry with a separate farm-in. The ongoing and increasing level of investment and activity by major international oil companies in Uruguay is a strong endorsement of the prospectivity of the Company’s Uruguayan assets.

ANGOLA

- 2D seismic completed: A 2D seismic program was completed on the KON-16 block, and a farm-out process has been initiated. The Company expects to finalise the transaction in relation to the acquisition of its interest in KON-16 in the near-term.

CORPORATE

- Challenger acquisition completed: The acquisition of Challenger Energy was completed, and the Challenger Energy assets and business successfully integrated during the period.

- ExxonMobil settlement (Colombia): The Company reached a settlement with ExxonMobil in relation to the exit from its legacy Colombian interests, resulting in a significant cash receipt.

- Strong balance sheet: Inclusive of net proceeds from a successful equity capital raise, as at 30 June 2026 the Company’s cash balance was approximately $16.1 million (this includes $700,000 of restricted cash held on deposit in support of work program obligations in Uruguay). Additionally, the Company expects approximately $6.75 million of gross cash inflows during the coming six months (comprising $6 million gross in respect of the remainder of the Colombian settlement payment, and $750,000 of deferred proceeds due from sale of legacy assets in Trinidad). The Company is thus fully funded through the upcoming period of catalysts.

Original article l KeyFacts Energy Industry Directory: Malcy's Blog