Westwood’s Todd Bush, Head of US Unconventionals (Energent) looks at supply, pricing and demand limitations on this critical element of the US supply chain.

In less than three years, the frac sand market erupted with in-basin frac sand in each shale play. Gone are the days of Northern White Sand (“NWS”) versus Brady Brown. Today, there are 23 frac sand mines in the Permian, 7 in Eagle Ford, 7 in Haynesville, 5 in MidCon, and additional mines announced across the US. Total supply is expected to reach 225 million tons in 2019 based on active nameplate and under construction mines. Energent’s frac sand mine database tracks the state of frac sand supply with the mine status, location, reserves, nameplate capacity, storage facilities, rail access, and more to build a mine cost curve. With this influx of frac sand supply, frac sand prices declined in the Permian and other shale plays.

Frac Sand Pricing Plummets

In August of 2018, Energent first reported Permian sand prices falling 33% to $28 per ton for contracted frac sand and $35 per ton on spot market. During the second half of 2018, more in-basin supply was brought online, further depressing prices. Currently, in-basin frac sand is available between $25 and $37 per ton at the mine.

In contrast, NWS is priced freight on board (“FOB”) destination to Midland at $78 to $85 per ton, not including the terminal charges. NWS suppliers may be able to decrease prices to $65 to $72 per ton FOB destination according to industry sources. In order to reach lower pricing levels, many suppliers believe that further collaboration with Union Pacific and BNSF is required.

Eagle Ford and Haynesville are in similar pricing situations. Eagle Ford in-basin frac sand prices range from $25 to $35 per ton at the mine compared to shipping NWS to Gonzales, Texas for $72 to $85 per ton FOB destination.

Haynesville in-basin prices range from $28 to $35 per ton at the mine versus $80 to $90 per ton FOB at destinations near Shreveport, Louisiana. Whether it is in-basin or NWS, operators still must get the sand to the well site.

Drive time for last-mile logistics

Most often, operators are contracting through pressure pumpers or logistics companies to truck frac sand to the well or pad site. Prices vary dramatically depending on the distance to the well. In the Permian, for example, the average per mile rate for a 30-mile haul is $18 per mile versus a 100-mile haul that averages $7 per mile according to our latest survey.

The below figure shows drive time analysis for the Permian based on the mine and potential well-site locations. Actual trucking times may vary widely due to lease road conditions, mine load times, and unloading conditions at the well site. Atlas Sand’s Kermit plant, for example, averages 14-minute load times while others in Winkler County may vary from 20 to 45-minute load times.

Source: Westwood Energent data and analysis

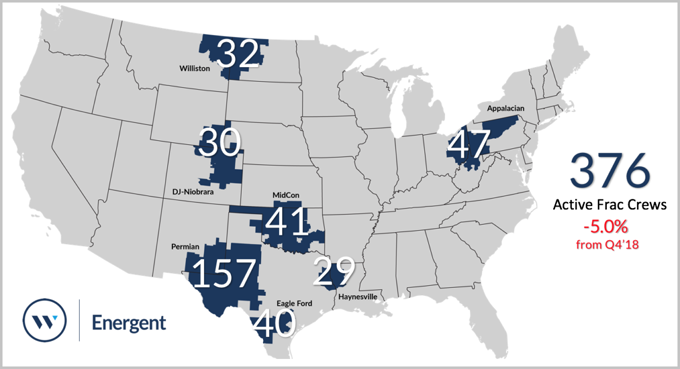

Frac crews limit sand demand in 1H’18

Financial margins are eroding across the industry with only a few sand suppliers able to offer integrated logistics, mobile storage, or well-site storage. Several mines closed during the second half of 2018 and the market should anticipate additional mines to limit or halt production. Each supplier is facing a challenging period with depressed oil prices, take-away constraints, and frac crew limiting frac sand demand.

Source: Westwood Energent data and analysis

At the Petroleum Connection’s Frac Sand Industry Update, Westwood presented on cycle time constraints and frac crew limits for frac sand demand. Every grain of sand must be pumped by a frac crew. Depending on the basin and operator preferences, frac crews may consume anywhere between 15,000 tons per month and 32,000 tons per month. Monthly throughput requirements by basin differ significantly from current forecasts for frac sand demand.

Frac sand supplier’s strategic flexibility is critical now that operators are debundling the key hydraulic fracturing categories – horsepower, frac sand, chemicals, and logistics – to reduce costs and gain operational efficiencies. With oilfield service stocks down, sunshine pumping about frac sand demand is no longer palatable by the investor community.

Todd Bush

Head of US Unconventionals l todd.bush@energentgroup.com

The pending update to the In-basin Frac Sand report covers highlights supply and demand in Permian, Eagle Ford, and MidCon.

KeyFacts Energy US Onshore country page l KeyFacts Energy Industry Directory: Westwood Global Energy