![]()

Tower Resources plc announces the results of an independent Reserves Report that conforms to SPE_PRMS guidelines (“Reserves Report”) from Oilfield International Limited (“OIL”) on behalf of the Company’s wholly owned subsidiary, Tower Resources Cameroon S.A, across its Thali licence, offshore Cameroon in which it holds a 100% licence interest. The Company also provides an operational update on Cameroon.

The OIL Reserves Report has quantified contingent and prospective resources across multiple fault block prospects on the Thali licence, including the existing oil discovery at Njonji in the southern part of the licence, together with their calculated Expected Monetary Value (“EMV”), as detailed below.

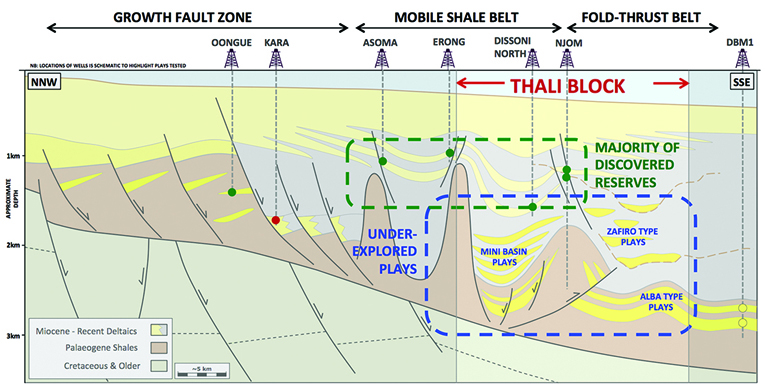

Thali licence cross-section Image source: Tower Resources

Reserve Report and other highlights:

- Gross mean contingent resources of 18 MMbbls of oil across the proven Njonji-1 and Njonji-2 fault blocks (with low/best/high estimates of 5/15/34 MMbbls) and with a development contingency probability of 80% on first phase and 70% on second phase;

- Gross mean prospective resources of 20 MMbbls of oil across the Njonji South and Njonji South-West fault blocks (with low/best/high estimates of 5/16/39 MMbbls);

- Gross mean prospective resources of 111 MMbbls of oil across four identified prospects located in the Dissoni South and Idenao areas in the northern part of the Thali licence (with low/best/high estimates of 21/84/237 MMbbls);

- Calculated EMV10s of US$118 million for the contingent resources, and US$82 million for the prospective resources, respectively;

- A Letter of Commitment has been executed to secure a modern and suitable jack-up rig for the drilling of the NJOM-3 well in Q2 2019;

- An offer of financing from an industry partner for the Thali licence has also been received and is being considered alongside other funding options.

The Reserves Report was independently compiled by UK-based industry specialist Oilfield International Limited and was based on the work that Tower has undertaken during the past year including a reprocessing and reinterpretation of all of the existing 3D seismic data over the licence area, and substantial further analysis of the data including an independent fault seal analysis undertaken by Dr Tim Needham of the University of Leeds Institute of Applied Geoscience that suggests that the Njonji 1 fault block may be in communication with the Njonji South structure. As part of the Reserves Report process, Tower has also developed a preliminary plan for the further exploration and development of the licence, subject to agreement with the Société National de Hydrocarbures (“SNH”) in Cameroon, which envisages a Phase 1 of four wells at Njonji including the proposed NJOM-3 well which is currently planned for April 2019 and an extended well test (“EWT”) commencing at the end of 2019. This Phase 1 would proceed in parallel with additional exploration in the northern part of the Thali licence, and would be followed by a Phase 2 of work on Njonji which will be further defined based on the results of Phase 1 and the additional exploration.

The well planned for Q2 2019 at Njonji (“NJOM-3”) is identified in the Reserves Report as a key gateway for the development at Njonji, as it will provide confirmation of the expected flow rates from the Njonji reservoirs, which can presently only be inferred from wireline modular formation tests (“MDT”) on the previous two wells because the previous operator did not conduct flow tests to surface. A successful drill stem test (“DST”) on this well may then, subject to the usual criteria, allow a reclassification of much of the Phase 1 contingent resources into reserves.

OIL has also calculated an EMV10 of US$118 million for the contingent resources on Njonji-1 and Njonji-2, equivalent to approximately US$6.50 per mean bbl of oil, which is the risked value of the contingent resources before making the investment required to develop them, and taking into account the cost and risk of the NJOM-3 well.

As part of the Reserves Report, OIL undertook a geologic risk assessment on the eight prospects/fault blocks, including the existing oil discoveries on Njonji-1 and Nonji-2, identified by Tower and conducted an independent review of the individual prospect risking. OIL has categorised the volumetrics on Njonji-1 and Njonji-2 as a contingent resource with an 80% chance of commercialisation (based on an estimated chance of success of NJOM-3 of 90%), and OIL has applied a 70% chance of commercialisation to the Phase 2 contingent resources, as their commercialisation is dependent on Phase 1 being executed.

The prospective resources in Njonji South and South West have been given an overall chance of development of 30% and 16% respectively. The larger Njonji South prospective Resources will be tested at low cost by one of the Phase 1 wells planned for Njonji, which can be deviated and extended to test the deeper Njonji South reservoirs, potentially adding some 18 MMbbls (Pmean) of gross resources and over US$100 million of NPV10 to the value of the Njonji project. At present, OIL estimates an EMV10 of US$22 million for the Njonji South and South West prospective resources.

There are also a further 111 MMbbls of Pmean prospective resources identified in the Dissoni South and Idenao fault blocks in the Northern part of the block, to which OIL has estimated chances of development ranging between 13% and 19%, and EMV10 of US$60 million.

| NJONJI – OIL CONTINGENT RESOURCES (Gross, MMbbls) | ||||||||||||||||

| Operator: Tower | Low Estimate | Best Estimate | High Estimate | Mean Estimate (Phase 1&2) | Chance of Development | |||||||||||

| Development Unclarified | ||||||||||||||||

| Phase I | 5.0 | 11.8 | 19.6 | 17.9 | 80% | |||||||||||

| Phase II | 0.0 | 3.4 | 14.8 | 70% | ||||||||||||

| TOTAL | 5.0 | 15.2 | 34.4 | |||||||||||||

| NJONJI – OIL CONTINGENT RESOURCES (Net Attributable to Tower, MMbbls) | ||||||||||||||||

| Operator: Tower | Low Estimate | Best Estimate | High Estimate | Chance of Development | ||||||||||||

| Development Unclarified | ||||||||||||||||

| Phase I | 3.1 | 6.9 | 10.0 | 80% | ||||||||||||

| Phase II | 0.0 | 2.0 | 7.1 | 70% | ||||||||||||

| TOTAL | 3.1 | 8.9 | 17.1 | |||||||||||||

| NJONJI – OIL PROSPECTIVE RESOURCES (Gross, MMbbls) | ||||||||||||||||

| Operator: Tower | Low Estimate | Best Estimate | High Estimate | Mean Estimate | Chance of Discovery | Chance of Commercial Success | Chance of Development | |||||||||

| Prospects | ||||||||||||||||

| Njonji South | 4.7 | 14.9 | 35.4 | 18.2 | 42% | 70% | 30% | |||||||||

| Njonji SW | 0.2 | 1.1 | 3.6 | 1.6 | 32% | 50% | 16% | |||||||||

| TOTAL | 4.9 | 16.0 | 39.0 | 19.8 | ||||||||||||

| NJONJI – OIL PROSPECTIVE RESOURCES (Net Attributable to Tower, MMbbls) | ||||||||||||||||

| Operator: Tower | Low Estimate | Best Estimate | High Estimate | Chance of Discovery | Chance of Commercial Success | Chance of Development | ||||||||||

| Prospects | ||||||||||||||||

| Njonji South | 2.5 | 7.2 | 15.9 | 42% | 70% | 30% | ||||||||||

| Njonji SW | 0.1 | 0.7 | 1.9 | 32% | 50% | 16% | ||||||||||

| TOTAL | 2.6 | 7.9 | 17.8 | |||||||||||||

| DISSONI & IDENAO – OIL PROSPECTIVE RESOURCES (Gross, MMbbls) | ||||||||||||||||

| Operator: Tower | Low Estimate | Best Estimate | High Estimate | Mean Estimate | Chance of Discovery | Chance of Commercial Success | Chance of Development | |||||||||

| Leads | ||||||||||||||||

| Dissoni South A | 8.3 | 30.9 | 76.2 | 37.8 | 24% | 80% | 19% | |||||||||

| Dissoni South B | 1.3 | 5.6 | 16.8 | 7.8 | 17% | 80% | 13% | |||||||||

| Idenao East FOI2 | 5.1 | 21.2 | 62.0 | 28.6 | 18% | 80% | 14% | |||||||||

| Idenao East FOI1 | 6.4 | 26.6 | 82.1 | 37.1 | 18% | 80% | 14% | |||||||||

| TOTAL | 21.2 | 84.3 | 237.1 | 111.3 | ||||||||||||

| DISSONI & IDENAO – OIL PROSPECTIVE RESOURCES (Net Attributable to Tower, MMbbls) | ||||||||||||||||

| Operator: Tower | Low Estimate | Best Estimate | High Estimate | Chance of Discovery | Chance of Commercial Success | Chance of Development | ||||||||||

| Leads | ||||||||||||||||

| Dissoni South A | 5.2 | 16.3 | 34.7 | 24% | 80% | 19% | ||||||||||

| Dissoni South B | 0.8 | 2.7 | 7.8 | 17% | 80% | 13% | ||||||||||

| Idenao East FOI2 | 2.9 | 10.0 | 27.2 | 18% | 80% | 14% | ||||||||||

| Idenao East FOI1 | 3.4 | 11.6 | 33.9 | 18% | 80% | 14% | ||||||||||

| TOTAL | 12.3 | 40.6 | 103.6 | |||||||||||||

| NJONJI – CONTINGENT RESOURCES (Attributable to Tower NPV10 and EMV10 US$ millions) | |||||

| Operator: Tower | After Tax NPV10 | EMV10 | |||

| Low Estimate | Best Estimate | High Estimate | Chance of Development | Swanson’s Rule | |

| Development Unclarified | |||||

| Phase I | 4.0 | 139 | 206 | 80% | 91 |

| Phase II | 0.0 | 19 | 1114 | 70% | 27 |

| TOTAL | 4.0 | 158 | 320 | 118 | |

Swanson’s Rule: 40% P50+30% P90+30% P10

| THALI LICENCE – PROSPECTIVE RESOURCES (Attributable to Tower NPV10 and EMV10 US$ millions) | |||||

| Operator: Tower | After Tax NPV10 | EMV10 | |||

| Low Estimate | Best Estimate | High Estimate | Chance of Development | Swanson’s Rule | |

| Prospective Resources | |||||

| Prospects | |||||

| Njonji South | 31 | 117 | 262 | 30% | 30 |

| Njonji SW | -3 | 7 | 29 | 16% | -8 |

| Leads | |||||

| Dissoni South A | 33 | 204 | 467 | 19% | 33 |

| Dissoni South B | 10 | 37 | 110 | 13% | -3 |

| Idenao East FOI2 | 35 | 138 | 381 | 14% | 14 |

| Idenao East FOI1 | 39 | 142 | 390 | 14% | 16 |

| TOTAL | 145 | 646 | 1639 | 82 | |

Swanson’s Rule: 40% P50+30% P90+30% P10

The Executive Summary extracted from the Reserves Report includes more detailed versions of these tables and additional figures, tables, details relating to the initial development plan and a summary of risk factors. The Executive Summary is available on the Tower Resources website at www.towerresources.co.uk.

A glossary of technical terms is included at the end of this announcement.

Cameroon Operational Update

In addition to receiving the Reserve Report, Tower’s subsidiary Tower Resources Cameroon S.A has also executed a Letter of Commitment in respect of a modern and suitable jack-up rig, to drill the NJOM-3 well between April and June 2019. The LoC is subject to contract, which Tower expects to be completed by the end of November 2018, and the terms are confidential. However, the economics set out in the LoC are consistent with Tower’s current drilling cost estimates, and Tower will be able to provide more details about the rig when the contract is finalised.

Tower has also received a proposal for partnership on the Thali licence, including a possible project financing for the NJOM-3 well, which it is considering. The Company is also discussing reserve-based financing options which could be established after a successful flow test of the NJOM-3 well.

Jeremy Asher, Chairman and CEO, commented:

“We are delighted to present our Reserve Report on the Thali licence in Cameroon, the first such report on this licence. The 18 million barrels of Pmean Contingent Resources on the Njonji structure, which we expect the NJOM-3 well to transform into Reserves, are crucial and transformative for our Cameroon project. We are already planning for production from NJOM-3 as early as the end of 2019, with three further wells being designed to increase production and also access considerable further reserves. The current EMV10 of $118 million is a good starting point for us to aim for in terms of delivering value to shareholders, but we hope to go much further as the development unfolds.

We are also pleased to be negotiating final terms of a contract for an excellent jack-up rig that is already proven in Cameroon waters and other West African territories”.