By Dr Simon P. Todd, Capriole Energy

US Shale oil doesn’t work at $50/bo oil price, it’s dead in the water at $25. One of five brutal facts the US oil industry needs to confront.

“Churchill said: ‘We are resolved to destroy Hitler and every vestige of the Nazi regime. From this, nothing will turn us. Nothing! We will never parley. We will never negotiate with Hitler or any of his gang. We shall fight him by land. We shall fight him by sea. We shall fight him in the air. Until, with God’s help, we have rid the earth of his shadow.’

Armed with this bold vision, Churchill never failed, however, to confront the most brutal facts. He feared that his towering, charismatic personality might deter bad news from reaching him in its starkest form. So, early in the war, he created an entirely separate department outside the normal chain of command, called the Statistical Office, with the principal function of feeding him—continuously updated and completely unfiltered—the most brutal facts of reality. He relied heavily on this special unit throughout the war, repeatedly asking for facts, just the facts. As the Nazi panzers swept across Europe, Churchill went to bed and slept soundly: ‘I... had no need for cheering dreams,’ he wrote. ‘Facts are better than dreams.’ ”

- JIM COLLINS, GOOD TO GREAT

In his seminal book, Good to Great, author Jim Collins describes how leaders of companies on the path to greatness “confront the brutal facts”. While good-to-great leaders have a vision for the world and clarity of the mission for his/her company within that vision, they also ensure that facts, no matter how jarring, are surfaced and heard. Collins refers to the exploits of Winston Churchill during the Second World War and that despite his vision to defeat Hitler, he deliberately set up a channel of facts, the Statistical Office, that would ensure that his charismatic and overpowering personality didn’t get in the way of hearing the brutal facts (see the quote above).

The US Oil & Gas industry with its oil production and its ethos now dominated by shale oil has been ignoring some brutal facts for nearly a decade, and indeed has been covering them up with false premises and promises that even hard-nosed investors believed for a while. The tide began to turn on US shale in late 2018 when a spurt of higher oil prices failed to deliver much of any financial performance improvement. The sector continued its nose-dive to become the poorest performing sector in the market.

Further “hands-over-ears” behaviors with respect to the risk of climate change largely manifested itself as various forms of climate change denial, as self-interest and group-think fueled propaganda aimed at any target available.

Now, with the double whammy of a global market share war and drastic demand reduction caused by the reaction to coronavirus, oil sits at a little more $20 per barrel, compared to the $50/bo price which is accepted in some circles as a full-cycle breakeven price the industry needs to function. Strident actions are being taken, reduced operating costs and slashed capital budgets in a hope to survive to when perceived normalcy returns. The brutal fact that the business can’t survive in this price regime is being confronted, at least in some ways, but there’s still some denial present with requests for bailouts, political help with the price war, and even tariffs on foreign oil. However, as I argue below, the reality of full-cycle breakeven costs is only the first of five brutal facts that the industry must confront now in order to have a sustainable future in the post-coronavirus world.

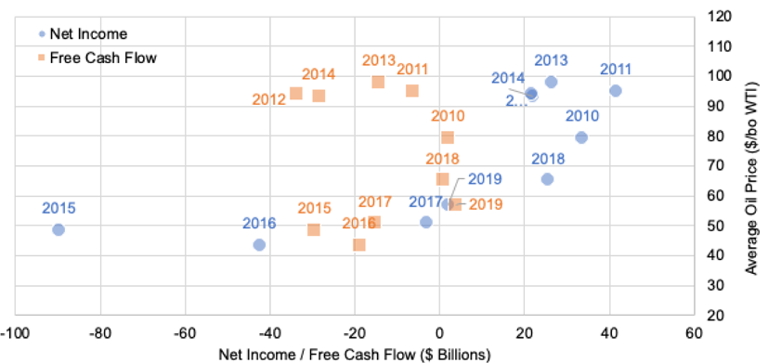

Figure 1: Total Annual Net Income and Free Cash Flow for 36 studied shale oi companies in the decade 2010-2019. (Source: Data: Yahoo Finance, EIA; Graphic: Capriole Energy).

FACT 1. US SHALE OIL NEEDS AT LEAST $55/BO PRICE TO SURVIVE

Shale gas and then shale oil was born in the late noughties when high natural gas and then oil prices enabled experimentation with horizontal wells and hydraulic fracturing. Drillers were able to create enhanced permeability in an extended well catchment in tight rock that otherwise would not flow to conventional vertical completions. The high oil and gas prices of the early part of the next decade brought wellhead returns (based on perhaps optimistic projected reserves for the wells) that attracted a lot of public and private companies into each new play in turn.

The full cycle return of the companies best measured as net income shows that oil prices about $55/bo are now required for profit to be made. In the early part of the decade, operating cash was consistently outspent by Capex as companies rushed to grab acreage and drill to increase production and EBITDA which was taken as the key performance measure of the time. So much so that even with a substantial drop in price in 2015 and 2016, drilling soon re-accelerated, with the capital shortfalls met by cheap debt. By the latter part of 2018, the shale bubble was beginning to perforate with investors realizing that real returns and return of capital were unlikely to be forthcoming from a “growth” strategy. As attention turned to shareholder returns from dividends and share buybacks in 2019, the full cycle breakevens of about $55/bo became clear (Figure 1). With 2020’s disastrous combination of supply glut with Russia and OPEC losing patience in funding US shale’s market share, coupled with the coronavirus-related demand fall, $20/bo prices have finally and dramatically exposed the shale oil business for what it is: built on debt that looks unlikely to be repaid, and ever destined to be marginally profitable only at prices significantly better than $55/bo WTI.

The reality of America's oil resource

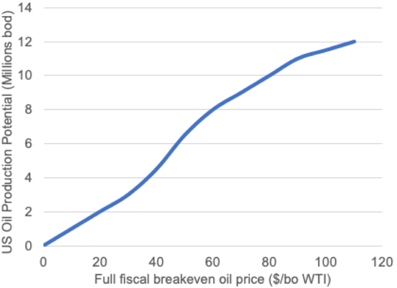

Figure 2: An approximation of the “creaming curve” for US production potential versus full cycle breakeven cost (Source: Capriole Energy).

Whilst there are undoubtedly incremental cost improvements to be made, the early development wells in any hydrocarbon accumulation are likely to be the most prolific, and I think it likely capital improvements on drilling and completion efficiency will at best offset decline in reservoir performance, and full-cycle breakevens combined with sustained production for US shale are unlikely to be reduced much further from $55/bo and with time will likely increase.

Figure 2 suggests a “creaming curve” for US production potential, describing an asymptotic curve for production potential versus full-cycle breakeven oil price. The detailed shape of this curve is arguable, but the key point here for the US oil industry to face is that much, if not most of the oil potential of America needs prices higher than $55/bo to work. Without price support of that order, US oil production can only decline. In order for the US oil industry to contribute to global price increase and stabilization, US oil production must decline.

FACT 2: THE US (AND THE WORLD) ECONOMY NEEDS OIL TO BE LESS THAN $70/BO TO THRIVE

While representing less than 2% of the US economy, and underpinning about half a million jobs, the US oil and gas production and refining industries are nevertheless fiscally important to producing states like Texas, and to the US in general because of the criticality of oil and natural gas in the current energy mix. Hence, if American hydrocarbon resources are to be prioritized over foreign supplies to fuel the US economy, then it follows that industrial, commercial and individual consumers must be able to afford at least $55/bo and equivalent gasoline and diesel prices (over $2.50/gallon). But energy cannot be too expensive because these costs flow into the costs of the products made, services provided and travel desired by consumers. Economists suggest that prices above $70/bo are too expensive for the economy and consumers. Hence there is a “sweet spot” or a Goldilocks “not too hot, not too cold” zone of $60 to $70/bo that both energy suppliers and energy consumers in the hydrocarbon economy can flourish.

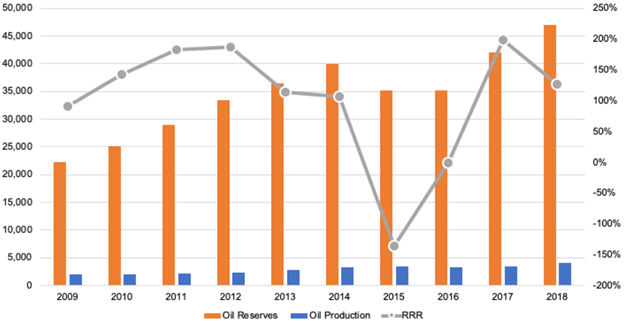

Figure 3: US Oil Reserves and Production in the last decade. RRR is Reserves Replacement Ratio which is the reserves added divided by the production in that year. (Source: Data: EIA; Graphic: Capriole Energy).

FACT 3: AMERICA REALLY IS RUNNING OUT OF AFFORDABLE OIL

Figure 3 illustrates how the oil industry has both grown oil production and oil reserves in the last decade. As well as a market that allows profitable production, to be sustainable the industry needs a Reserves Replacement Ratio better than 100%. There are three points to note in Figure 3.

Firstly, the ratio of Reserves to Production, known as R:P, although not plotted on the chart trends between 10 and 14 years during the period. In other words, if production continued at the same rate without further addition of reserves, there are about 12 years of US oil reserves left. Of course, because production declines in rate with time, the actual time to produce all the reserves is much longer. Nevertheless, it’s a good measure of the health of the reserves bank, Russia has an R:P double that of the US and Saudi Arabia’s R:P is 6 times bigger than the US.

Secondly, when price shocks like in 2015 caused reduced drilling activity, both production, and reserves addition, decline. Sustained low prices accelerate decline as reduced drilling to replace naturally declining production.

Thirdly, as noted above (Fact 1), in maturing oil fields not only does adding production get harder (more expensive) but adding reserves does too. This casts doubt on much of the reserves base depicted in Figure 3 where reserves are supposed to be technically recoverable in the economic conditions of the time. The last decade shows that shale oil has rarely yielded a profit and is in a cash hole of more than $200 billion. So if much of the last 30 billion barrels of oil was produced at a loss, on credit, why should the next 30 billion barrels be any better? This concern is only heightened by an inspection of debt-laden balance sheets of the companies involved. This is another important component for US energy policy that has been obfuscated by the “shale boom”.

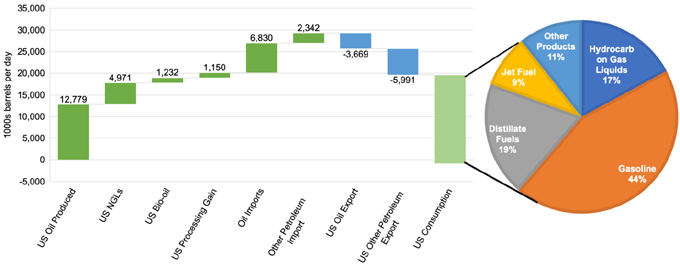

Figure 4: December 2019 balance of oil and petroleum products production, export, import and consumption (Source: Data: EIA; Graphic: Capriole Energy).

FACT 4: US SHALE OIL HAS NOT DELIVERED ENERGY INDEPENDENCE, NOR WILL IT WITHOUT OTHER POLICY MEASURES

Up until last week, America has been consuming over 20 million barrels of petroleum products each and every day. Figure 4 shows the balance of US production, imports and exports, and final consumption. The picture illustrates another obfuscation by those declaring that the US has become in 2019 a “net energy exporter” and established independence as a result.

What really has happened is that in terms of petroleum and petroleum products the US has indeed for the last few months been a net exporter, but only of petroleum products, not crude oil. This is a result of the inability of US refineries to cope with all the ultra-light oil (LTO) from the Permian and elsewhere. In 2015, despite there being options to re-tool refineries to deal with more LTO, shale producers instead lobbied the federal government to lift the decades-old export ban to command a price improvement from accessing the global price market managed by OPEC which at the time was some $10/bo better than local US pricing. By the way, this event marks the beginning of the market share war that has recently culminated in OPEC and Russia losing patience and increasing supply.

If demand remains the same, which as discussed later is questionable in a post-coronavirus world, declining US crude oil production will only increase dependency on foreign crude oil. That’s one reason why a singular enforcement of a tariff on foreign oil to “level the playing field” may be ill-advised as the current trajectories of US consumption and production indicates that America is not self-sufficient. However, as discussed further below, there are policy measures together with a transformational business model and strategy moves that can secure a more sustainable future for both a declining US oil industry and the general energy needs of the American economy.

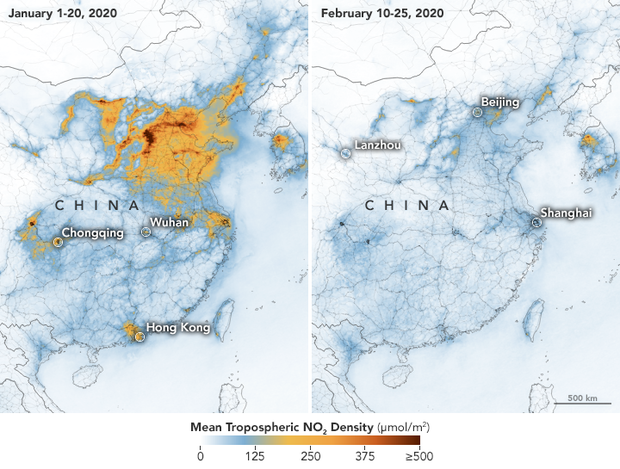

Figure 5: Before and after; the pollution reducing effects of the coronavirus lockdown in China (Source: CBS News)

FACT 5: BURNING OIL IS BAD FOR AIR QUALITY IN AMERICAN CITIES AND INCREASES THE LIKELIHOOD OF GLOBAL WARMING RISKS

This, of course, is one of the facts that the US oil industry has spent so much time denying or avoiding. But fact it is. There is so much well-documented evidence available to support this fact that I am not going to waste time here debating it. Burning oil and oil products is bad for the planet. Rather it is much more important to note the convergence of this fact with the previous four, if one is concerned about a sustainable and secure energy future for America. Simply stated, America must drastically reduce its dependence on environmentally damaging burning of an expensive, price-volatile, and dwindling resource such as oil.

The main target area for demand destruction is largely confined to transport: how goods and people move about the world and around America. As can be seen from Figure 4 over half of the oil-derived fuels are for gasoline and diesel, using in cars, SUVs and light trucks. A future is beckoning where oil is largely used only for its useful molecules for feedstocks for chemicals, fertilizers, plastics, polymers and countless other products that underpin modern civilization. Curiously, because of ongoing efforts to contain coronavirus outbreaks, we are beginning to see a glimpse of what a future without burning gasoline and diesel (Figure 5).

Figure 6: The man himself. Apparently he didn’t say “never waste a good crisis” and Rahm Emanuel, Chief of Staff to President Obama and later mayor of Chicago, gets the credit for that adage.

THAT’S THE FACTS, WHAT’S THE BOLD VISION?

Going back to the story about Churchill, what bold vision does the confrontation of these brutal facts enable? Here’s one view. I envisage a future in which there is a purposeful energy industry in the US and the world which is energizing a prosperous and inclusive economy. Energy is affordable and decarbonized, and yet used carefully with an efficiency that would seem extraordinary to us today. When and where burning fossil fuels and other polluting activities remain necessary, economic incentives support the capture and sequestration of the emissions or their offsetting by some other method.

Ever the optimist, I believe the current crisis is a great opportunity to galvanize ourselves to discuss and own such a vision and get working to create it (Figure 6). Good crisis management doesn’t just put out the fire but finds solutions to prevent recurrence and establish a more resilient future. So it is with the current crises we face today.

Here are some suggested steps to get the discussion started.

STEP 1: RADICALLY RE-BASE AND OPTIMIZE US UPSTREAM OIL PRODUCTION

This first step is required regardless of the other steps proposed later if the US upstream oil industry is to survive the current crisis let alone build resilience for future lower prices. In addition to cost, the most desirable barrels in the future will be those with the lowest Scope 1 and 2 greenhouse gas (GHG) emissions intensity. Fortunately for upstream operators, there will tend to be a correlation between the lowest cost and lowest carbon. Oil companies are already slashing capital budgets and executing actions to reduce operating costs and if done thoughtfully this will undoubtedly lead to some long term benefits as well as short-term reductions in production.

State and federal regulators can assist by enforcing current rules or creating new rules for well spacing, lease retention, flaring and so forth.

I’ve argued before for these radical changes and still believe that operators need to recognize that as a leadership mindset shift is as much required, as new technology and operational practices. While the actions of individual operators using technology and operational best practice to reduce both capital and operating expenditure can make an appreciable difference, these levers are likely insufficient on their own, and it appears that dramatic consolidation of companies is required to maximize the benefits of the efficiency measures, as well as providing combined companies more quality through the choice of drilling locations.

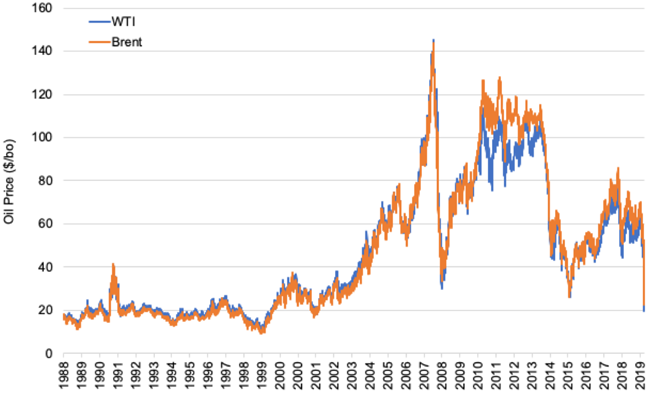

Figure 7. Oil prices, West Texas Intermediate (WTI) and Brent. (Source: Data: EIA, Graphic: Capriole Energy)

STEP 2: RESTRUCTURE THE US OIL REFINING MARKET

As the supply of US LTO was increasing rapidly in 2015, with US refineries unable to fully cope with local LTO instead of heavier, foreign grades, WTI oil prices fell some $10/bo below that of foreign crudes as priced by the Brent benchmark (Figure 7). US shale companies successfully lobbied the federal government to lift the decades-long embargo on the export of oil and so allow US LTO to access the higher international prices.

This proposed step, to restructure the US oil refining market, is essentially a reverse of the policy changes of 2015. As well as a reimposition of the export ban, this step proposes a “purchase tax” on US refiners to pay when they purchase foreign oil. The intent of this idea is to incentivize refiners to both prefer US crudes and invest in upgrades and new refinery units to handle more LTO, and for American petroleum products to serve the American economy. I don’t see it as a complete isolation of the American oil market from global resources, but in order to secure real energy independence this step enables American oil supply to meet American demand, with the target of self-sufficiency. Looking at Figure 4 again, the premise emerges that 2019 levels of US production of crude oil, condensate, NGLs, and other hydrocarbon refinery inputs, including biofuels, could have met 2019 US consumption needs if refineries could deal with the crude and other liquids that were exported.

Punitive tariffs on foreign sources of oil such as Saudi Arabia and Russia have been suggested by some. I don’t think that correct by principle, and I suspect that the long term consequences have not been fully considered. I also don’t think it’s smart to relieve the backpressure on shale companies to become more efficient. It’s painful for most if not all US producers, their contractors and the people working in the industry, but I conclude a reduced US export and some return to pre-coronavirus demand will see prices move towards the “Goldilocks” zone described above. If regulators can’t or won’t force US oil to reduce its supply, then market forces should be left to catalyze the change.

At present, I can see more logic in a “purchase tax” that is large enough to cover the amortization of refinery investment at a reasonable return, so given the data from the EIA from 2015 on investment costs, perhaps a tax or tariff in the range of $5 to $10/bo is better. The “purchase tax” dividends would be directed towards research, development, and investment into measures that reduce oil demand, such as fuel efficiency, substitution (electric and fuel vehicles), and public transport improvements.

All that said, I defer to experts to come up with the right re-structuring measures, but self-sufficiency, enabling American oil demand to be met by American oil supply should be the goal.

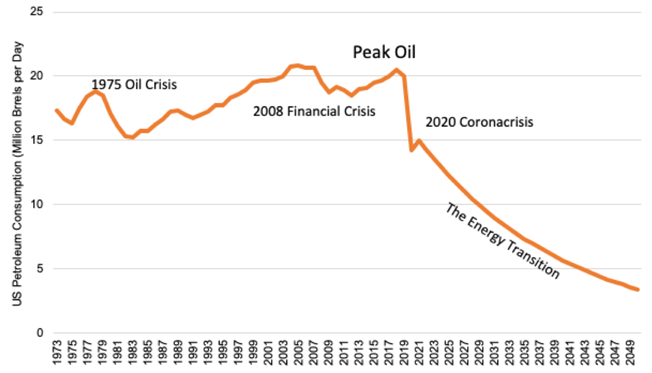

Figure 8: Consumption of petroleum products in the past, and one forecast of the future (Historical data from EIA: Graphic: Capriole Energy).

STEP 3: IMPLEMENT A PROGRAM OF GOALS, REGULATIONS, INCENTIVES, AND INVESTMENTS TO CONTINUOUSLY REDUCE US OIL CONSUMPTION

With the myth of plentiful, affordable oil in the US now fully exposed, the US must engage and accelerate its own energy transition and regain a global leadership position with respect to policy, technology, and innovation. America has fallen behind other countries with respect to the energy transition, but that provides much opportunity to learn, copy and implement appropriate policies quickly. For oil in the US, the focus is on transport. While the improvements made by car manufacturers (particularly non-US) on fuel economy in the last 15 years are substantial, they have been over-run by consumer habits of larger vehicles (like SUVs) and driving more miles.

Governments must find ways to encourage a more dramatic cultural adaptation to public transport, electric vehicles and indeed traveling in general. Perhaps the restrictions and experiences of the constraints imposed on public mobility during this coronavirus crisis will cause some of these habits and rituals. While I have to confess feeling a little cooped up here at home, unable to travel back to Ireland in April as we’d planned, the accessibility of today’s digital architecture makes continued involvement in business and social activities possible. I suspect that the post-coronavirus world will be substantially different from the one in which we began 2020, and mobility habits may be quite different. In Figure 8 I speculate on how the drastic demand reduction of 2020 might be followed by efficiencies and substitutions leading to a 5% per annum decline in American petroleum consumption, ultimately to a level where most oil is used for its useful molecules and is not wasted in combustion.

STEP 4: OIL-BIASED COMPANIES NEED TO DIVERSIFY AND RESTRUCTURE THEIR INVESTMENT PROPOSITION

This bold move involves US oil companies not only confronting the brutal facts but coming up with a new business model and strategy for the new energy world ahead. It starts with acknowledging that not only is a lot of LTO from shale too expensive for the economy, but it is a poor fit for the purpose of supplying American refineries with what they need. So the first diversification is back into forgotten medium and heavier oil fields that await secondary and tertiary recovery. Those resources would have been tackled had it not been for the shale boom, and ironically technological improvements may help with field redevelopments. Enhancements of the 45Q ruling, to incentivize sequestration of CO2 in EOR schemes, have the potential to be carbon-negative at least in the early stages of the development.

Beyond the scope of this essay, the future of natural gas, and the stabilization of its price market, also needs to be reconsidered as natural gas is a much more abundant resource than oil.

Straight underground sequestration of CO2, without EOR, should also be incentivized for harder-to-abate emissions sectors, and anything to do with reservoir development fits neatly within oil companies’ existing capabilities.

Also resonant with oil companies skills are energy opportunities like geothermal, and while solar and wind (at least onshore) might be somewhat disparate from an independent oil company’s original core business and capability, there is nevertheless an interesting and important diversification opportunity in renewables. These sectors have different risk-reward models and different capital costs and cost structures, but with the days of high-risk reward oil exploration numbered, and a stabilized oil price market tailored to reliable (and declining) demand forecasts, why couldn’t production of oil become a new low-risk low returns business model? The corollary here is a utility company like Nextera, that while biased to renewables, also has natural gas power generation in its portfolio, without any strategic incoherence.

Figure 9: The U.S. shale industry responds only to oil price signals and is like “a market without brain”, BP’s ex-chief executive Bob Dudley said in February 2019. Not only does the shale oil industry need a brain, but it needs a joined up approach with the rest of American industry with the purpose of delivering an affordable sustainable, secure and stable US economy for the future.

STEP 5: US OIL COMPANIES NEED TO MAKE A PROFIT FOR THEIR SHAREHOLDERS, BUT IT ALL NEEDS TO SERVE A PURPOSE FOR SOCIETY

It’s been interesting to observe the different responses of different US oil companies and certain pundits to the recent oil price crisis. I don’t think I am being too unfair to suggest that for the most part CEO-proposed options have firstly suited their company’s own position and prospects, with perhaps a secondary glance at others’ needs. This needs to change, dramatically.

Each company that survives the current crisis not only needs to confront the brutal facts but must collectively and collaboratively develop and embrace a new vision for America’s (and the world’s) energy future, of the kind outlined above. The collaboration should extend to developing a system and network that provides that a “brain” to assess, analyze and plan the policies, strategies, and models to be adopted in that future. Each component company needs to understand and commit to its part of the mission, its societal purpose, and the profit proposition that these investments enable.

America needs, and the world needs America to develop a leadership coalition with representatives from all quarters who are singular in their purpose to design and begin a plan for the energy transition. This coalition needs to form now and gather together, leaving self-interest, titles, egos, dogmas, and political partisanship at the door.

Capriole Energy is the company platform for Dr Simon P. Todd, an executive with broad international energy leadership experience ranging from exploration, development and production operations to organizational development, culture change and corporate governance. Simon helps boards, senior executives and investors improve the performance of their businesses while managing his own energy investments.

If you have news or commentary you would like to share, please contact us and we will be in touch.