Wael Sawan, Chief Executive Officer of Shell

The oil majors have spent the past decade responding to one major disruption after another. The collapse in oil prices in late 2014 forced deep spending cuts and portfolio repair. Then the energy transition pushed management teams to decide how quickly the industry would change, what that meant for oil and gas demand, and how much of their existing businesses should change with it. The roller-coaster continued as the pandemic brought an extraordinary collapse in demand, followed almost immediately by an energy crisis, a price shock and some of the strongest cash generation the industry had ever seen.

Even for a sector used to cycles, that was a lot to absorb. And throughout it all, investors were demanding that the majors compete for attention against the backdrop of soaring equity indices by cutting costs, tightening spending, improving discipline and returning more cash to shareholders.

Shell navigated that period better than many of its peers. It has remained recognisably an oil and gas company, built one of the world's strongest LNG businesses, cut costs and returned very large amounts of cash to shareholders. Management has become clearer about where it wants the company to compete and more willing to withdraw from businesses where it does not believe Shell has an advantage. That combination has created a strong investment narrative.

But a closer look at the data also reveals that Shell has made some large strategic judgements that are not immediately obvious. One of the clearest is that, since acquiring BG Group, Shell has grown the commercial reach of its LNG business while its own liquefaction volumes, production and proved reserve base have all declined from post-acquisition levels.

Shell has been clear that it sees advantage not simply in producing hydrocarbons, but in connecting production, LNG, contracts, shipping, trading, optimisation and customers across a global system. That helps explain why these trends have been allowed to diverge. It does, though, raise the question of whether Shell can continue to create increasing value from that system if it does not rebuild the physical resource base underneath it at the same rate.

This is not the only important shift the data reveal about the company. To understand how Shell arrived at its current position, and how the different parts of the strategy fit together, it is necessary to go back to 2015 and the acquisition of BG Group.

BG Group

When Shell announced its acquisition of BG Group in April 2015, it described the deal as an acceleration of its LNG and deep-water strategy. The direction Shell is pursuing today therefore did not begin with its current CEO, Wael Sawan. Its foundations were laid more than a decade ago, with a transaction recognised as transformative at the time but whose full strategic significance may only now be becoming clearer.

BG brought Shell a major position in Brazilian deep water, a large gas and LNG portfolio, equity supply, liquefaction exposure and valuable third-party LNG offtake contracts. Following the acquisition, Shell's LNG sales increased by around 46%, liquefaction volumes by 37%, production by 23% and proved reserves by 13%. Shell's filings confirm that the increases in production and reserves were driven substantially by the acquisition, including around 2.4 billion boe of proved reserve additions from BG.

Those increases reflected a change in the perimeter of the company rather than organic growth, but BG did more than make Shell larger. It reinforced a long-standing strategic fixation on gas. The deal was initially about scale and volumes, but over time that position evolved into something broader: a model in which value could be created across the LNG chain rather than only at the point of production. Shell could combine its own production and liquefaction with third-party supply, contracts, shipping, trading and customer access, giving the enlarged company far greater flexibility to move and optimise molecules across a global system.

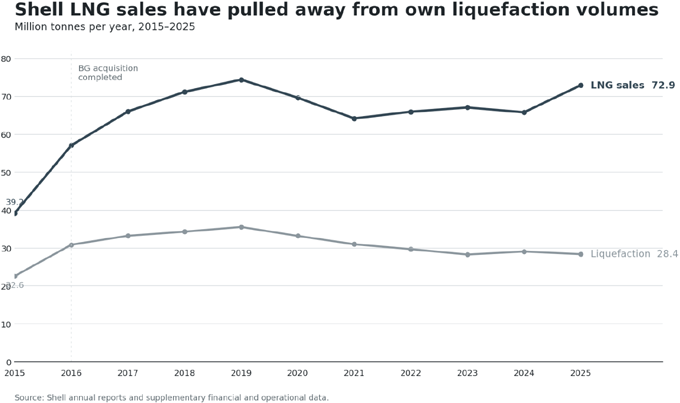

Chart 1: Shell LNG sales versus liquefaction volumes

The numbers since the acquisition show just how far that model has developed. In 2016, Shell sold 57.1 million tonnes of LNG against its own liquefaction volumes of 30.9 million tonnes. By 2025, LNG sales had risen to 72.9 million tonnes while liquefaction volumes had fallen to 28.4 million tonnes.

From the post-BG base, LNG sales increased by approximately 28% while Shell's own liquefaction volumes declined by around 8%. The relationship between the two changed materially: Shell sold LNG volumes equal to about 1.85 times its own liquefaction volumes in 2016, rising to approximately 2.57 times by 2025.

For investors, this means accepting the proposition that Shell's strategy can create more value even as some of its traditional physical volumes decline. A sophisticated LNG business does not need to own every molecule it sells. Long-term supply contracts can provide access without requiring Shell to fund every upstream development. Portfolio flexibility can redirect cargoes towards stronger markets. Shipping creates options, while trading can extract value from differences in geography, timing, contracts and prices.

The difficulty is that investors cannot value this system with the same confidence as a conventional upstream business. An oilfield can be analysed through reserves, production, decline rates, costs, taxes, investment requirements and commodity prices. Shell's integrated gas and LNG business depends on a far less transparent combination of assets, contracts, logistics, trading and optimisation.

That means the investment case requires a degree of faith: faith that the system is creating durable value, that management can continue to extract it, and that the decline in more traditional physical measures is being more than offset elsewhere. Investors may already be making that judgement without fully recognising how much of the Shell case now depends on it.

The physical base shrinks

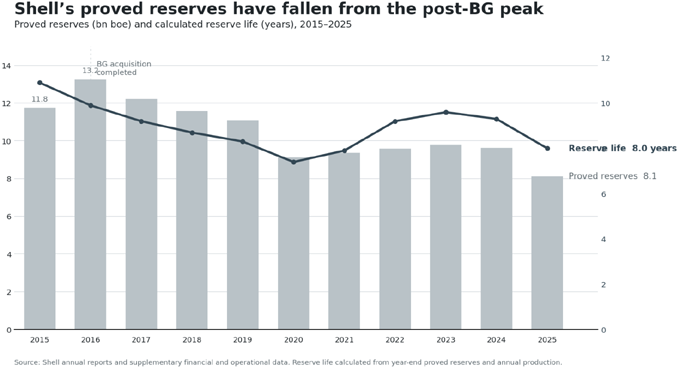

BG also gave Shell a significantly larger resource and production position. At the end of 2016, Shell had approximately 13.3 billion boe of proved reserves and was producing around 3.67 million boe/d. By the end of 2025, proved reserves had fallen to approximately 8.1 billion boe and production to around 2.8 million boe/d.

The contrast with the LNG chart is striking. Between 2016 and 2025, Shell's LNG sales increased by approximately 28%, while its own liquefaction volumes fell by around 8%, production declined by approximately 24% and proved reserves by about 39%. Chart 1 shows the commercial LNG system expanding away from Shell's own liquefaction base. Chart 2 shows what was happening elsewhere in the company at the same time: the resource base inherited and enlarged through BG was becoming materially smaller.

Chart 2: Shell proved reserves and calculated reserve life

The reserve history is not a straight line and should not be presented as one. The BG acquisition created the obvious step-up in 2016. Production then depleted the base, assets were sold and reserve estimates changed as project economics, prices and other assumptions moved. The pandemic further complicates the middle of the series because production was disrupted and reserve revisions became unusually important.

Even with those qualifications, the direction across the decade is difficult to ignore. Calculated proved reserve life fell from around 10.9 years in 2015 to approximately 7.4 years in 2020, recovered to about 9.6 years in 2023 and then fell back to around 8.0 years in 2025. The recovery after the pandemic was significant, but it was neither complete nor sustained.

The pandemic and energy crisis

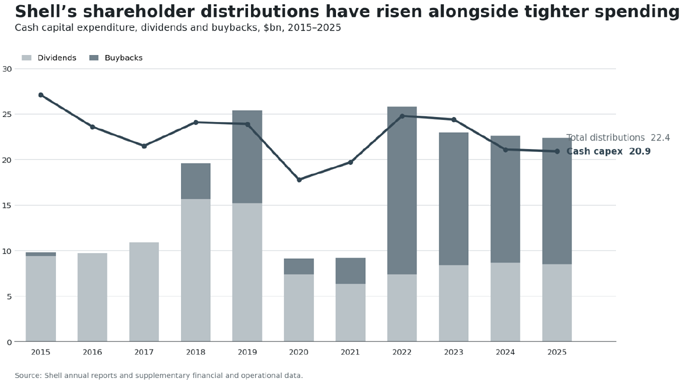

Starting the analysis in 2020 would give a flattering and incomplete picture of what happened next. The pandemic brought an extraordinary collapse in demand, sharply lower commodity prices, production disruption and severe pressure on investment. Shell cut cash capital expenditure from $23.9 billion in 2019 to $17.8 billion in 2020, while the company was still operating under a strategic framework in which oil production was expected to decline gradually over time.

The share-price chart shows just how violent the dislocation was. Shell entered 2020 trading at around £20 per share and fell below £10 during the worst of the pandemic period. The recovery that followed was equally dramatic, carrying the shares back through pre-pandemic levels as energy markets tightened and the value of Shell's oil, gas and LNG position became much clearer.

Chart 3: Shell share price

The current strategy is different in emphasis from the one Shell was pursuing before and during the pandemic. The company has become more selective, more focused on returns and clearer that Integrated Gas and Upstream remain central to the business. But the past decade is not a story of Shell abandoning one strategy and inventing another from scratch. Gas and LNG have remained persistent priorities across different management teams. BG accelerated the strategy, the 2020-era framework preserved it, and Wael Sawan has sharpened and concentrated it.

The energy crisis after Russia's invasion of Ukraine then tested the model in the opposite direction from the pandemic. European gas supply was disrupted, global LNG flows shifted rapidly, prices rose sharply and the value of shipping access, destination flexibility and the ability to move gas between customers increased. Shell was exceptionally well positioned for that environment and generated adjusted earnings of $39.9 billion in 2022, with Integrated Gas contributing $16.1 billion and Upstream $17.3 billion.

High commodity prices benefited the whole industry, but Shell had spent years building a system able to do more than simply receive a higher market price for its production. Supply positions, LNG contracts, shipping, traders, destination flexibility and a large customer base gave the company more ways to respond as the market fractured.

Exceptional volatility also made the business harder to analyse. It created exceptional commercial opportunities, but those conditions do not tell investors how much the same system will earn in more normal markets. Shell's LNG portfolio may deserve a premium because of the value it can create across different environments, but investors cannot easily separate normal earning power from the opportunities created by rare periods of market dislocation.

Above all, Shell is a cash-return machine

The decade-long spending and distribution data fall into distinct periods. After BG, Shell had a very large acquisition to absorb and a balance sheet to repair. Spending was brought under control, debt reduction became important and the company gradually returned to buybacks as the post-acquisition financial position strengthened.

The pandemic interrupted that process. Distributions fell sharply in 2020 and 2021, before rising dramatically as cash generation recovered and the energy crisis drove exceptional earnings across the sector. Shell distributed approximately $25.8 billion to shareholders in 2022, $23.0 billion in 2023, $22.6 billion in 2024 and $22.4 billion in 2025. Over those four years, approximately $94 billion went to shareholders, compared with around $91 billion of cash capital expenditure.

Chart 4: Shell cash capital expenditure, dividends and buybacks

That comparison is useful. If the accusation is that Shell has simply returned too much cash, the obvious response is that its owners demanded it. Investors had spent years telling the majors to stop pursuing production growth for its own sake, stop overinvesting at the top of the cycle and stop treating shareholders as the residual claim after every possible project had been funded.

Shell responded. Costs have been reduced, spending kept tight and shareholder distributions raised. At its 2025 Capital Markets Day, the company targeted shareholder distributions of 40–50% of cash flow from operations through the cycle, annual cash capital expenditure of $20–22 billion for 2025–28 and further structural cost reductions, while maintaining investment in Integrated Gas and Upstream and targeting more than 1 million boe/d of new production start-ups between 2025 and 2030.

There is a strong argument that this is simply what better management looks like. Previous management teams across the industry spent too much money on marginal projects, chased volume and destroyed value at the top of the cycle. Shell may now be concentrating spending on fewer, better opportunities while using its LNG, trading and optimisation capabilities to create value without matching commercial growth tonne for tonne with its own assets.

The difficulty is that the cost of not rebuilding an oil and gas portfolio does not appear immediately in the accounts. An exploration well not drilled does not reduce current earnings. A basin not entered does not create an impairment. A discovery not made cannot be seen by investors. A project deferred may improve near-term cash flow, while an acquisition not pursued leaves more money available for buybacks.

For a long time, discipline and depletion can look remarkably similar. The difference becomes clearer only later, when the resource base has to be rebuilt and the cost of doing so may be much higher.

Sawan sharpened an existing strategy

Wael Sawan did not invent Shell's gas strategy. He inherited a company whose commitment to LNG had already been reinforced decisively by BG and maintained across different management eras. His contribution has been to concentrate the company more firmly around the businesses where Shell believes it has the strongest advantages.

This is not a strategy without risks, and the risk really comes from the strength of its conviction. Shell appears increasingly confident that it can extract more value from commercial control of molecules than from simply owning more of them. If global gas trading becomes larger and more complex, its combination of supply, contracts, shipping, trading and customers may become increasingly valuable.

But complexity is not automatically value. Commercial systems still require molecules. Contracts expire. Competitors learn. Customers develop alternatives. Exceptional trading conditions normalise. The harder a business is to value independently, the more important it becomes to examine the parts that can be measured, and those measures show that Shell's commercial LNG reach has expanded while its own physical resource base has become smaller.

Management needs to be right about the value of the difference. If it is not, the consequences would be severe: Shell could find that it has allowed its physical resource base to weaken while placing increasing strategic weight on a commercial advantage that proves either less valuable or less durable than expected. Correcting that mistake, if it is one, would be extremely difficult given how far Shell has already travelled down the path it has chosen.

Competition is getting stronger

Shell has spent decades building its LNG position, but it is no longer developing that model without serious competition. ExxonMobil is making LNG a central part of its upstream growth plans and expects sales to exceed 40 million tonnes a year by 2030. TotalEnergies is expanding an integrated global LNG portfolio, QatarEnergy is increasing production capacity on a scale capable of reshaping the market itself, and large US exporters such as Cheniere are becoming increasingly important commercial participants rather than simply providers of liquefaction capacity.

Shell consequently faces two tests. The first is proving that the integrated model creates returns that genuinely compensate for the decline in its traditional physical business. The second is proving that whatever advantage the model creates is durable enough to withstand competitors building larger and more flexible portfolios of their own.

Its investment case increasingly depends not only on the system creating value today, but on Shell continuing to extract more value from it than its competitors can. That is a higher bar than simply believing LNG demand will grow.

Doubling down: ARC Resources

In April 2026, Shell agreed to acquire ARC, a major producer focused on the Montney in western Canada. The transaction adds substantial production, inventory and future development opportunities after a decade in which Shell's proved reserves and group production have declined from their post-BG levels.

ARC is an answer to the resource question raised by the data. Shell is buying physical depth. But the choice of asset reinforces its bet. It has not bought a broad oil portfolio unrelated to the rest of the strategy, it rebuilds part of the physical base while strengthening the gas and LNG system at the centre of the wider strategy. It is not a retreat from the commercial model towards a simpler resource-ownership strategy; it reinforces the supply position supporting that model.

The Montney offers large-scale gas resources, LNG Canada creates Pacific access to Asian markets, and Shell's trading and customer organisation may be able to extract more value from the combination than a standalone producer could achieve on its own, helping justify the premium paid.

But ARC also shows just how concentrated the strategic judgement has become. BG, the growth of the LNG portfolio, the widening gap between LNG sales and Shell's own liquefaction volumes, the emphasis on trading and customers, and now ARC all point in the same direction. Shell is not simply buying gas because it needs more reserves. It is buying physical supply that strengthens the system it has spent a decade building, and is now arguing that its competitive advantage in that system justifies inorganic growth.

Oil is steadily becoming relatively less important to Shell's strategic story even though it remains a major source of earnings and cash flow for both Shell and its peers. Shell is placing increasing weight on the proposition that gas, LNG and the commercial system built around them will create more value over time than a broader balance between oil and gas would have done.

Transition strategies

BP made a much more radical judgement about the speed and direction of the energy transition. It attempted to move rapidly towards a broader integrated energy company while reducing the relative importance of the oil and gas business on which its market value still depended.

Shell has not done that. Its strategy is grounded in markets where it already has expertise, assets and scale. Its LNG portfolio exists today, its traders already operate globally, its customer relationships are established and its upstream business remains substantial.

The comparison therefore does not lie in the strategy itself. It lies in the danger of becoming too certain about one version of the future. BP acted as though the future it anticipated was sufficiently certain to justify weakening other strategic options before the new model had proved itself. Shell's risk is different, but the question is still worth asking: has the company become so confident in the future value of its integrated gas and commercial system that investors are underestimating the cost of the physical depth being lost elsewhere, particularly in oil?

Shell may have judged the future correctly. Gas demand may prove stronger and more durable than many public forecasts assume. LNG may become increasingly important to power security, industrial competitiveness and rapidly growing electricity systems. Greater market complexity may increase rather than reduce the value of Shell's commercial capabilities, while scale can create more contractual options, more shipping flexibility, more customer reach and more opportunities to optimise supply.

Strong current performance gives management a credible case that the strategy is working. But strong performance should not end the analysis. Shareholders are most likely to grant management the benefit of the doubt when cash returns are good and the share price is rising. That is precisely when the underlying strategic judgement deserves the closest attention.

What long-term shareholders are really backing

Shell has navigated the past decade better than many of its competitors. It bought BG, repaired the balance sheet, survived the pandemic, demonstrated the power of its LNG system during the energy crisis, cut costs and returned enormous amounts of cash.

Those shareholder returns look impressive. But under the bonnet, the data show something more complicated. Since the first full year of BG ownership, LNG sales have increased while Shell's own liquefaction volumes, production and proved reserves have declined from their post-acquisition levels. ARC adds back physical depth, but it also strongly reinforces the same gas and LNG strategy.

Shell may ultimately be right. Its LNG, trading and customer system may continue to create increasing value even if the company does not rebuild its owned physical base at the same rate. That does not make the shares an automatic buy. The model is increasingly complex and difficult for investors to value from outside. A strong company can still be a poor investment if the valuation already reflects its strengths while underestimating the risks building beneath them.

The bet is simple, and Shell has already made it. It may prove to be one of the strongest strategic positions in the industry. But it is still a big bet, and it should be valued as one.

This article is available at PetroEquity Signal, alongside further analysis of the companies, decisions and strategic shifts shaping the sector.

Visit: petroequitysignal.com