Oberon Houston, Oil & Gas Investment Banking

An investor examining Tullow Oil today would not immediately encounter one of the great exploration stories of the modern upstream industry. The first impression would be of a company that has spent the past two years fighting for survival, struggling to avert a shareholder wipeout as weakening production and an approaching wall of debt maturities threatened to overwhelm it.

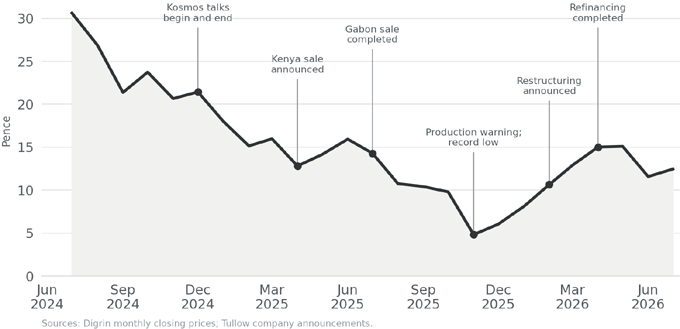

Tullow ended 2025 with net debt of some $1.35 billion against a market value of only around £185 million. It still owned a substantial production base, but precious little of its headline value reached shareholders once operating costs, royalties and taxes, sustaining capex, decommissioning and financing costs had been deducted. Even at a reasonably supportive oil price, the business generated only modest free cash flow relative to the debt it carried, leaving the shares highly sensitive to production, facilities uptime and further spending.

Only two years earlier, management had been presenting a much more optimistic recovery case. It expected the business to generate hundreds of millions of dollars of free cash flow, reduce debt materially and was even contemplating a return to shareholder distributions. A five-year facility with Glencore, accompanied by marketing and offtake agreements covering Tullow’s principal crude streams, was presented as another step towards resolving the maturity profile.

Tullow Oil recent share price history

The assistance came at a price. Glencore gained an increasingly important role in marketing Tullow’s oil and in the flow of cash from its principal producing assets. Commodity traders will finance distressed producers when conventional lenders become cautious, but they do so in exchange for security and commercial access. Glencore would later sit at the centre of Tullow’s survival.

During 2025, survival took precedence and Tullow sold almost everything outside its Ghana-centred core that could generate meaningful near-term cash. Gabon was producing and generating cash, while Kenya represented another basin-opening discovery that the company had never converted into production. The disposals raised several hundred million dollars but left the business smaller and more concentrated around two off-plateau Ghana developments whose performance had contributed to the pressure.

These were not routine portfolio refinements undertaken from a position of strength. Both assets were jettisoned not because they lacked value, but because immediate cash was needed to keep Tullow alive as the weight of debt pulled it lower.

The approaching 2026 maturity of more than $1.2 billion of secured notes left the company increasingly dependent on creditor support. A refinancing completed shortly before the deadline pushed the principal maturities into 2028 and 2030, replaced Glencore’s existing facility and added a new cargo-prepayment arrangement. It prevented an immediate collapse, but largely rearranged the debt rather than removing it.

Tullow had entered the classic balance-sheet squeeze that arises when a company cannot refinance without the agreement of those sitting ahead of shareholders in the financial structure. Creditors gained greater influence over cash generation, disposals and future spending, while shareholders retained only what remained after the debt had been protected.

Alongside the refinancing, Tullow agreed to acquire the TEN FPSO and secured extensions of the Jubilee and TEN petroleum agreements to 2040. These measures gave the Ghana assets more time and may reduce some future costs, but they did not restore the company’s strategic freedom. Most of the saleable portfolio had gone, the shares were worth pennies against the debt, and the remaining business was being managed primarily to generate cash and service creditors rather than rebuild the exploration company.

Seen through this recent history, Tullow resembles a familiar distressed upstream story: a concentrated producing portfolio, good assets sold for cash, a commodity trader embedded in the financing structure and shareholders dependent on creditors continuing to provide time. What it does not explain is how a company that once possessed several basin-opening discoveries, billions of dollars of financial capacity and one of the industry’s most highly regarded exploration teams arrived at this point.

The answer begins not in Ghana or Uganda, but in the UK Southern North Sea, where a small package of mature gas assets sold by BP gave Tullow the cash flow to build a radically different company. The decisions that followed would first turn a small independent into a £14 billion explorer, and then transform the opportunities created by its geologists into obligations that consumed almost everything they had built.

UK Southern North Sea foundations

Tullow was founded in 1985 by Aidan Heavey, an accountant rather than a geologist or petroleum engineer. Its first project was a small gas field in Senegal, and the company initially expanded through modest interests in regions and assets that were too small or peripheral to attract the largest international oil companies. It listed in London and Dublin in 1989, but remained constrained by limited production and access to capital.

The transaction that changed its prospects came in 2000, when Tullow acquired producing Southern North Sea assets from BP for approximately £200 million. The fields gave it substantial production and operating cash flow for the first time, while the Hewett and Bacton interests developed capabilities in field-life extension, infill drilling, infrastructure management and cost control. Tullow later described the acquisition as the catalyst for its subsequent growth.

There is an instructive comparison here. Perenco also acquired mature Southern North Sea gas assets from BP, but drew a different lesson from the experience. The transaction helped it recognise how much value could be created by investing in fields that larger companies no longer considered central, and it used that insight to develop a model based on acquiring mature production, improving operations and extending field life.

Tullow instead treated mature production as the means to finance frontier exploration. Perenco remained private and, by 2025, reported net production of around 324,000 boe/d. The two companies had used similar foundations to build very different businesses: Perenco deepened and repeated the mature-field model, while Tullow financed one of the most ambitious exploration organisations of its generation.

Building a formidable oil exploration company

Tullow’s transformation accelerated in 2004 with the $500 million acquisition of Energy Africa. The deal doubled the company’s size and brought producing assets, exploration acreage and technical capability across the continent, including positions that would connect Tullow to its defining discoveries in Uganda and Ghana.

Energy Africa helped combine substantial technical expertise with entrepreneurial decision-making. Management backed wells capable of transforming the business rather than limiting exploration to incremental reserve replacement, and the initial results were exceptional.

In Uganda’s Lake Albert Rift Basin, Tullow and its partners accumulated a series of discoveries that proved a material petroleum system in a region with little existing oil infrastructure. Jubilee followed offshore Ghana in 2007, establishing the commercial potential of the deepwater Tano Basin and transforming both Ghana’s petroleum industry and the market’s perception of Tullow. The Ngamia discovery in Kenya in 2012 opened another oil play in the South Lokichar Basin and reinforced the belief that the company’s results reflected a repeatable capability rather than one fortunate campaign.

Very few independents have opened several substantial petroleum provinces within such a short period. Tullow’s exploration organisation deserves to emerge from the company’s history with its reputation enhanced, because later corporate failures did not retrospectively diminish the quality of the geological work. The problem was not that the exploration teams found too little, but that the opportunities they created became too large for the company that housed them.

Valuation shifts from production to promise

Exploration success changed more than Tullow’s resource base. Its market value increasingly reflected expectations of future discoveries, developments and monetisations rather than current production alone. That premium became part of the financing machinery, allowing the company to raise substantial sums from shareholders, negotiate larger debt facilities and pursue transactions that would have been impossible for a business valued only on its producing assets.

The 2010 acquisition of Heritage Oil’s Ugandan interests illustrates the process. Tullow exercised pre-emption rights to acquire Heritage’s 50% interests in two Ugandan blocks for approximately $1.45 billion, having raised around £925 million from shareholders to support the purchase and its wider programme. A subsequent farm-down to Total and CNOOC was embedded in the plan from the outset: Tullow intended to consolidate the basin, simplify ownership and then bring in two companies with the financial and project capability required for a large, landlocked development.

The strategy was sound if the subsequent dilution took place on appropriate terms. Heritage nevertheless marked a change in Tullow’s identity. The company was now using a premium public-market valuation to acquire and consolidate entire resource positions before deciding how much of the resulting development exposure it could afford to retain.

There was nothing inherently misguided about that ambition. The assets were real, the market was supportive and management had created extraordinary value. The danger was that each successful decision expanded the next set of available choices, making larger interests, larger projects and larger financial commitments appear increasingly reasonable.

Uganda and the opportunity to reset

The Uganda farm-down was completed in February 2012, with Total and CNOOC each acquiring one-third of the licences and Tullow retaining one-third. The approximately $2.9 billion of consideration crystallised years of exploration work and basin consolidation while transferring much of the future development burden to larger, better-equipped partners.

The deal did more than validate Tullow’s exploration-and-farm-down model. It created a rare opportunity to restructure the company around the capabilities that had made it exceptional. Tullow could have reduced debt decisively, narrowed the portfolio, protected its exploration organisation and limited its exposure to the large developments already accumulating in Ghana, Uganda and Kenya. The proceeds offered the chance to preserve the core business before the cost of developing its discoveries began to overwhelm it.

Management clearly understood the principle of transferring development risk. Tullow’s strategy documents described producing assets funding exploration, while discoveries created opportunities for selective development or dilution. By 2013, management was explaining that the “real trick” was to obtain a development carry, reducing Tullow’s interest and cash contribution while preserving meaningful production exposure.

Uganda therefore appeared to complete a disciplined cycle in which Tullow could finance exploration, prove resources, sell down development exposure and recycle the proceeds. Yet the farm-down was not interpreted as a reason to consolidate the gains already made or become permanently more selective. Capital expenditure reached approximately $1.9 billion in 2012 and Tullow forecast another $2 billion in 2013 as it continued funding Jubilee, TEN, Kenya, Uganda, frontier drilling and acquisitions.

Uganda had removed one major development burden and restored substantial financial capacity. Rather than using that capacity to protect the exploration franchise and secure the producing core, Tullow deployed it across the next generation of opportunities. What might have been a strategic reset became the beginning of another worrying cycle of commitments.

Jubilee and the limits of first oil

Jubilee reached first oil in December 2010, around 40 months after discovery. The speed of the development reinforced the belief that Tullow could design, construct and operate a complex offshore project on a timetable comparable with much larger companies.

The field should not, however, be romanticised as an uncomplicated triumph. It required early well remediation and continuing drilling and water-injection investment, while production and facilities performance did not settle into a low-maintenance plateau. In 2016, damage to the FPSO Kwame Nkrumah’s turret bearing required shutdowns, altered offloading procedures, support vessels and a major remediation programme. Insurance covered much of the direct financial impact, but it did not remove the operational disruption, engineering demands or Tullow’s continuing dependence on reliable Jubilee production.

The bearing failure was unusual, but the wider lesson was not. First oil does not end deepwater risk: the owner remains exposed to reservoir performance, well productivity, pressure support, facilities uptime, maintenance and infill drilling. A major can absorb weaker production, extended downtime or higher sustaining expenditure across a broad portfolio. For a mid-cap independent, the same outcomes can determine leverage and the cash available for every other asset.

Jubilee remained a valuable field and a remarkable exploration achievement. The problem was the degree to which the wider company came to depend on it performing reliably and generating enough cash to support several other commitments at the same time.

TEN and the price of retaining risk

TEN was the point at which Tullow’s stated strategy encountered its hardest practical test. The development combined the Tweneboa, Enyenra and Ntomme discoveries, with Tullow holding 47% and acting as operator. It was designed around an FPSO with capacity of approximately 80,000 barrels a day and represented a multi-billion-dollar gross investment.

Tullow initiated a farm-down process in 2013, seeking a development carry that would reduce spending while preserving operatorship and a material interest. Aidan Heavey told investors that obtaining a carry was “not an issue”, because there were queues of interested companies; the unresolved question was value. As development advanced without an agreement, management increasingly stressed that Tullow could fund TEN itself and would not transact unless buyers accepted its valuation.

The change was strategically important. A transaction presented as the mechanism for limiting development exposure became optional when the market would not validate management’s assessment of the asset.

A farm-down is not simply a negotiation over price. An upstream development is valued through a range of possible reserves, production profiles, costs, timing and commodity prices rather than one certain outcome. Management may place substantial weight around one P50 case, while buyers reviewing the same data may reach a lower central value or attach greater probability to the downside. Their offer can represent the price at which informed counterparties are prepared to assume uncertainty, rather than an attempt to acquire the asset cheaply.

The choice is between accepting the market’s price for transferring part of that uncertainty and placing the company’s balance sheet behind management’s preferred case. A lower valuation may require an impairment and expose a gap between earlier claims and external value, but rejecting it retains more downside as well as more upside. Management can be vindicated, yet for a company of Tullow’s size, keeping almost half of TEN placed the entire business behind that judgement.

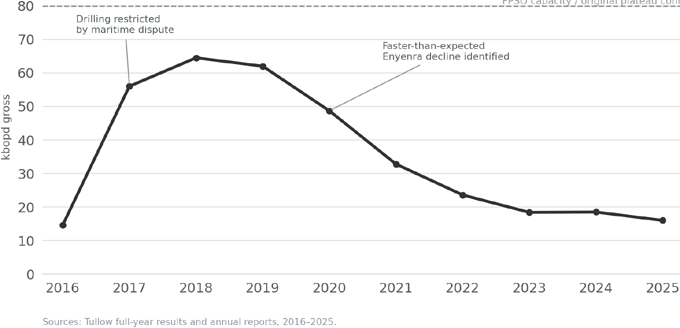

TEN reached first oil in August 2016 on schedule and within the announced development budget. The criticism is not that Tullow failed to construct the project or that the field produced no oil, but whether subsequent performance justified retaining so much exposure. Initial production was constrained by the Ghana–Côte d’Ivoire maritime dispute and improved when drilling resumed, yet later technical reviews identified faster-than-expected decline at Enyenra and weaker reserve performance elsewhere in the development.

TEN production profile

TEN continued producing and retained economic value, but it provided less margin for error than Tullow had assumed when it chose to keep almost half the project. Management’s assessment was tested first by the absence of a transaction on acceptable terms and later by the field itself.

Portfolio overwhelms the balance sheet

A mid-cap with a large interest in a deepwater development is exposed in ways not captured by the field’s headline net present value. Lower reserves, faster decline, poor facilities uptime, additional wells, lower oil prices and higher sustaining expenditure can each reduce the cash available to repay debt and support the wider business. None needs to make the field a technical failure: a development can remain valuable while delivering less cash, later and with more reinvestment, than the assumptions used when the interest was retained.

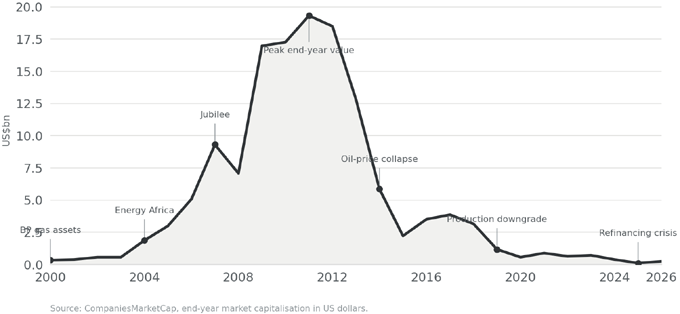

Tullow Oil market capitalisation

When several variables move adversely together, the consequences spread beyond the project. Cash expected to finance other assets or reduce debt is instead required to repair facilities, drill replacement wells, sustain production or service borrowings. Uganda did not become a poorer resource because Jubilee required remediation or TEN’s production profile was revised, but its value to Tullow shareholders was crowded out by the financial demands of Ghana and the debt accumulated around the wider programme.

A major can carry an underperforming field and wait for a slow-moving development such as Uganda to mature. A leveraged mid-cap may instead be forced to sell assets, reduce exploration or issue shares at precisely the moment when patience would preserve the most value. The relevant test is not whether a retained development eventually produces oil, but whether the company can absorb the plausible range of outcomes without sacrificing the rest of its portfolio.

The Uganda farm-down had provided approximately $2.9 billion of proceeds, sharply reduced Tullow’s immediate funding burden and created the opportunity for a more fundamental reset. The company could have reduced debt, narrowed its development exposure and preserved the exploration organisation and producing assets at the heart of its success. Instead, the cash and borrowing capacity released by Uganda were redeployed across a development and exploration programme that expanded faster than the producing business could support.

Tullow Oil balance sheet deterioration

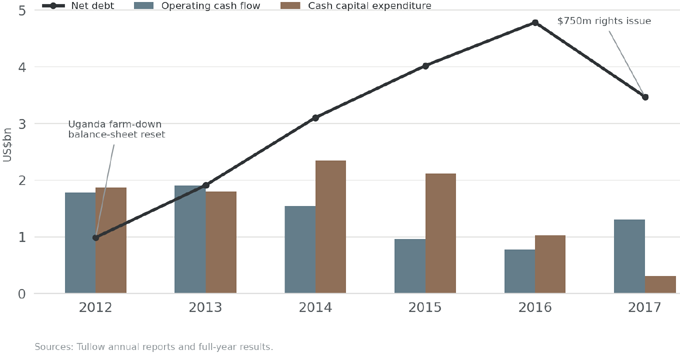

Net debt was some $1 billion at the end of 2012, rose to around $1.9 billion by the end of 2013 and reached $4.8 billion by the end of 2016. TEN was not the sole cause. Tullow was also funding Jubilee, Kenya, Uganda, frontier drilling and acquisitions. In 2013 it generated approximately $1.9 billion of operating cash flow but spent around $1.8–$2.0 billion on its capital programme, excluding Spring Energy. By 2016, despite TEN reaching first oil, operating cash flow had fallen to roughly $0.8 billion and debt reduction had become a critical need.

The increase from around $1 billion of net debt after Uganda to almost $4.8 billion four years later shows how decisively the opportunity was lost. The proceeds had not disappeared into one failed project, but had been spread across an opportunity set too large for Tullow’s internally generated cash flow to support. Uganda could have marked the point at which the company secured its core and became more selective. Instead, it restored the capacity for another round of commitments.

When the tide went out

Brent began its sharp decline in 2014, and Tullow’s subsequent difficulties are often presented as a consequence of the oil-price collapse. The chronology shows that the company’s expenditure commitments and debt trajectory were already established before the full commodity shock reached its financial statements.

Warren Buffett wrote in Berkshire Hathaway’s 1992 shareholder letter that it is only when the tide goes out that investors discover who has been swimming naked. Lower oil prices did not create Tullow’s concentration of development and financing risk; they removed the conditions that had made it appear manageable. Investors stopped giving the company full credit for distant resources and focused instead on debt service, facilities reliability, sustaining capital and near-term production.

The geology had not changed overnight, but the financial meaning of the assets had. Tullow was no longer valued principally as an exploration franchise capable of producing the next Uganda or Jubilee, but as a leveraged producer whose shareholders sat behind substantial debt and whose cash flow depended increasingly on a narrow Ghanaian base.

The oil-price decline therefore exposed rather than caused the underlying weakness. A business with less debt, fewer simultaneous development commitments and a larger margin for operational disappointment could have absorbed the shock. Tullow had instead reached the downturn with a financial structure that required too many favourable outcomes to arrive together.

From rights issue to reconstruction

Tullow cut expenditure and completed a $750 million rights issue in 2017. Net debt fell from approximately $4.8 billion at the end of 2016 to around $3.5 billion a year later, but part of the cost of the earlier strategy had been transferred back to shareholders through dilution.

The decisive break came in December 2019, when Tullow reduced its production expectations, suspended the dividend and announced the departures of chief executive Paul McDade and exploration director Angus McCoss. Debt and development concentration had previously been tolerated because investors believed Jubilee and TEN would generate sufficient cash and that the exploration organisation would continue creating value. Faster-than-expected decline at Enyenra, reserve reductions and further investment requirements at Jubilee undermined those assumptions.

The assets continued producing, but their profiles were less supportive than the financial structure required. Tullow did not need Jubilee or TEN to become worthless; it only needed the cash-generating core to deliver below expectations while the balance sheet remained critically dependent on it. The pandemic intensified the pressure, but the strategic problem was already visible.

Rahul Dhir became chief executive in 2020 with a mandate radically different from the one that had defined Tullow’s rise. The priority was no longer to open new basins but to preserve liquidity, improve Ghana performance, reduce costs, sell assets and refinance debt. Tullow sold its remaining Uganda interest to Total, demonstrating that the corporate timetable had become shorter than the asset timetable: Uganda remained valuable, but Tullow needed immediate cash and fewer commitments more urgently than long-dated upside.

Jubilee South East came onstream in 2023 and lifted gross field production towards 100,000 bopd, but even this success was used primarily to support free cash flow and debt reduction rather than rebuild the exploration model. By 2024, management again believed the company was approaching an inflection point. The optimism proved premature, leading to the Gabon and Kenya sales and the 2026 restructuring described at the beginning of this article.

The business that emerged was not the exploration-led Tullow that had opened several African basins. It was a smaller Ghana-focused producer operating within a financial framework designed principally to ensure that debt could be serviced and refinanced. Tullow survived, but much of the portfolio built during the exploration years had been sold before shareholders received the value once expected from it.

The company a major might have bought

Tullow’s history raises a corporate question that cannot now be answered conclusively. At its peak, the company offered an oil major something difficult to build internally: an entrepreneurial exploration organisation with a proven ability to open basins and a portfolio containing several material discoveries.

A larger company could have placed that capability within a broader financial structure. Jubilee, TEN, Uganda and Kenya would still have carried subsurface, execution and political risk, but underperformance by one project would have been spread across a global portfolio and a much larger balance sheet.

The opportunity may have narrowed as Tullow became increasingly committed to development. A buyer seeking exploration capability would eventually have acquired debt, operated projects and substantial future expenditure alongside the people, acreage and discoveries. There is no basis for calling this a deliberate takeover defence, but the effect may nevertheless have been defensive: Tullow became harder to acquire just as its exploration organisation may have been most attractive to a major.

By the time the shares had fallen far enough to make the company appear affordable, a buyer would have been acquiring a financial reconstruction rather than the pure exploration franchise that had once distinguished it.

The road not taken

The Perenco comparison remains useful, but Tullow did not need to become Perenco. Its more natural alternative was to remain an exploration-led company, supported by a carefully selected production base and willing to transfer development exposure when projects became too large for its balance sheet. The Uganda farm-down gave it the financial capacity to make that choice.

Tullow’s first transformation had been spectacularly successful. The Southern North Sea cash engine and Energy Africa portfolio supported an exploration organisation that found Uganda, Jubilee and Kenya and created value on a scale few independents have matched. Uganda then offered the chance to consolidate those gains: reduce debt, narrow the portfolio and preserve the exploration franchise before the cost of developing its discoveries began to dominate the company.

The difficulty came when management treated the restored capacity as the means to continue expanding. Success encouraged Tullow to retain interests and pursue developments whose subsurface and operating outcomes mattered too much to the wider business. What had begun as a model for creating and monetising options gradually became a company carrying several large, interdependent obligations.

The mistake was not that Tullow explored, found resources or developed its discoveries. A company that sells every discovery immediately may surrender much of the value its technical work has created. The caution lies in what happens when informed buyers assess a development more conservatively. Accepting a lower farm-down valuation can be painful, but it transfers risk; rejecting it means placing the wider portfolio behind management’s technical judgement.

Tullow’s experience shows how the good parts of a portfolio can be overwhelmed without becoming bad assets themselves. Uganda remained valuable and Kenya remained an important exploration achievement, but the company lost the financial flexibility needed to retain and develop them on its preferred timetable. It ultimately sold both, together with mature Gabon production that might otherwise have provided useful diversification and cash flow.

Tullow did not fail because its explorers stopped being good at their work. It struggled because the opportunities they created became too large, too capital-intensive and too concentrated for the company that housed them. Exploration created optionality, but development converted that optionality into obligations. Uganda gave Tullow the chance to reduce those obligations and protect the business that had created them; instead, the company used the reset to assume more.

When the tide went out, the discoveries were still there. What became visible was how much of their uncertainty Tullow had chosen to carry itself.

www.petroequitysignal.com l KeyFacts Energy: Tullow Ghana country profile