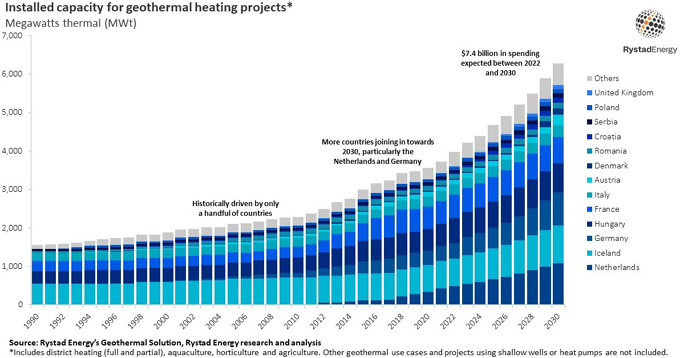

The European geothermal heating market, at one time dominated by only a handful of countries, is set to experience a purple patch in the coming years as governments scramble to find an affordable alternative to expensive gas-fired heating, Rystad Energy research shows. Total installed capacity is projected to surpass 6.2 gigawatt thermal (GWt) in 2030, a 58% increase from today’s total of 3.9 GWt, developments that are expected to cost an estimated $7.4 billion*.

A renewable, reliable source of heating, geothermal technology has been around for decades, but its heyday may be just around the corner. Due to its high development costs versus other energy sources and risks surrounding subsurface conditions and drilling success rates, widespread adoption has been relatively limited to date. A recent influx of new players in the geothermal market, many of which come from the oil and gas industry, is seeing companies pushing on with pilot projects aimed at solving the industry’s challenges.

Daniel Holmedal, senior analyst, Rystad Energy:

“Geothermal is a virtually unlimited source of consistent energy that could play a crucial role in addressing energy security and affordability in the decades to come. As European countries move to decarbonize their power mix and chase secure sources of heating for the winter months in light of geopolitical tensions, investments in geothermal projects will skyrocket"

Geothermal heating has a long history in Europe, with the industry historically led by Iceland, France and Hungary. Since 2010, however, more countries have joined in on the action, with Germany and the Netherlands showing growth plans towards 2030 that would see them lead the charts in terms of installed capacity.

Riled by energy insecurity in light of the sudden drop in Russian gas flows, Germany is pouring money into geothermal projects and is expected to spend more than $1.5 billion by 2030. In the last 10 years, installed capacity in the country has doubled from 200 megawatt thermal (MWt) in 2012 to 400 MWt today. By 2030, capacity is set to double again and approach 850 MWt. The only country to install more capacity between 2022 and 2030 will be the Netherlands, which will have more than 1 GWt capacity by the end of the decade, spending $1.1 billion in the process.

Countries that were early adopters of geothermal heating, such as Iceland, France and Hungary, are also expected to increase their capacity installations, but at a slower rate. The UK is somewhat late to the party, with more focus on geothermal power projects and only 20 MWt of geothermal heating capacity today, but that total is expected to top 100 MWt in 2030. The UK government is expected to spend more than $470 million on geothermal heating by the decade’s end.

Drilling success, development costs remain a concern

It is not all good news for the industry, however, as challenges surrounding drilling success rates and the cost of developing large-scale projects persist. The heating network is generally the most significant cost component for geothermal district heating projects. Since heating networks are installed at a local level, these networks are typically funded by local authorities or have already been built out. For our analysis, we excluded expenditure on these networks. Following that exclusion, drilling cost becomes the key driver of project costs.

Depending on subsurface temperatures at the project location, well depths range from a couple of hundred meters to a couple of thousand meters. The average drilling length for European geothermal district heating projects is around 2,000 meters, but some recent ultra-deep projects, including those in the UK and Finland, have surpassed 5,000 meters. The contribution of drilling costs to total project costs tends to decrease as projects get larger, but well depth and drilling success rates are two other important factors.

Drilling success is variable and largely dependent on the specific location of the well and the industry’s maturity in that particular country. For instance, success rates in Germany and Hungary often exceed 90%, but similar rates in the Netherlands sink as low as 70%. This can largely be attributed to the Dutch geothermal industry being in its infancy compared to its neighbors.

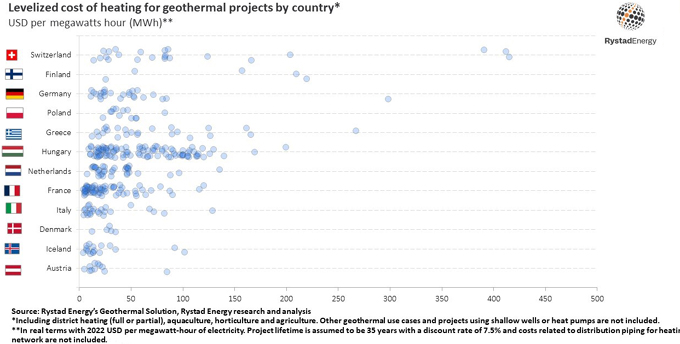

Analyzing the levelized cost of heating (LCOH) for geothermal projects compared with other sources is a helpful benchmark when evaluating its long-term validity. LCOH is the cost of producing 1-megawatt hour (MWh) of thermal energy in US dollars. The number is calculated by discount expenditure in dollars and generation in MWh for each year of the plant’s lifetime to a present-day value and dividing total discounted cost by total discounted generation. For projects in our database, we assume a lifetime of 35 years and a discount rate of 7.5%.

The LCOH of geothermal projects can vary widely, impacted by the project size, well depths and the ground-level temperature – a colder location puts more stress on the system and will have a lower levelized cost over its lifetime. The average capacity weighted LCOH for Europe (excluding Iceland) is $39. However, levelized cost varies widely between countries. France has one of the lowest average costs weighted by capacity per project at around $26 per MWh, whereas Switzerland’s LCOH clocks in at $64 per MWh.

*This analysis includes district heating (full or partial), aquaculture, horticulture and agriculture. Other geothermal use cases and projects using shallow wells or heat pumps are not included.

KeyFacts Energy Industry Directory: Rystad Energy