The West African offshore rig market has been one of the hardest hit during the oil price downturn. Once a region that attracted premium units and demanded some of the highest rig day rates – some rigs commanded over $600,000 – it quickly descended into an area with a glut of stacked rigs and a demand drought. Figure 1 shows that over the past few years utilisation in the area has plummeted to lows of 37% and 51% in the jackup and floating rig (drillship and semisubmersible) segments, respectively. However, some of the utilisation demise can be attributed to The Canary Islands[1], which has evolved into a popular long-stay car park for out of work floating rigs, and this has put an added strain on an already lagging market.

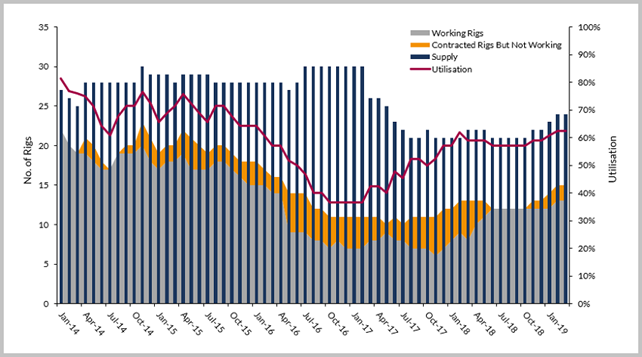

Figure 1: West African Marketed Floating Rig Supply, Demand and Utilisation – January 2014 To March 2019

Source: Westwood RigLogix

From an exploration and appraisal perspective, Wildcat data show that high-impact exploration in deepwater West Africa disappointed in 2018, with the only potentially commercial discovery at Eni’s Kalimba-1 well offshore Angola. There were some high-profile failures, such as Kosmos’ Requin Tigre-1 offshore Mauritania, FAR’s Samo-1 offshore Gambia, and two probably non-commercial pre-salt discoveries at Boudji-1 (Petronas) and Ivela-1 (Repsol) offshore Gabon. This year will see Total drilling its first wells in the MSGBC, at the Jamm-1 and Yaboy-1 wells offshore Senegal and Mauritania respectively. Kosmos, carried by BP, will drill the large Orca prospect which is reported to have 13tcf in-place potential. Elsewhere on the margin, Svenska is expected to drill the Atum-1 prospect offshore Guinea Bissau and Eni is expected to continue its exploration campaign in block 15/06 offshore Angola.

Over the coming years there are several planned developments that will provide long-term rig demand in the region if they come to fruition. Woodside Petroleum will drill up to 25 wells using two floating rigs at its SNE Phase 1 project off Senegal, Aker Energy will drill up to 26 wells at its Deepwater Tano/Cape Three Points Phase 1 project in Ghanaian waters, while Total, BP and Chevron have various long-term developments planned off the coast of Angola.

As illustrated in Figure 1, the West African jackup market was at its peak in January 2014; all but one marketed unit[2] was on hire and overall utilisation was a strong 81%. However, from that point on utilisation steadily deteriorated as the downturn took hold and as a result, utilisation plummeted to just 37% by October 2016 when only 11 of the 30 rigs in the region were under contract.

Drilling contractors finally reacted in late first quarter 2017 by retiring older assets, which resulted in a supply decline of 9 rigs by the end of that year. Since then, despite a few dips and coupled with a demand uptick, the market has experienced a bit of improvement with utilisation reaching 53% in early March 2019.

There are not only fewer jackups in the region since the downturn but also fewer players. Shelf Drilling and Borr Drilling are the two biggest jackup providers in the market, with a few others such as Vantage Drilling and ENSCO also in the mix. Supply increased by three units between fourth quarter 2018 and first quarter 2019 due to Borr securing work for a few newbuilds in the Far East and Shelf bringing in units from other regions for new commitments. Day rates in the segment remain subdued, though some of the high-specification units are understood to have been fixed in the $70,000 to $80,000 range of late, which is progress considering contracts were reportedly being fixed below $60,000 per day for many units.

Jackup demand has made progress over the last 18 months thanks in part to contract awards for long-term development campaigns from the likes of ExxonMobil and First E&P off Nigeria. However, there are just a handful of outstanding tenders in the region for drilling scheduled tobegin in the next year, so without further attrition or additional demand created, utilisation is likely to remain stagnant.

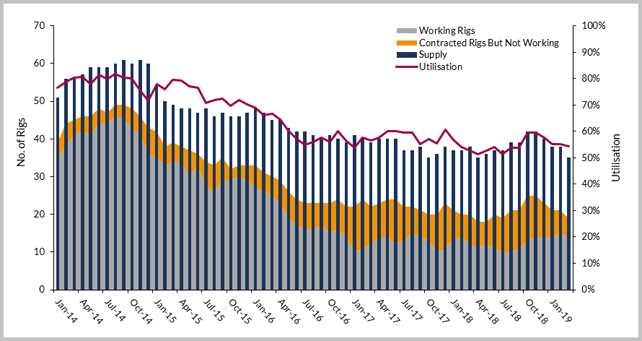

Figure 2: West African Marketed Floating Rig Supply, Demand and Utilisation – January 2014 To March 2019

Source: Westwood RigLogix

In comparison to the jackup segment, the downturn in the floating rig market has been more severe, prolonged and, as already mentioned, worsened due to the Canaries becoming a popular stacking ground for such units. As shown in Figure 2, the floating fleet hit its highest utilisation in August 2014 at 82% (48 of the 59 rigs were committed). However, just one month later utilisation started its freefall and did not stop until four years later when, in July 2018, it bottomed out at 51% with only 18 of 35 rigs on hire.

Had it not been for the 23 rigs removed from the fleet (60 reduced to 37), the utilisation situation could have been more dire. Fast forward to present day and there is still a vast surplus of rigs in the region – with a paltry 19 out of 35 rigs currently on hire or with contracts due to start this year. Utilisation remains below 60%, and day rates in the region remain low, with most known contracts fixed between $130,000 and $170,000 per day. Rumours suggest two soon-to-be-awarded contracts for work with a 2020 start may be fixed in the $200,000-$300,000 per day benchmark, but this is due to the operator requesting drilling contractors to accept contract conditions with high liabilities.

As noted previously, the floating rig segment has no shortage of ‘planned’ deepwater developments over the coming years, with the likes of Total and Woodside requiring more than one unit for long-term campaigns. Rig contracts for these projects will all depend on final investment decisions (FID) timing as many have been delayed for several years. Additionally, at least four units will leave the region in the next 12 months for work elsewhere which will help with supply glut.

If drilling contractor’s fourth quarter 2018 presentations are anything to go by, the worst of the downturn is behind us and rig demand and utilisation will continue to increase over the next few years. The cogs are in motion for a recovery in the African rig market, but it will not be a rapid recuperation as witnessed in areas such as Norway. This market will need aid in the form of further rigs being moved from the region for work elsewhere or through further attrition where possible, but most important of all, operator exploration and development projects in the region need to be approved more quickly. Of course, additional exploration success such as the recent Total discovery at Brulpadda in South Africa should help quicken that pace.

Teresa Wilkie, Senior Analyst

twilkie@westwoodenergy.com

[1] In January 2014 there were four cold-stacked jackups in the region that were not marketed for work.

[2] RigLogix classes the Canary Islands as being part of the West Africa region.

KeyFacts Energy Industry Directory: Westwood Global Energy